On Tuesday morning, network service provider Megaport Ltd (ASX: MP1) released its third-quarter cashflow report. The market’s response was mixed, with its share price ultimately falling 3.28% from $12.19 down to $11.79.

As the industry leader in leasing bandwidth on the private (i.e. company-to-company) internet, Megaport would seem to be socio-economically indispensable, pandemic or not. It is the leading solution for companies seeking to connect their own data centres with cloud computing data centres, and is designed for use in conjunction with Amazon Web Services, Google and Microsoft Azure for this purpose.

So it’s unsurprising that Megaport’s share price has proved resilient. Although it crashed in late March along with the rest of the market, the company has since recovered almost all of that fall.

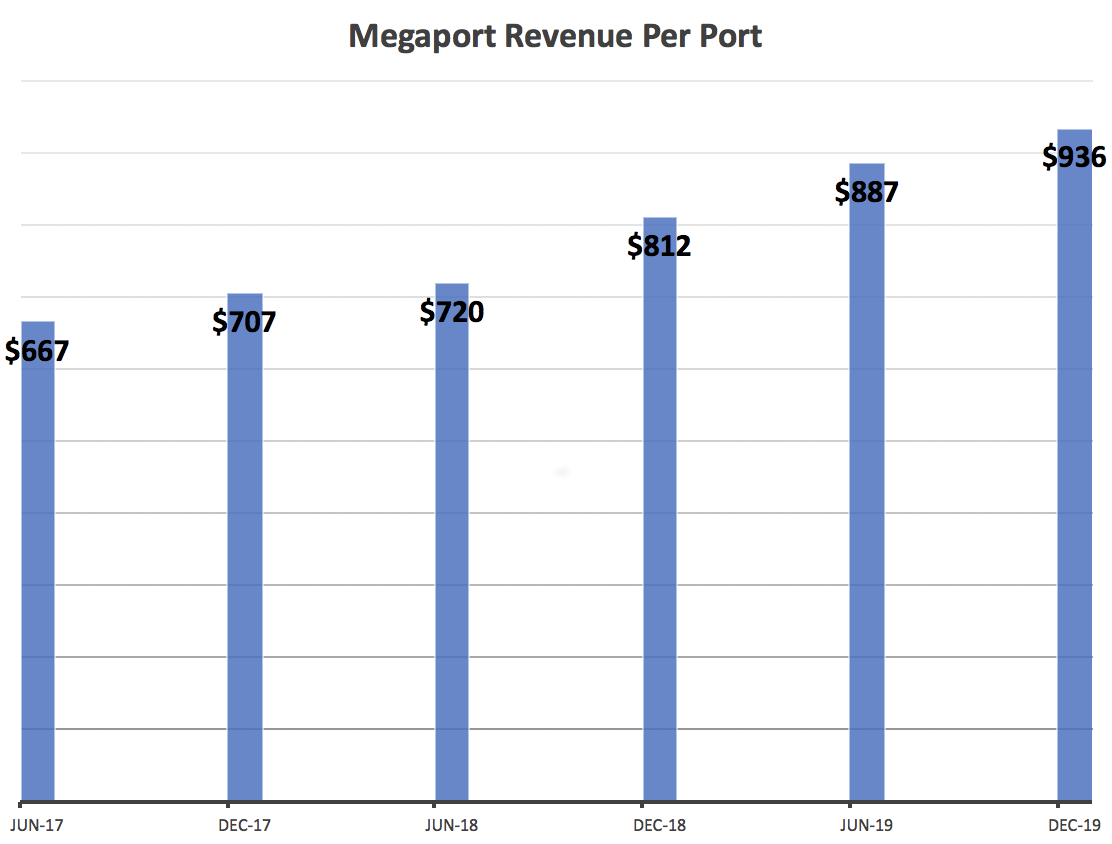

On its face, there was plenty of good news in Megaport’s quarterly report. Monthly recurring revenue has reached $5.4m, an increase of 19%. The company also has $108.7m in the bank, not including the recent institutional placement and share purchase plan worth a combined $65m.

Megaport continues to invest heavily in expansion, reporting investment of $6.3m this past quarter, in addition to its negative operations cash flow of $9.3m.

Arguably the quarter-on-quarter additional $1.6m staffing spend, predominantly relating to establishing a new team in Japan, is better classed under expansion than operations. That would cause investment expenditure to surpass operational expense.

From a long-term, world domination perspective, the strategy makes sense. The bigger a software-defined network is, the greater its value. Megaport’s margins will increase as it capitalises on the difference between the internet’s total fibre capacity and what it is able to lease out by balancing the varying on-demand requirements of its users. And of course, as the private internet inevitably continues to expand, the company’s market grows.

So the investments Megaport makes today serve a dual purpose. They increase its profitability, while also increasing entry costs to competitors.

We have trouble discerning a margin of safety in its current share price, since the company does not currently have any earnings. Furthermore, we find it very difficult to know when it will be profitable, and how much further dilution will be required to get there. What is clear, however is that Megaport Ltd is an interesting business worth following.

Revenue last half was just under $26m and its market capitalisation is over $1.75 billion, so if we annualise last half, it is trading on more than 33 times revenue. That indicates the market expects strong growth for a long time to come.

Christian Tym does not own shares in Megaport Ltd.

This post is not financial advice, and you should click here to read our detailed disclaimer.

Save time at tax time: A Rich Life depends on Supporters to pay for its free content, so if you’d like to try Sharesight, please click on this link for a FREE trial. It saves me heaps of time doing my tax and gives me plenty of insights about my returns. If you do decide to upgrade to a premium offering, you’ll get 2 months free and we’ll get a small contribution to help keep the lights on.

If you’d like to receive a occasional Free email with more content like this, then sign up today!