I’ve always had a conscious bias towards investing in medical technology. The reason for this is that I believe both technology and healthcare are favourable industries, with more demand growth in the foreseeable future. Within the realm of technology, software often plays an important role in creating a favourable business model, for the simple reason that it scales well.

Once a business has software that creates value, it doesn’t cost you much to add a new customer, because you can copy the software infinitely (or provide access to it on the cloud to as many customers as you want). Finally, it can be quite difficult and slow to win over medical clients, and there is often some specialisation required. Customers might include various departments of large hospitals pharmacy networks, radiology or pathology networks and mental health hospitals or GP clinics. These difficulties mean that customers are hard to win, but also hard to lose.

Therefore, if a small business is already making a small profit from selling medical software, and it can win new customers organically, its profit can grow much faster than revenue.

Two Med-Tech Stocks for My Portfolio

After each of these companies reported their quarterly cash flow results, my impulse was to buy shares, since both managed to showed an improved fourth quarter, when it comes to free cash flow. But I decided to hold off until I’d finished my notes below.

After reviewing the situation, I’m still planning to buy some more shares in Alcidion (ASX: ALC) (I already own some) and some shares in Mach7 Technologies (ASX: M7T). I’ll probably only make small purchases at this stage, because both companies are priced somewhat optimistically, and sentiment could change for the worse. I’m mindful that I could also add to my holding over time, if the market offers a more attractive price (or if the companies exceed expectations). Finally, it’s worth noting that Alcidion and Mach7 are loss making businesses, albeit potentially on the verge of profitability. I would still consider them high risk investments, at least until their ability to turn a full year profit is proven.

How much I invest will depend somewhat on the prevailing share price next week. Once I’ve made my first purchases, I’ll update this paragraph.

Update 12:20pm Thursday August 4, 2022: I have now made small purchases of both Mach7 and Alcidion.

Here are my notes on each…

Alcidion (ASX: ALC)

Alcidion (ASX: ALC) sells hospital clinical workflow and patient administration software principally to government healthcare systems in Australia, New Zealand and the United Kingdom. Key brands include Silverlink, Patientrack, Smartpage, ExtraMed and Miya. A core competence of the company is its ability to sell to government health systems, which has driven organic growth. As you might guess from its range of brands, the business has also used acquisitions to grow, most recently with Silverlink.

Alcidion came to the ASX in late 2015 via a backdoor listing at 3.1 cents per share. In 2018 it acquired MKM Health and Patientrack, bringing on substantial revenue and the CEO of MKM Health, Kate Quirk, as leader of the combined business. In the last half year results (H1 FY 2022) it produced revenue of $12.8m and a loss of almost $6m. Its market capitalisation at the current price of 15.5 cents per share is about $197m. It had $17.3m in cash at the end of June 2022.

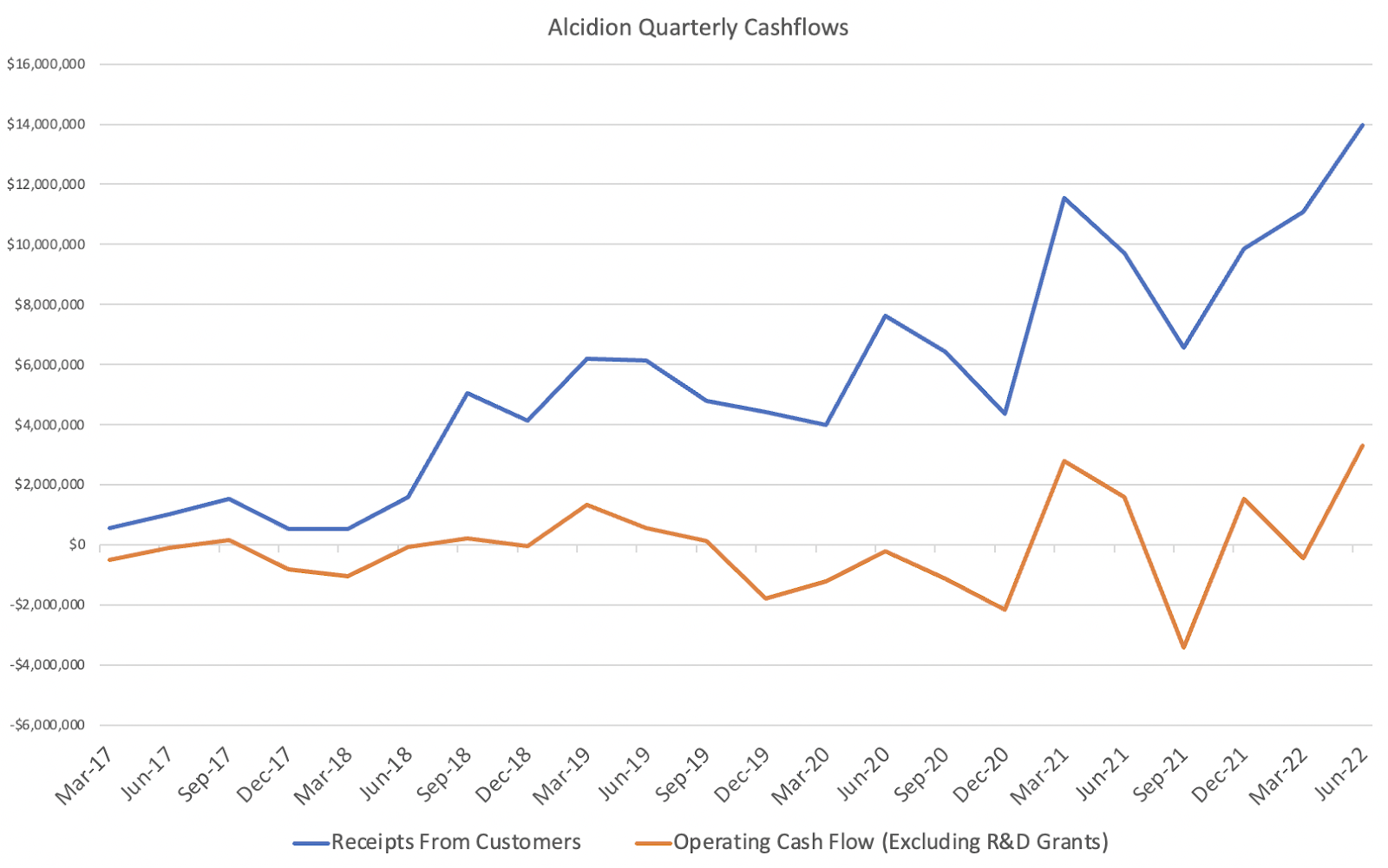

At the time of writing, we’re still waiting for Alcidion’s FY 2022 audited results. However, we do have its quarterly cashflow statement to June 2022. The latest quarter was Alicidion’s strongest ever quarter in terms of both receipts from customers of almost $14m and operating cash flow of about $3.3m. For the full year, Alcidion was narrowly free cash flow positive, if you ignore acquisition payments. That said, it is also worth noting that cashflow is lumpy and from the look of the chart below, Alcidion is due a weak quarter.

FY 2022 represents an important milestone for Alcidion because the company can report positive unaudited underlying FY22 EBITDA (excluding M&A costs). On top of that, the company has long promised to reach profitability in FY 2023, though it’s not entirely clear whether it will make a net profit after tax, or just a positive EBITDA. Either way, the FY 2022 result lends a lot of credibility to the idea that Alcidion will not need to raise capital to fund its growth (or keep the lights on).

The company says that “Based on current unaudited results, Alcidion is expected to report FY22 revenue of at least $34.0M, a 31% increase on pcp, including $4.3M of Silverlink revenue.” Even if we remove the acquired Silverlink revenue, Alcidion would have revenue of about $29.7m in FY 2022, up about 15% on revenue of $25.9m in FY 2021.

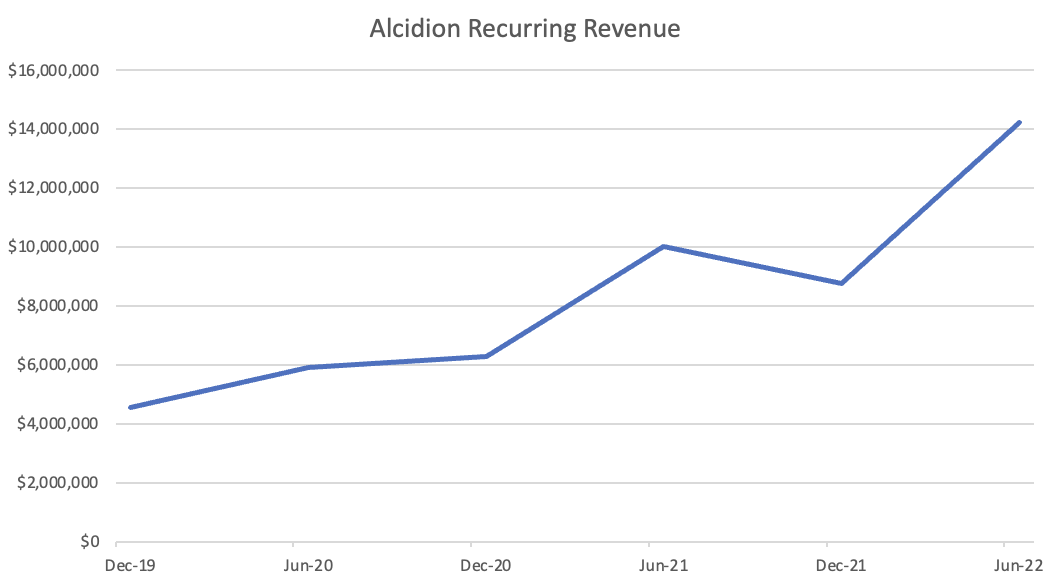

Product revenue is recurring in nature, albeit not necessarily on an annual basis, and came in at $23m in FY 2022. This implies just under $14.3m for the second half, as shown below. Even if $4.3m came from Silverlink, recurring revenue excluding Silverlink was at least as high as the second half last year.

Looking forward, Alcidion already has $28.3m in contracted revenue for FY 2023, with another $2.9m likely, for a total minimum expected revenue of $31.2m. In the last few years, Alcidion has finished the year with anywhere from about $7m to about $15m extra revenue compared to its contracted revenue at the start of the year. This has benefitted from acquisitions, but if we conservatively assume just $6m of revenue from additional contract wins, that would give us $37.2m in total FY 2023 revenue. Given the company is already approximately breakeven, even this revenue growth of about 10% could easily produce a small profit of under $2m.

Then, if the company maintains cost discipline, another year of modest growth could see a profit before tax of around $6m or more in FY 2024. Given accumulated losses, I wouldn’t expect Alcidion to pay much tax on this initially. At the current price of 16c Alcidion has a market cap of around $200m. By the end of 2024, I’d expect a slightly higher cash balance than the current $17.4m, absent an acquisition, so you could call the forecast enterprise about $180m assuming $20m cash.

Using earnings before interest and tax (EBIT) that would give us an EV/EBIT multiple of about 33. This implies continued growth going forward. Given the potential for operating leverage in a software business, and Alcidion’s fairly attractive growth prospects, it is not difficult to imagine Alcidion doing 25% EBIT margins on revenue of $60m, within a few years. That would imply $15m in EBIT. Even assuming a tax rate of 30%, that would be NPAT of about $10.5m, implying a P/E ratio of about 19 at the current share price. While I’m not saying that’s what will happen, I do think this thought experiment illustrates how a few years of growth and good management could make the current price tag for Alcidion look quite attractive.

Risks To Alcidion

The biggest risk for Alcidion shareholders is that it isn’t on a path to sustainable profitability. Even though the company will breakeven on an underlying EBITDA level, we still don’t know when it will become profitable. Ideally, that should occur in FY 2023, but it isn’t guaranteed. We also don’t know if management will consistently grow profit, or just look to operate around breakeven while investing in growth.

Alcidion’s main markets in UK and Australia rely on government departments choosing to modernise hospital health systems using Alcidion’s technology. At present, Alcidion is able to successfully grow within the prevailing procurement frameworks. However, political changes could potentially slow the roll out, favour alternatives, or try to bargain down prices. This could cause revenue growth to slow, effectively preventing growth.

Alcidion has made several acquisitions throughout the years. If these businesses face structural or systemic barriers to profitable growth, or prove difficult and costly to integrate, they could end up causing trouble. And even assuming the business performs well, one could argue that Alcidion has paid quite high prices to acquire its Silverlink, for example.

Generally speaking, integrating a diverse set of separate software solutions is a difficult task, which often has more technical debt relative to a single solution developed organically by the same team. Technical debt essentially results from development teams expediting delivery of functionality which later needs to be refactored. In other words, it’s the result of prioritising speedy delivery (or integration of existing code from different sources) over perfect code.

Why I Think Alcidion Stock Is Worth Buying

Alcidion improves outcomes for patients by maximising the chance that nursing staff will process test results in a timely manner and observe patients as appropriate. Nursing staff are overstretched in both Australia and New Zealand and there is an acute need for any kind of system that can ease the administrative burden. One way to help is to improve the level of automation and assistance provided by computers.

Last year Alcidion was small growth software stock with a soaring share price but no profits. Since then, the share price has fallen but the actual results have continued to improve. The next quarter likely to be weaker than this (fairly impressive) quarter, so I wouldn’t be surprised if I get a better opportunity to buy Alicidion shares later in the year. That said, I still think that the shares offer an attractive balance of risk and reward yesterday’s closing price of 15.5 cents per share, and I intend to increase my position size. I am expecting Alcidion to make a small profit, or come very close to profitability, in FY 2023. If it falls short of that, I might sell my shares.

Mach7 Technologies (ASX: M7T)

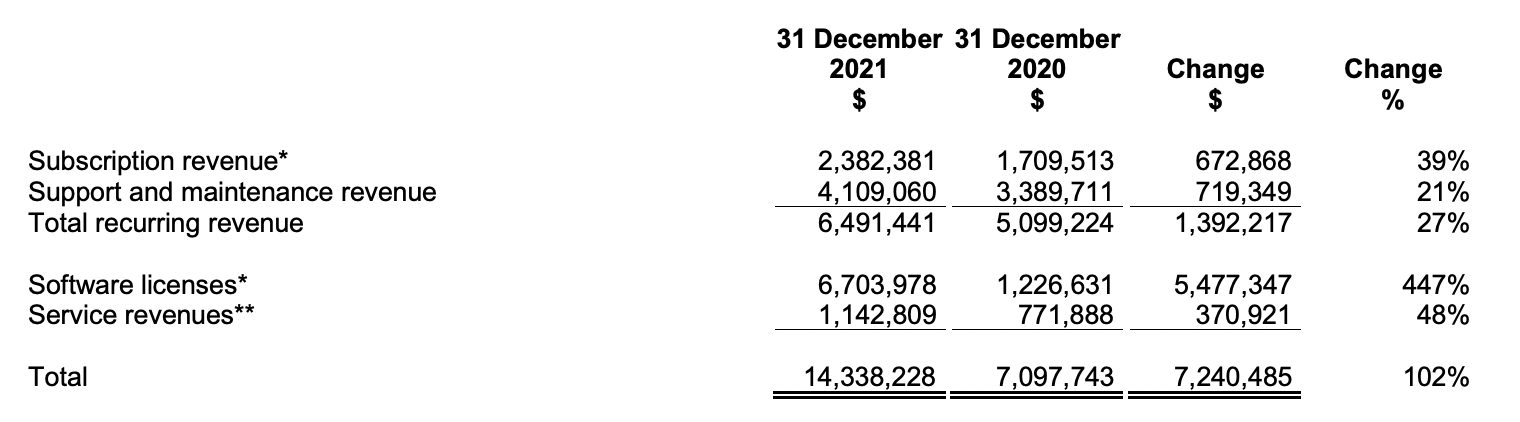

Mach7 (ASX: M7T) was founded by Rudy Sugiarto and current CTO Ravi Krishnan, who previously worked at medical imaging technology heavyweight Agfa. Mach7 provides enterprise radiology imaging solutions, such as file storage or image viewing software to over 150 customers, mainly hospitals and radiology networks, in 15 countries.

In the last half year results (H1 FY 2022) Mach7 produced revenue of $14.3m and a loss of almost $0.5m. Its market capitalisation at the current price of 68c cents per share is about $163m. It had cash on hand of $25.8m at 30 June 2022.

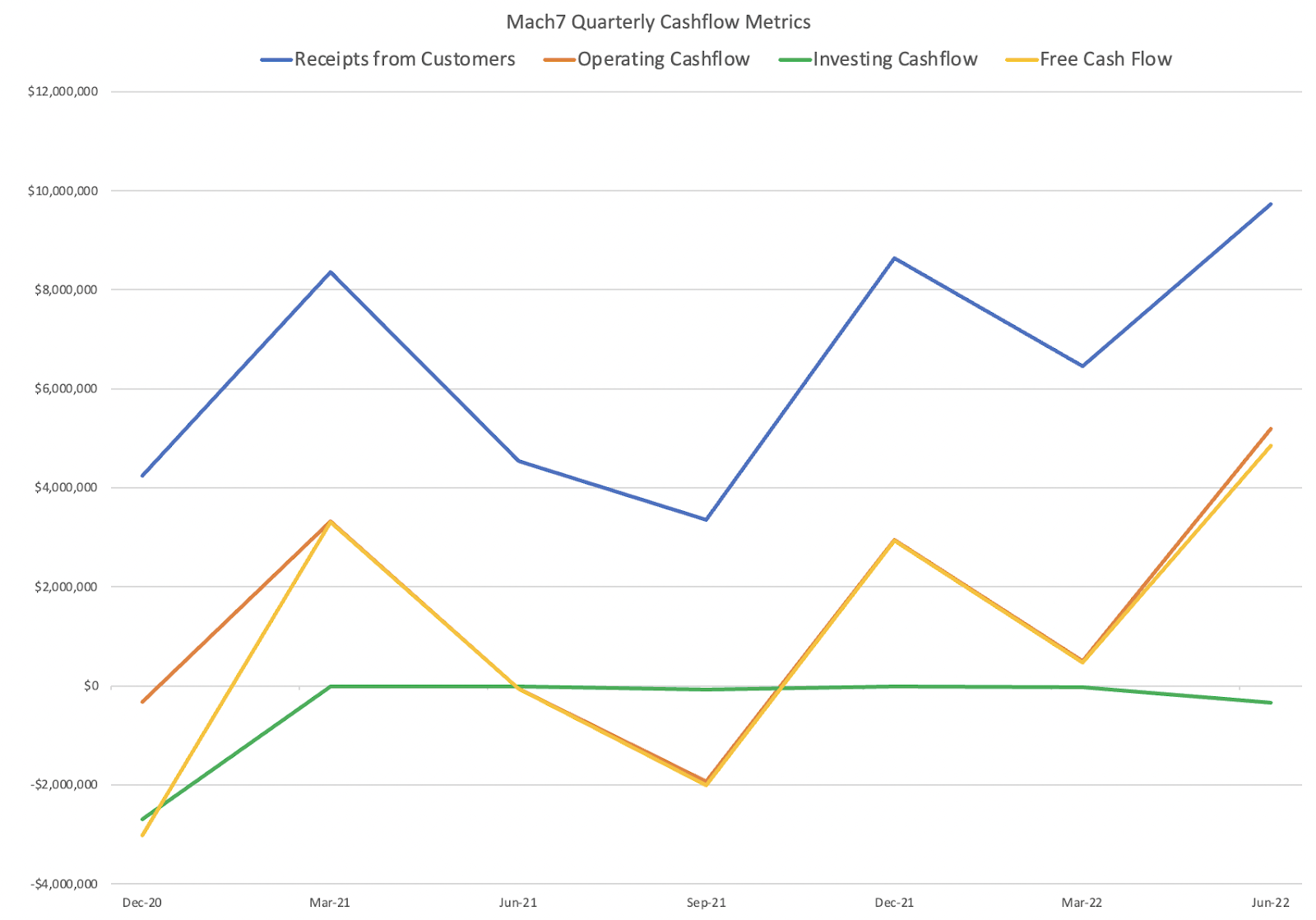

When it comes to cash flow, the last three quarters have all seen the company produce free cashflow. However, the September quarter is generally a weaker quarter for cash receipts, so it is possible cash burn will resume in the next quarter.

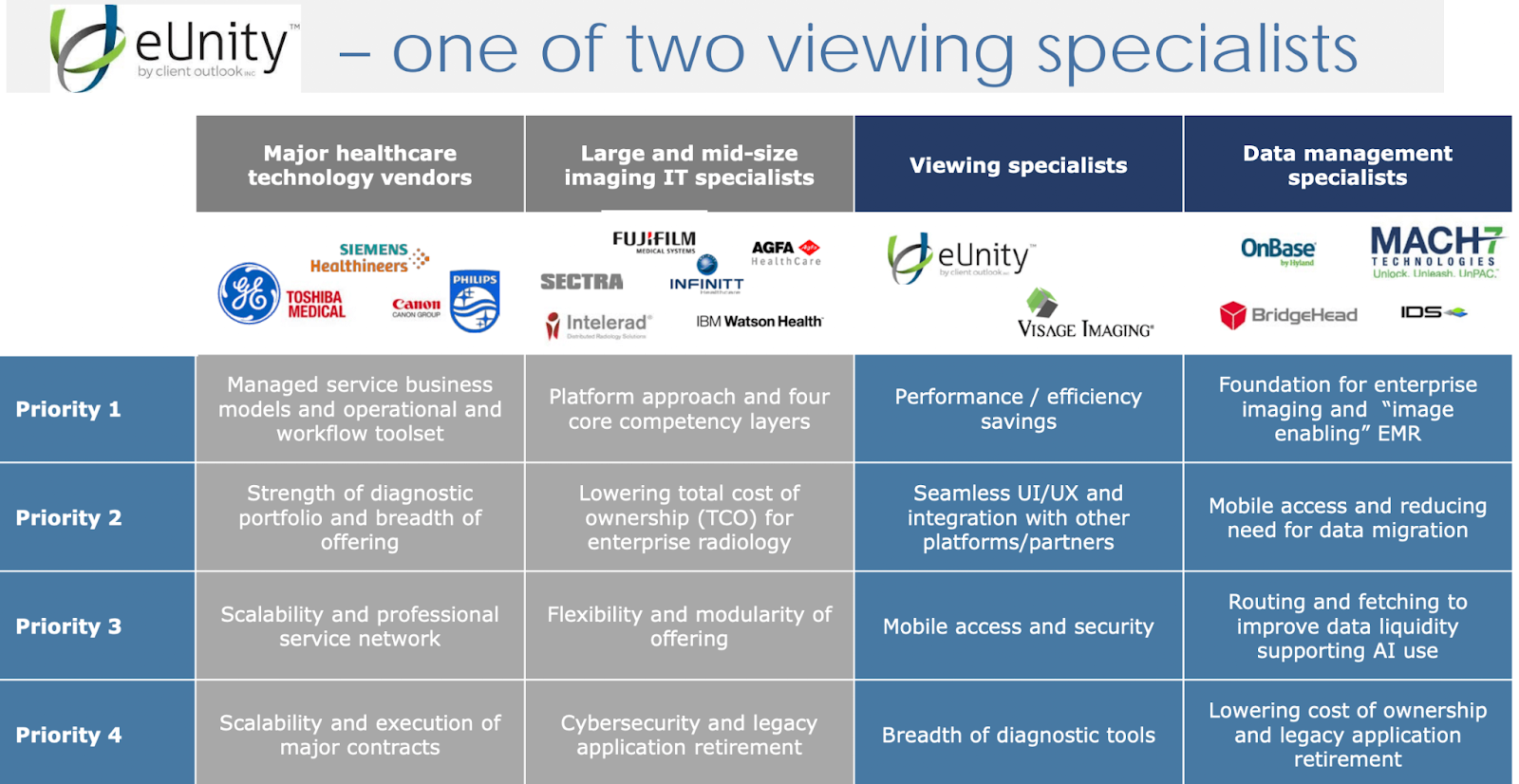

The 2016 presentation containing the image above above also states that “Mach7 deconstructs PACS by consolidating archiving and communication across an enterprise while enabling departmental picture systems (eg Viewers) to plug into the platform”.

Picture Archiving and Communication Systems (PACS) used to be sold by a single vendor but now the different elements such as the Archive and the Viewing Software can be sold separately, with different vendors having interoperable software. Back in 2016, Mach7 had a distribution arrangement with eUnity to re-sell their viewer. However, in 2020 Mach7 bought Client Outlook, the developer of eUnity for $40.8m, funded by a placement and entitlement offer at $0.68. Since then, it has provided viewing software as well as enterprise imaging platforms.

Today, Mach7 offers the eUnity viewer, universal work list software, and enterprise data management (which is essentially a vendor neutral archive), putting it in competition with a stock I already own, Pro Medicus (ASX: PME).

When you compare the two companies side by side, Pro Medicus looks like the higher quality business. First of all, it has the more impressive customer list. More importantly, I believe it can charge considerably more for its software. Having first bought shares at under $1, my legacy holding in Pro Medicus is significant and will likely outweigh any position in Mach7. The important question here is whether competing with Pro Medicus is such a bad thing.

Given that Pro Medicus tends to focus on a premium offering for the best and biggest hospitals, it’s likely that it will become more powerful over time. The access Pro Medicus has to top academics working in the fields of radiology and artificial intelligence is an advantage.

That said, Pro Medicus keeps its prices high to ensure it can efficiently monetise the value its superior software creates for those hospitals that can afford to make the investment. In the last half Pro Medicus had an earnings before interest and tax (EBIT) margin of 66%. If Mach 7 had an EBIT margin of just half that, being 33%, it would have made EBIT of about $4.7m on revenue of about $14.3 million. Instead it made a loss of just over $400,000.

At the end of the day, even though I think Pro Medicus will capture the best and most valuable clients, I believe that both companies should benefit from the “deconstruction” of PACS. This essentially means that hospitals are moving to a system where different vendors can provide different elements of the system. As I understand it, Pro Medicus’ Visage could technically be used to view images on Mach7’s vendor neutral archive (or a legacy storage system).

Previously, hospital clients would be beholden to a single PACS vendor. Due to the trend to deconstructing these systems, companies with more modular “deconstructed” offerings have been gaining market share, because their systems do not lock the hospitals in to an ecosystem. You might think that by offering different elements of the PACS system, vendors like Pro Medicus and Mach7 are not really deconstructing the PACS tech stack. However, the key here is that interoperability means that hospital clients are not locked in to the eUnity viewer, even if they want to keep using Mach7’s vendor neutral archive.

I think that there is room for both Mach7 and Pro Medicus to both build attractive businesses as providers of various parts of the deconstructed PACS technology stacks.

Risks To Mach7 Technologies

One of the real weaknesses in Mach7’s business model is that most of its revenue is not recurring in nature. Instead of charging a subscription or per transaction, most of Mach7’s revenue is software licenses or one-off service revenue (often related to implementation).

This means that its cash receipts (and profits) can be quite up and down, given the timing of license fee payments.

The biggest risk with Mach7 is that the company is not really on a path to sustainable profitability. Even though the company looks like it will become profitable, the lumpiness of its business means it could go backwards. For example, the CEO Mike Lampron said on the recent quarterly investor call that he isn’t expecting so much renewal revenue in FY 2023, so the company will have to make up that deficit with new customer wins. Even assuming Mach7 does make a profit, we don’t know management will consistently grow profit in the years ahead, or just look to operate around breakeven while investing in growth.

If it turns out that the market for radiology archives and viewers is more competitive than I thought, Mach7 may be unable to achieve satisfactory EBIT margins, even at maturity. The fact that Pro Medicus is extremely profitable does not mean that all players in the space will have high margins. It is possible that once you drop back from being the very best radiology imaging viewer provider, the field is much more competitive, and the margins are much lower.

Edit: There is also the case of a patent dispute with AI Visualize to consider. Mach7 has won the first round though AI Visualize can appeal. From the outside, this appears to be a case of patent trolling (I cannot see any customer list for AI Visualize). If so, that is unfortunate for Mach7 and is perhaps a reason for caution. It is difficult to predict what courts will find, and defending the allegations is a cost for Mach7, but it seems unlikely and older company with real customers has stolen the technology of a newer company without customers listed on its website.

Why I Think Mach7 Stock Is Worth Buying

My view is that deconstructed picture archiving communication systems (PACS) add a lot of value to their clients by making radiology faster, cheaper, and more accurate. Pro Medicus is able to sell Visage for a premium because of its speed, accuracy and (to a degree) its functionality. Mach7 may not be able to win the biggest and best clients, but it has still managed to build a substantial business. The business already has annualised recurring revenue (ARR) of $14.4 million, and the CEO said on the recent investor call that the business is “edging closer… towards the side of more subscription and recurring models”.

Over the next few years, there is an opportunity to move clients from an up-front license sale model to a more regular subscription or usage based model. Going forward, some clients, especially government clients, might want to stick with the license model. Either way, I think that most clients will be fairly sticky, and recurring revenue should keep growing.

In the recent quarterly update, Mach7 said that the $14.4m in ARR “is now covering approximately 65% of the Company’s annual operating costs,” indicating about $22.2m in operating costs. Mach7 expects to grow recurring revenue by another $2.9m based on contracts it has already signed. That would bring ARR to $17.3m.

The company is optimistic about “FY23 Sales Orders target is expected to be around $36 million, which is 20% more than the FY22 target of $30million.” When it comes to revenue, Mach7 is forecasting around $27m for FY 2022, and says “Looking forward to FY23, the Company expects to see strong double digit growth again.” The company’s confidence in growth comes from the fact that, at the customers, two deployments have been staged to run in parallel with deployments from other providers. This could put Mach7 in the position to be profitable in FY2023.

Due to its reliance on license sales, Mach7 is unlikely to be able to consistently grow profit over the years. Having said that, it does like like its on the verge of making its first profit, after quite a few years of trying. As I write, the share price of 68c is the same as what investors paid years ago when Mach7 bought eUnity. Since then, the strategy has found some success and the cash flow has improved markedly. I think FY 2023 could be an inflection point for Mach7 in terms of its profitability, so I plan to buy some shares around the current price.

Please remember that these are personal reflections about stocks by an author, and this article is not intended as a recommendation. The author owns shares in Alcidion already, and plans to buy shares in Mach7 after publication of the article. By the time you are reading this, I may already own shares in Mach7 (see disclosure above). The author owns shares in Pro Medicus.

This article is an investment diary valuable only for the cognitive process it demonstrates. Any advice contained in this article is general advice only. The author has not considered your investment objectives. Any statements of advice above are authorised by Claude Walker (AR 1297632), Authorised Representative of Equity Story Pty Ltd (ABN 94 127 714 998) (AFSL 343937)

Save time at tax time: If you’d like to try Sharesight, please click on this link for a FREE trial. It saves me heaps of time doing my tax and gives me plenty of insights about my returns. If you do decide to upgrade to a premium offering, you’ll get 4 months off your subscription price (the best deal available, I’m told) and we’ll get a small contribution to help keep the lights on.

The information contained in this report is not intended as and shall not be understood or construed as personal financial product advice. You should consider whether the advice is suitable for you and your personal circumstances. Before you make any decision about whether to acquire a certain product, you should obtain and read the relevant product disclosure statement. Nothing in this report should be understood as a solicitation or recommendation to buy or sell any financial products. A Rich Life does not warrant or represent that the information, opinions or conclusions contained in this report are accurate, reliable, complete or current. Future results may materially vary from such opinions, forecasts, projections or forward looking statements. You should be aware that any references to past performance does not indicate or guarantee future performance.