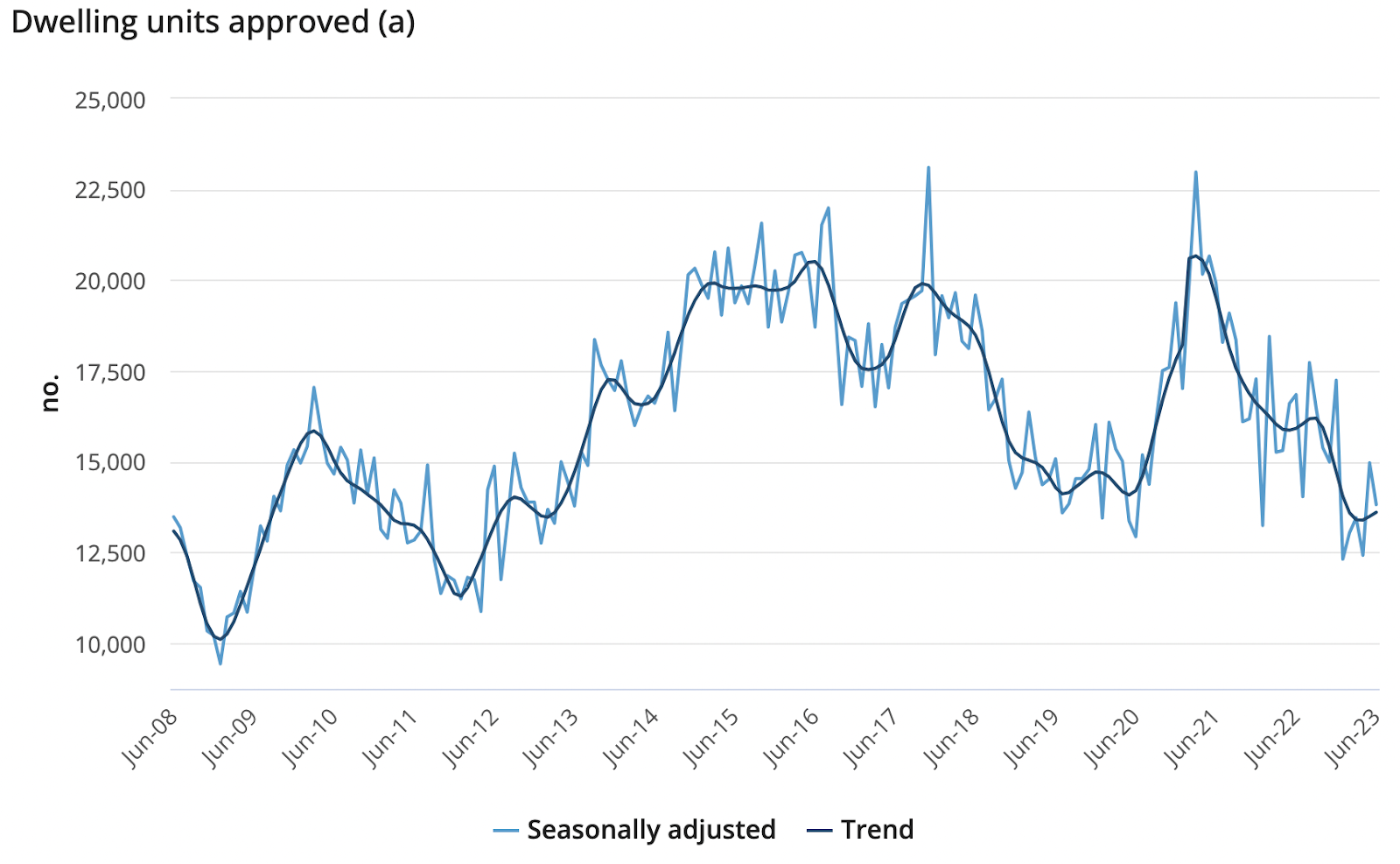

Australia’s building industry has been particularly affected by increased costs and higher mortgage rates, and it appears tough times will persist in the near-term.

Although building approvals rose 20.6% in May, in seasonally adjusted terms, the overall trend remains downward. While the Reserve Bank kept rates on hold at their most recent meeting, we could see further rate rises as inflation is still well above the desired level. Further impacting sentiment around construction companies is the risk of builders going into administration, as well as inflating building costs.

Source: Australian Bureau of Statistics

While I am in no hurry to buy construction company shares in the current economic environment, I am still keeping an eye out for opportunities, particularly for those companies that will benefit when inflation falls. The following two small ASX listed construction companies are on my watchlist due to solid revenue growth and the potential to benefit from improved conditions in the construction industry.

Big River Industries Limited (ASX: BRI)

Big River Industries is an Australian building materials distributor, supplying timber, hardware, building supplies and services for the residential, commercial, industrial building and construction industries. It supplies building materials to a wide variety of customers (with over 9,000 direct to market channel accounts).

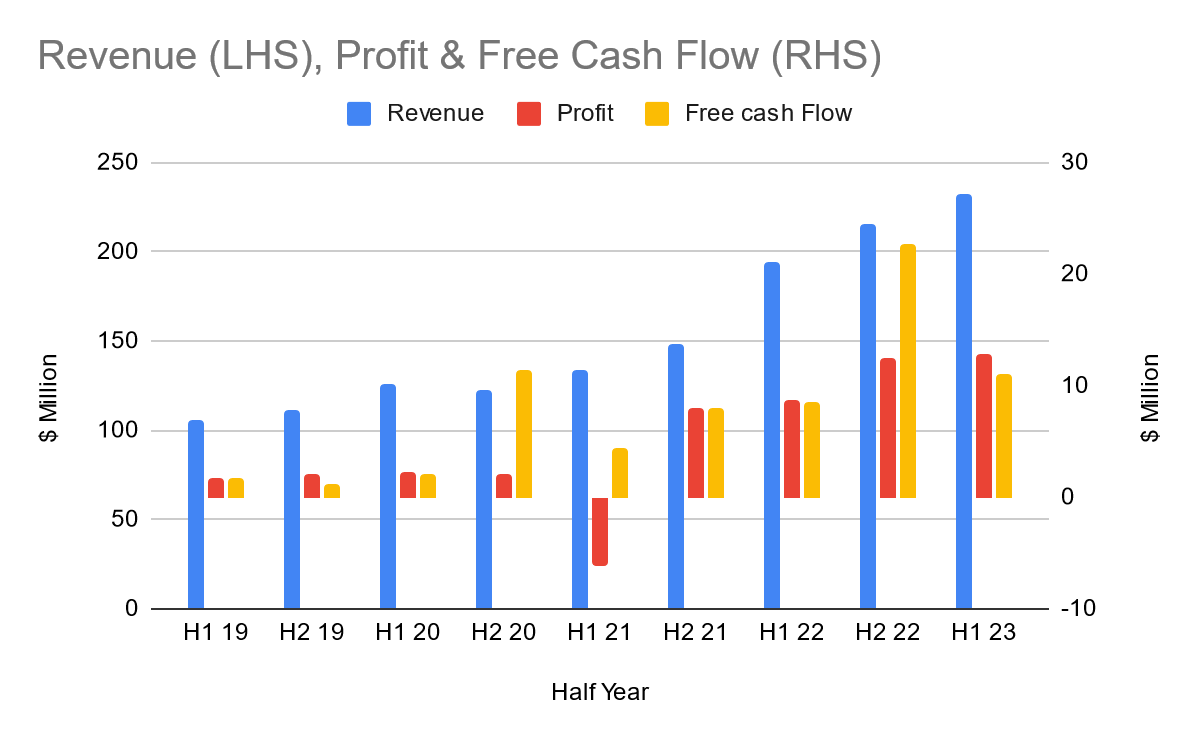

Big River Industries H1 FY 2023 Results

Since listing in 2017 Big River has seen consistent revenue growth. The half year to December 2022 saw revenue of $232 million, up 19.9% on the prior corresponding period. Organic growth accounted for 10.8% of this with the balance coming from the two recent acquisitions. Trade centers accounted for 44% of revenue, 27% from formwork, and 29% from panels.

Net profit after tax was up 5.8% to $12.8 million, and free cash flow was $13.9 million, which was cash from operating activities, minus expenditure on property, plant and equipment.

Big River Industries Acquisitions

During the half, panels and roof tiles supplier FA. Mitchell & Co. was acquired for $598,000 in cash, and contributed revenue of $1.8 million and $0.1 million to net profit after tax, for five of the six months.

Timber and building supplies company Epping timber was acquired for $6 million in cash, and contributed $1.5 million to revenue and $0.1 million to net profit after tax, over a month.

Risks to Big River Industries

Some builders are going into administration, which means lower demand for materials in the short term, but this will create a backlog of work that will still need to be completed in the future.

Big River is aiming to complete ~2-3 acquisitions per year, which could mean equity dilution. Big River had $16.9 million in cash at 31 December 2022, and may be wary of borrowing as interest rates could move higher. Inflation at 7% is still well above the Reserve Bank’s target band of between 2-3%.

Big River Industries (ASX: BRI) Director Ownership

There have been no on-market director trades over the last year, although directors that own shares are reinvesting via the dividend reinvestment plan. Managing Director and Chief Executive Officer John Lorente owns 172,023 shares. Independent Non-Executive Chairman Malcolm Jackman owns 135,340 shares. Non-Executive Director Martin Monro owns 27,104 shares. Non-Executive Director Vicky Papachristos owns 34,968 shares, and Non-Executive Director Brad Soller owns 13,552 shares.

At the time of publication, the Big River Industries share price is around $2.51, so most of these holdings would be worth significantly less than a small apartment in a capital city.

Big River Industries (ASX: BRI) Share Price and Outlook

At the current Big River Industries share price of $2.51, Big River has an undemanding trailing price to earnings ratio of around 8.2, which is lower than most of its larger peers in the building industry. Big River Industries’ trailing twelve months dividend yield is a generous 7.4%, fully franked.

Big River Industries is a small cap, looking to entrench itself further into Australia’s building supplies industry by adding to its diverse range of products, outlets and direct client accounts with acquisitions over the coming years.

Short-term the building industry is weak, but longer-term a housing shortage and rising migration bodes well for the company, so I will be keeping a close eye on Big River.

Acrow Formwork and Construction (ASX: ACF)

Acrow provides engineered formwork, scaffolding and screen systems, as well as in-house engineering and industrial labor.

Acrow is now earning a larger percentage of revenue from the higher margin engineering systems and services. Acrow tripled its engineering team over the last four years, and its increased engineering capabilities have been a driver of growth. Acrow should benefit from an increase in civil infrastructure activity on the east coast in the coming years.

Acrow H1 FY 2023 Results

For the six months to December 2022, Acrow reported revenue was up 14% on the prior corresponding period to $79.2 million. Underlying Net Profit after Tax was up 43% to $10.49 million. Profit growth was achieved across all three divisions. Free cash burn was $3.3 million from operating cash plus proceeds from disposal of property, plant and equipment minus expenditure on property, plant and equipment. This demonstrates that Acrow is quite capital intensive.

Over the half, net debt rose by $4.6 million to $37.4 million, primarily due to the capital investment for growth initiatives, and the shift into Jumpform (type of formwork used for constructing large vertical concrete structures, such as high-rise buildings). Net gearing increased 0.6 ppts to 28.9%, net debt to EBITDA remained flat at 1.1 times and interest cover was 13 times for the period. Cash on hand reduced over the period to $1.73 million.

Acrow Formwork (ASX: ACF) Guidance for Financial Year 2023

Acrow now expects financial year 2023 Underlying Net Profit Before Tax (UNPAT) to be 7% higher at $29.5m – $30.5m, driven by trading performance and acquisitions.

Acrows Recent Acquisitions

In May Acrow acquired Heinrich’s Ishebeck Formwork Panel System for $12 million, funded through cash and debt. Previously it acquired the screens business. Together, these acquisitions are expected to contribute ~$9.5m to Acrow’s EBITDA in FY24, for a combined outlay of up to $23.5million.

Risks to Acrow Formwork

Acrow is still capital intensive as expansion requires more hire equipment and maintenance to support growth. However, its net margins have increased significantly from 4.26% in H1 2021 to 14.08% in H1 2023, as the higher margin engineering services business makes a greater contribution.

If the Reserve Bank has to raise interest rates further to get on top of inflation that would likely impact Acrow’s profit through increased financing cost, while inflation may continue to increase working capital requirements.

Acrow is partly dependent on government infrastructure spending, and if there was a pause in spending it may affect Acrows revenue. Though this appears less likely at present due to the large budget surplus, transport infrastructure spending (mainly on the east coast) is set to be scrutinised by the Labor government after it inherited more than 700 projects from the Morrison government, that it claimed were not economically viable.

Bad debts increased over the six months to December 2022, but only accounted for 1.5% of revenue. However, bad debts could become a more serious threat if Australia goes into a recession.

Outlook for Acrow Formwork (ASX: ACF)

The Acrow share price has pulled back after a strong run and trades on a trailing price to earnings ratio of 11.8, and dividend yield of 3.9%.

Acrow has a strong pipeline of work, including significant projects such as Snowy Mountain 2.0.

Some investors may still think of Acrow as primarily a scaffold hire company, but it has shifted into the more specialised and higher margin formwork, and engineering services. This may partly explain why Acrow has remained under the radar of investors with a low price to earnings ratio. Being viewed as a cyclical company also keeps the price to earnings ratio lower.

Chief Executive Officer Steve Boland purchased $144,600 worth of shares on-market in mid-June, as the price pulled back, and he has bought shares on-market in the past, too.

While I think this is a good company, I will be waiting to see how the battle to control inflation plays out, before considering purchasing shares.

Sign Up To Our Free Newsletter

Disclosure: neither the author of this article Chris Coe, nor the editor Claude Walker own shares in ACF or BRI and neither will trade in those shares for at least 2 days following the publication of this article. This article is not intended to form the basis of an investment decision and is not a recommendation. Any statements that are advice under the law are general advice only. The author has not considered your investment objectives or personal situation. Any advice is authorised by Claude Walker (AR 1297632), Authorised Representative of Equity Story Pty Ltd (ABN 94 127 714 998) (AFSL 343937).

The information contained in this report is not intended as and shall not be understood or construed as personal financial product advice. You should consider whether the advice is suitable for you and your personal circumstances. Before you make any decision about whether to acquire a certain product, you should obtain and read the relevant product disclosure statement. Nothing in this report should be understood as a solicitation or recommendation to buy or sell any financial products. A Rich Life does not warrant or represent that the information, opinions or conclusions contained in this report are accurate, reliable, complete or current. Future results may materially vary from such opinions, forecasts, projections or forward looking statements. You should be aware that any references to past performance does not indicate or guarantee future performance.