One of the most successful investment biases over the last decade has been to find “high quality” businesses with good long term track records. But before we take a look at some examples, I have to unpack what I mean by “high quality” businesses. My personal definition requires:

- Ability to invest in growth at high returns on invested capital (15%+)

- A sustainable competitive advantage that is strengthening over time

I don’t believe everyone shares this definition, and some might quite reasonably include a free cashflow component. However, I would consider free cashflow more heavily when discerning whether the company is trading at a reasonable price, or if it is too expensive to buy right now. I think of pricing power as a key marker of competitive advantage, and I look at longer term averages of return on equity, return on invested capital, and return on assets to discern the ability to invest in growth at high returns.

So, based on my criteria above, I thought I would share three companies that might interest you.

REA Group (ASX: REA)

REA Group is the owner of realestate.com.au, and has a very impressive track record of growth. We covered REA Group’s H1 FY 2024 results in detail but zooming out, there is clear evidence it is a high quality company.

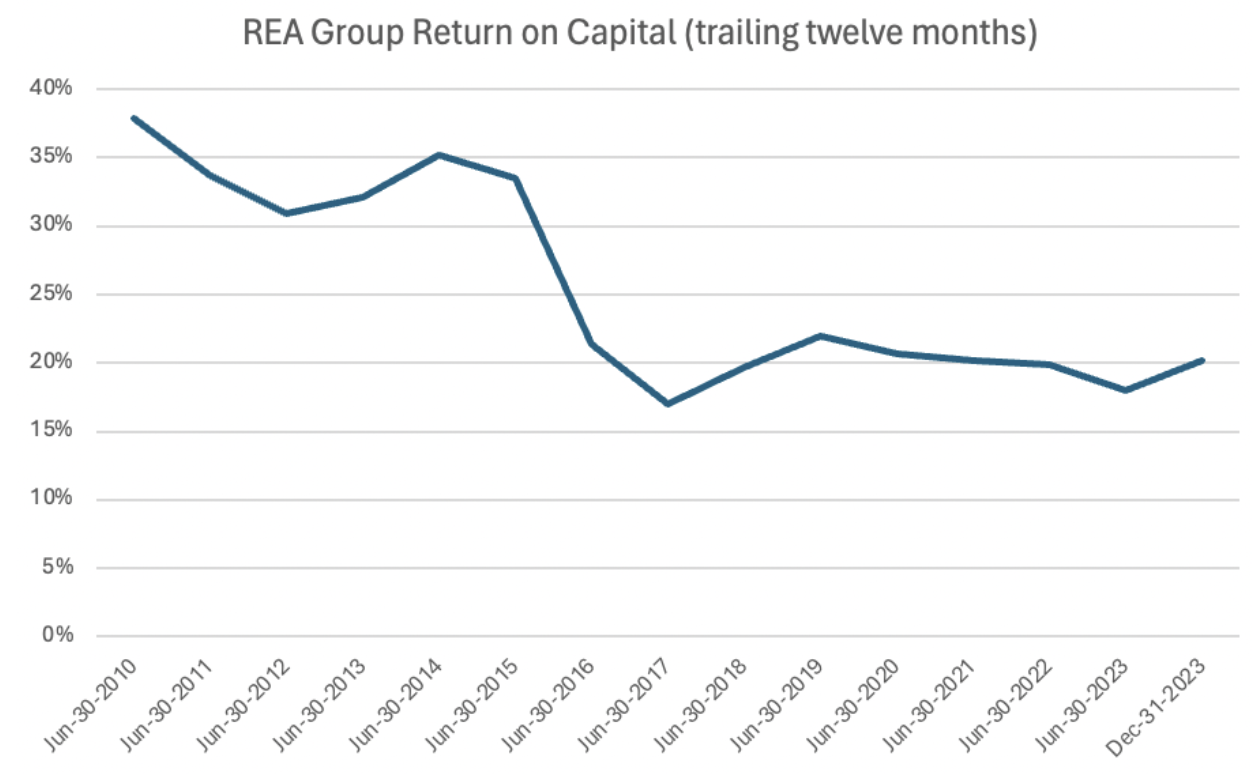

First of all, in the chart below, you can see that the company’s return on capital has been persistently high.

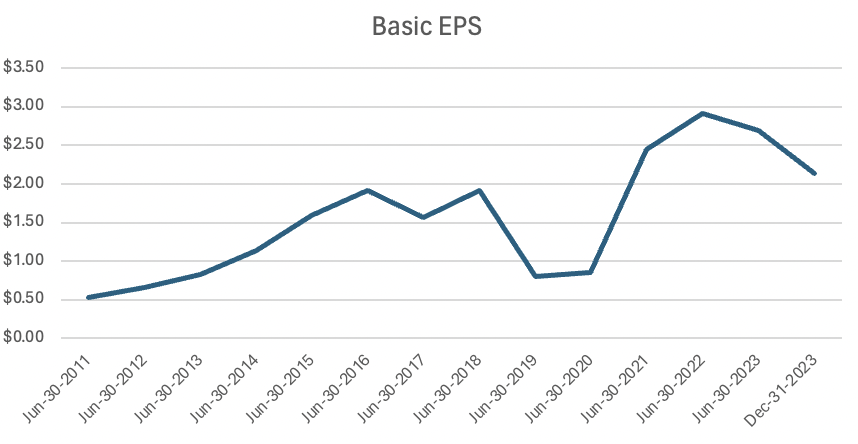

Second, you can see that there has been some strong earnings per share growth over the long term, even though the company has suffered its ups and downs, over the years. Notably, the poor result in FY 2019 was due to a write-down of the Asian operations.

To me, these long-term results suggest that the company’s investments in its brand and products have yielded positive results. Arguably, its overseas investments (especially in India) will be a big factor in returns going forward, so the future will of course look different from the past. However, the financials certainly support the other evidence that indicates that realestate.com.au has genuine reinvestment potential.

When it comes to pricing power, it is very obvious that realestate.com.au shines. Not only is it able to put up prices, but when real estate agents complain about it, they still have to use the website because their own clients expect it. Going forward, the company is expecting to be able to continue to flex pricing.

On the H1 FY 2024 results conference call, the CEO said:

“…I’m not going to flag what’s going to happen in ’25 until we’ve announced our price. I mean, price will be a fair driver in ’25 for sure. But alongside that price is value. And we’d like so much of our yield growth this year is customers choosing to buy more premium products. And we always want to be able to do that to them. So again, I’m not going to flag what we’re going to release in terms of product and features. But it will be a combination, I would think, of further choice in premium products together with roll price, will drive our revenue growth into next year.”

Finally, my biggest concern about REA Group is that it does seem to becoming less popular with employees. After making a big show of employee flexibility at the start of the pandemic, REA Group is progressively enforcing “return to office” policies that some employees find very jarring and counterproductive.

With a trailing P/E ratio of around 55 and a dividend yield of about 1%, REA Group will need to keep growing for many years. Its track record suggests this is possible, but incurring unnecessary commercial lease costs while potentially upsetting and demotivating the workforce seems suboptimal.

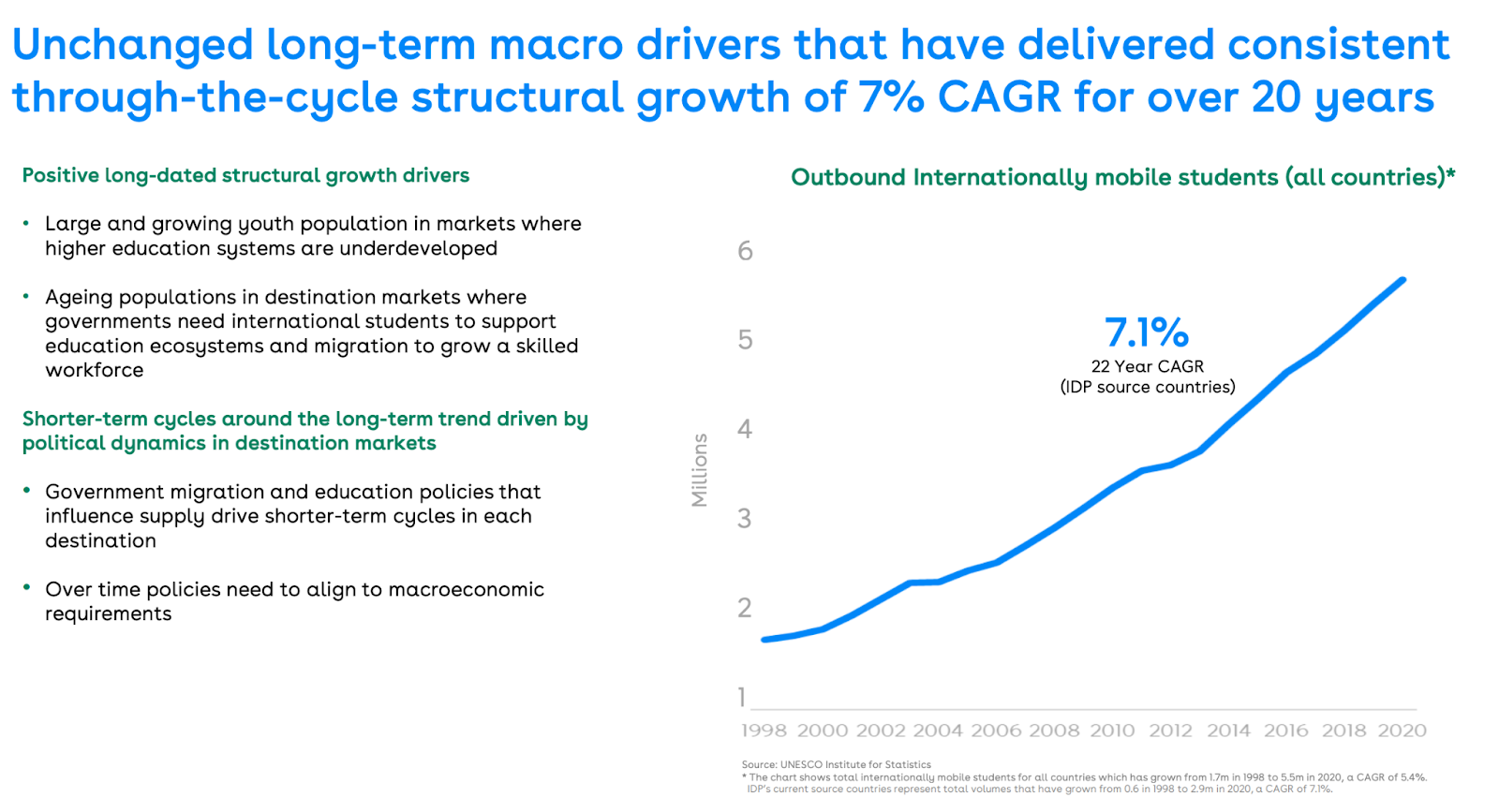

IDP Education (ASX: IEL)

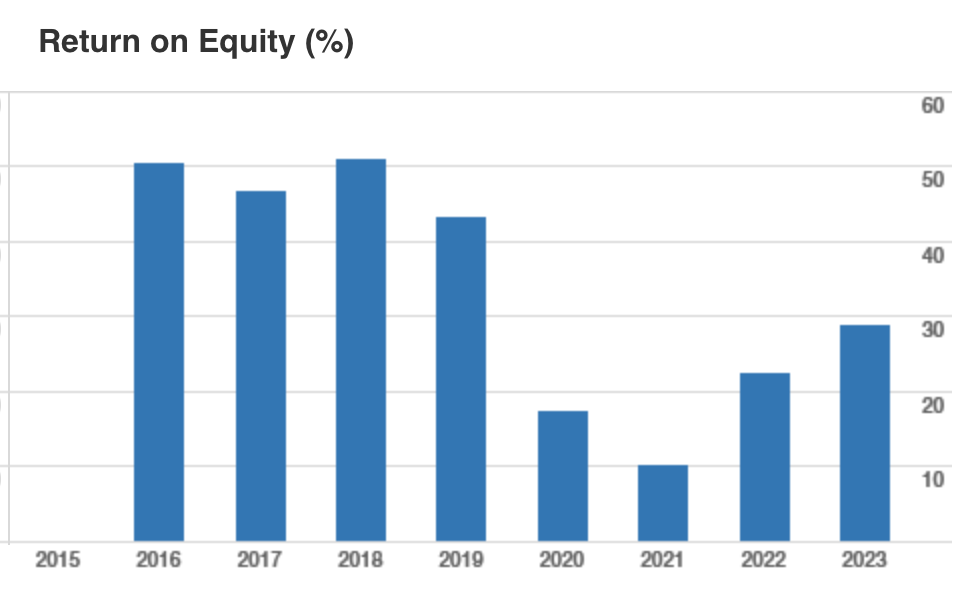

IDP Education essentially sells qualifications (in particular, as part of an immigration process). This means it can achieve very high returns on equity, because the business scales very well. In the graph below, the dip in ROE related to the pandemic’s impact on immigration.

Because IDP Education only competes with other government certified educational institutions, it can charge prices far in excess of its cost of actually educating students; net profit margins of over 15% are a testament to this fact. However, this pricing power may be eroding, since Canada announced it would open up its market for English tests for students wanting a visa to rival companies.

It is uncertain how badly this undermines pricing power. The CEO commented after the H1 FY 2024 results that “…we’ve seen the new competitors for Canada focusing primarily on network expansion and marketing. And the really important callout here is that pricing has remained rational.”

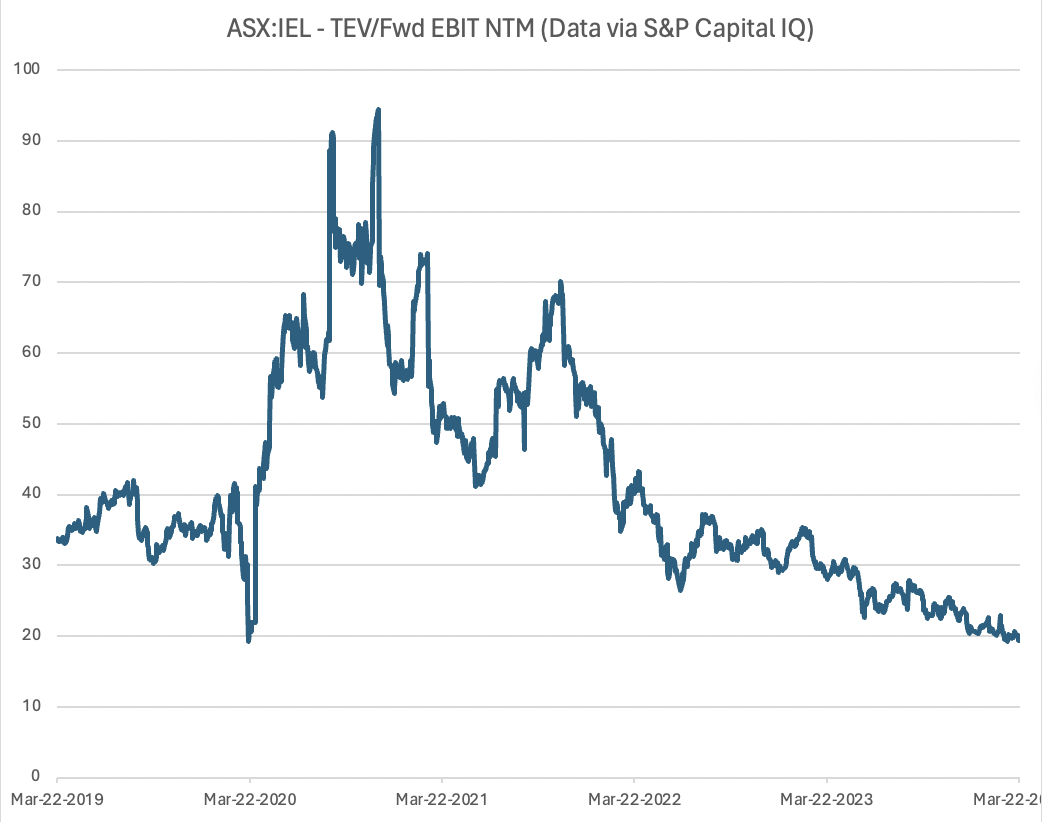

Nonetheless, concern about weakening pricing power has helped push EDP Education down to 5-year lows in terms of near-term estimated Enterprise value to Earnings Before Interest and Taxation multiples.

Ultimately investors need to consider whether the need for young workers in fatter, older and richer countries will overwhelm the impact of potentially increasing competition. My view is that the rational approach is for operators to not compete on price, but that remains to be seen.

You can see that the company itself advertises “through-the-cycle structural growth” so there is at least an argument that the company will continue to find opportunities for investment in growth at attractive returns.

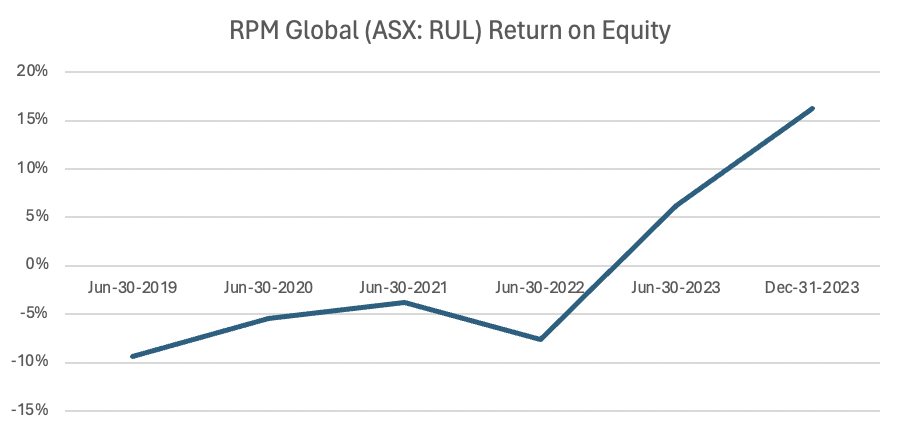

RPM Global (ASX: RUL)

RPM Global is a more nuanced submission to this category of 3 high-quality compounders that have a long track record of success. The main reason for that is that while (in my opinion) the underlying business performance has been successful, the high quality nature of the business is only just beginning to emerge. You can see how the company has just begun to demonstrate the kind of return on equity that I think is likely to be sustainable, going forward.

Nonetheless, it does seem that RPM Global is able to grow by developing and selling new products, and going forward, that is likely to be highly profitable (after a few years running the business at a small loss).

Another complicating factor is that RPM Global has a high quality software business and a lower quality consulting business, so it is not clearcut how easily it can reinvest in growth at high ROI… but it is likely the software business offers that opportunity.

However, that said, it is more clear that the company has some pricing power. On the recent analyst call the CEO said:

“But there certainly is pricing power in the asset management. And so these are bigger product. XECUTE is a bigger product. So the more value you add to the customer, then generally, the more you can charge. So it’s sort of not much more to say about pricing than that.”

The other reason I think there is pricing power is that enterprise software often does have pricing power, especially when it is core to business operations and is used by executives and technicians. Essentially, the more skill and knowledge required to use a given piece of software, the higher switching costs.

It is easier to switch basic email software (eg from Gsuite to Outlook) than it is highly technical software. These high switching costs should give rise to pricing power.

I own shares in RPM Global because I think it is a high-quality compounder that is not yet widely recognised as such. However, I admit there is less certainty that it is a high quality compounder compared to IDP Education and REA Group, mentioned above. However, sometimes the best returns come when the market is changing its opinion (positively) about a business, compared to when a very solid (and widely loved) business simply continues to perform well.

In any event, I think RPM Global has certainly got a track record of success based on the 10 year share price movements (shown below alongside REA Group and IDP Education).

For those interested in a recent discussion of RPM Global (ASX: RUL) check out this recent baby giants podcast where my friends Matt Joass and Andrew Page discuss the stock.

I recommended RPM Global (ASX: RUL) to A Rich Life Supporters back in June 2023, and while that recommendation remains exclusively for Supporters, I have recently made our coverage of the H1 FY 2024 RPM Global results free to read for all readers.

Disclosure: the author owns shares in RUL and will not trade RUL shares for 2 days following this article. This article is not intended to form the basis of an investment decision. Any statements that are advice under the law are general advice only. The author has not considered your investment objectives or personal situation. Any advice is authorised by Claude Walker (AR 1297632), Authorised Representative of Equity Story Pty Ltd (ABN 94 127 714 998) (AFSL 343937).

Sign Up To Our Free Newsletter