Analyzing companies is inherently difficult, and forecasting a future is even more challenging. Note that if any of the following special scenarios are present, the task becomes increasingly complex:

- The company has significantly diluted shareholder value through multiple capital raises.

- The company has squandered shareholders’ dollars on ideas that failed to materialize.

- The company undergoes a change in management every four to five years.

- The company has acquired multiple companies.

- The company has changed its financial calendar year, making accurate comparisons challenging.

- The company has changed its reporting currency.

- The company has renamed its internal segments and reorganized various business units within those segments.

- The company is transitioning from non-recurring to recurring revenue streams.

- There are management changes.

All these factors make Catapult (ASX: CAT) a real challenge to value, but I believe these negatives are also creating an opportunity.

Catapult primarily operates in the sports analytics industry, focusing on the collection and analysis of athlete performance data.

The foundational technology of Catapult was developed from a five-year collaboration between the Commonwealth Cooperative Research Centre for Microtechnology and the Australian Institute of Sport. This partnership was aimed at enhancing Australia’s Olympic efforts across more than 20 sports. It resulted in the creation of technology platforms that integrate inertial sensors with GPS to track athletes. In 2006, Catapult’s founders, Shaun Holthouse (currently a Non-Executive Director) and Igor van de Griendt (also a Non-Executive Director), established the company to commercialize these innovations, leading to the development of sophisticated tools for measuring athlete performance.

The following images illustrate Catapult’s journey from its inception to its entry into the ASX. I will discuss the history from 2015 onwards in the following section.

|

Since 2015, Catapult has both organically and through acquisitions developed solutions and now reports operations across three main segments:

- Performance & Health: A SaaS platform that tracks athlete data using wearable devices.

- Tactics & Coaching: A video analysis software that enhances coaching strategies and player performance.

- Media & Other: This segment includes the Athlete Management System (AMS) and strategies to monetize video content to increase fan engagement.

Market Overview

Catapult operates within the sports analytics sector, which is an integral part of the elite sports market. This market is defined by the financial value of sports, the number of elite athletes, and the income of these athletes. As all three of these factors grow, the competition within leagues and among individual athletes intensifies, compelling them to utilize their skills optimally and adopt technology to assist in monitoring, coaching, or managing workloads.

A few noticeable trends include the increasing number and financial growth of sports leagues, which are widely reported in the news. Fortunately, recent years have seen significant advancements in women’s sports, for example, the success of the Women’s Big Bash and the Matildas. These developments not only indicate that the sports market is already on an upward trajectory, but they also suggest that it will accelerate even further with the inclusion of women’s sports.

Moreover, fans are increasingly demanding more engagement, driving broadcasters to provide up-to-date analyses using video replays and comprehensive data. Coaches require real-time data to provide accurate feedback, and high-value athletes are making decisions based on detailed data regarding their injuries and sustainable workloads.

The crucial role of sports analytics in facilitating these needs underscores its significance in the evolving sports market. Even without deep-diving into extensive market research data, the broader picture supports the belief that Catapult is positioned in front of an expanding market.

Management

- Executive Chairman: Dr. Adir Shiffman has been on board since 2013. He has founded and sold several technology startups. Dr. Shiffman also runs a podcast, and listening to it gives the impression that he is a smart individual with strong opinions on everything; and he does not shy away from expressing them. He owns approximately 6 million shares in Catapult, which is about 2.3% of the company.

- Board Members: The founders, Mr. Shaun Holthouse and Mr. Igor van de Griendt, still serve on the board as Non-Executive Directors. Mr. Holthouse was the CEO until 2017, and Mr. van de Griendt served as CTO and COO until 2019. Together, they hold roughly 38 million shares, or 14.5% of Catapult.

- CEO: Mr. Will Lopes, appointed as CEO in November 2019, has been pivotal in the company’s ongoing turnaround. Prior to joining Catapult, he was the Chief Revenue Officer of Amazon’s subsidiary, Audible. After becoming CEO, he has brought on several Amazon executives to assist in steering the turnaround, notably Chris Cooper as COO and Zoe Rumford as CPO

- CFO: Bob Cruickshank, who became the CFO in April 2023 and is based in the USA, has a history of working with Amazon as well. The main reason for the CFO change was the need for a US-based CFO, as opposed to one based in Australia.

- Ownership and Shares: As of now, Catapult has issued a total of 261,107,456 ordinary shares. Key insiders, including board members and top executives, hold about 18% of the company’s total shares, demonstrating a substantial ownership stake. There are also almost 26 million unquoted securities, such as long-term and short-term incentives, and various options, which are poised to potentially dilute existing shares in the future.

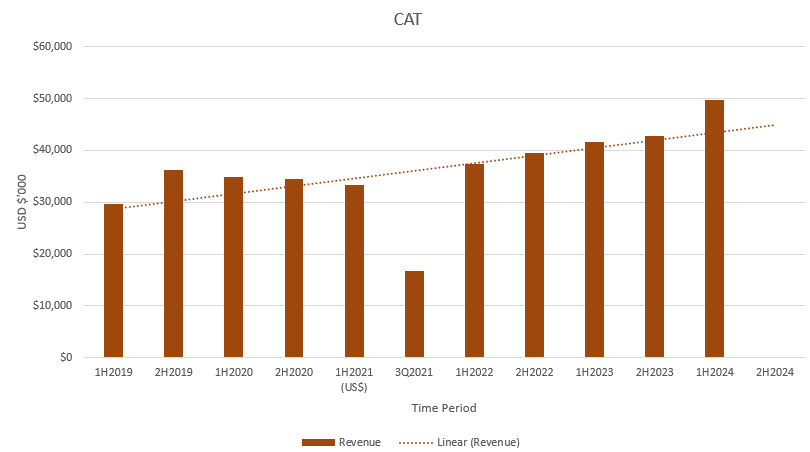

Catapult’s Revenue

In H1 FY 2024, Catapult reported revenue of US$49.8m and a loss of US$8.4m. The graph below shows the revenue trend over time, with figures presented in US dollars.

|

Note: From 1HF 2021, CAT switched its reporting currency from AUD to USD, I have standardized past figures to reflect this change using a conversion rate of 0.69 cents. Catapult also restructured its financial calendar from FY22. Originally, Catapult’s financial year began in July, but from FY2022 onwards, it starts in April. This led to the financial year 2021 being only nine months long, making “2H2021” actually just the third quarter of that year.

Moreover, Catapult transitioned from a capital sales model to a subscription recurring revenue model. This shift is mainly complete, and now the majority of Catapult’s revenue is recurring subscription revenue.

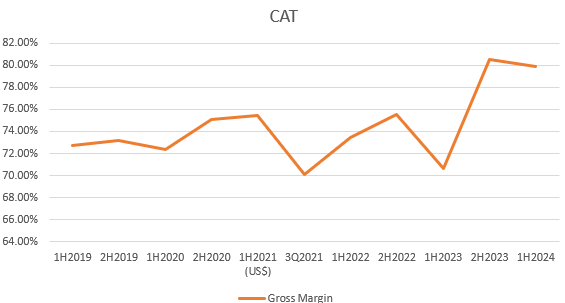

Catapult’s Gross Margin

The graph below shows the gross margin trends. It’s important to note that, as mentioned earlier, the move from capital to subscription sales means that “COGS” costs from wearable hardware sales have been capitalised and then recorded as depreciation. Additionally, Catapult has started capitalizing “hotswap units” — used for servicing/replacement obligations for legacy capital deals — instead of expensing them from FY23. These changes have positively impacted the gross margin.

|

Balance Sheet

Catapult holds a revolving loan facility worth US$20 million, scheduled to mature on December 27, 2024. From this $20 million facility, CAT has drawn US$11 million (As of Sept 2023) and faced an average interest rate of 9.3% in 2023. Additionally, CAT had $US10.3 million in cash as of September 2023, positioning it with adequate liquidity despite its current debt level.

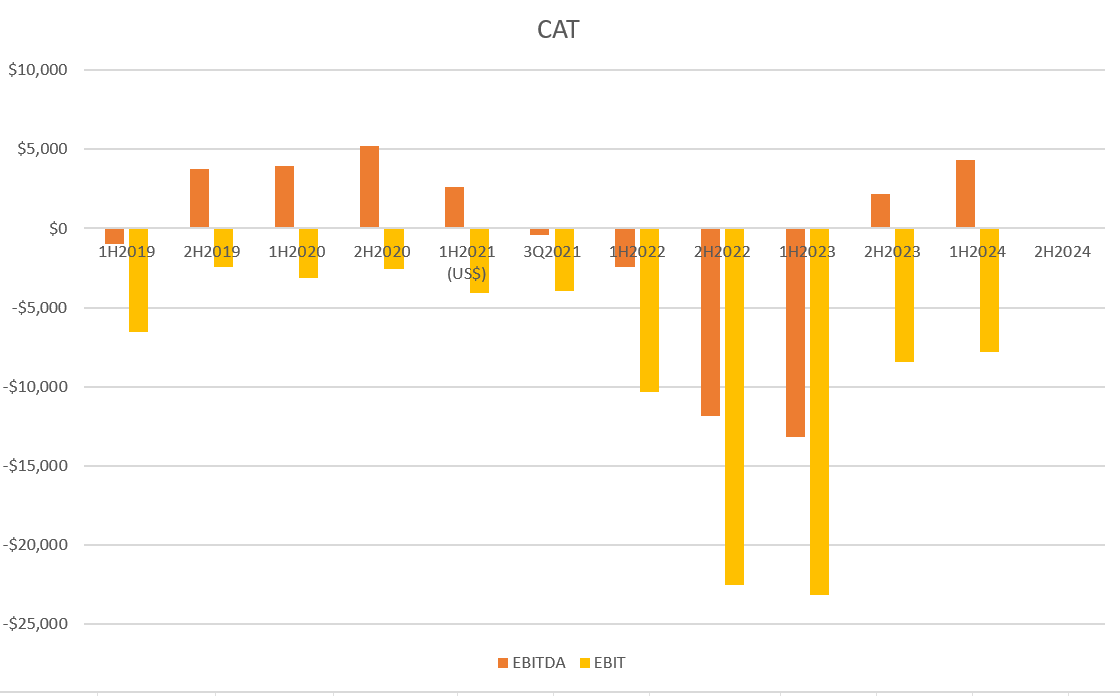

Earnings

Catapult hasn’t achieved profitability yet, so to judge how efficiently it is running its operation, I have put together this EBITDA and EBIT chart. The explanation of the dip during FY22 and FY23 was communicated as due to an accelerated growth investment strategy, as well as added depreciation from capitalising device costs as part of SaaS model.

|

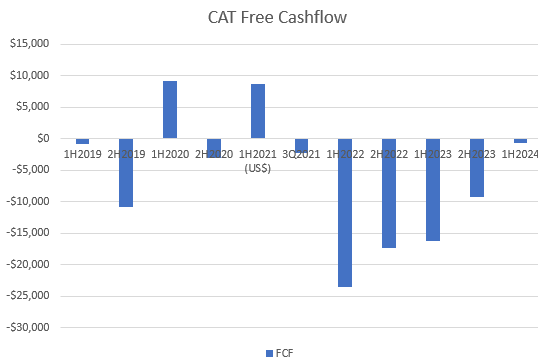

Cashflow

The chart below shows the free cash flow (I have calculated free cashflow as Net increase/decrease in cash and adjust for loan drawdown/repayment and cash received for share issues – but I haven’t factored in the impact of Employee share-based payment expense for this graph). Note that according to the company’s calculation of free cash flow, which excludes interest and lease repayments, it actually made a positive free cash flow of US$1.3m in the last half.

|

Why Catapult Deserves A Spot On Your Watchlist

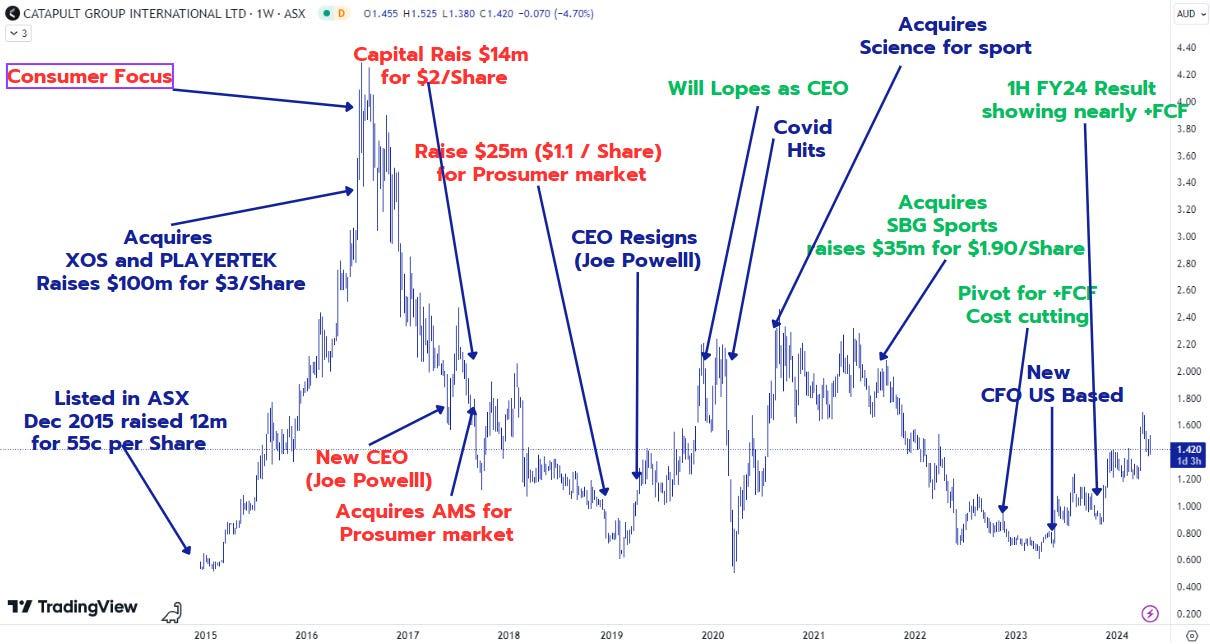

Let’s delve into Catapult’s ASX-listed history so far. The following picture illustrates key events such as capital raisings, acquisitions, and management changes.

|

After listing on the ASX, Catapult had an amazing start, and everyone was excited about its prospects until late 2016. This was when they shifted their focus towards the consumer/prosumer market and began burning through cash. From then on, for a number of years, Catapult was somewhat out of favour in the market, and understandably so. The company was often seen as too aggressive in its investor materials and struggled with clear profitability strategies.

However, from the latest financial results, it’s clear that Catapult is close to achieving positive free cash flow.

Although the company currently balances an equal amount of debt and cash, with continued prudent management, it has the potential to evolve into a profitable, global sports analytics business. This progress suggests a promising future where Catapult could generate significant cash flow and substantially enhance shareholder value.

Based on the results of 1HFY24, the market has recognized the potential, and the share price is now sitting at around $1.50, up from around $0.80.

At $1.50, the market cap of Catapult is approximately $393 million. It is generating roughly $100 million USD revenue per year, growing its top line by 20%, boasts a high gross margin of ~80%, and on the verge of free cash flow positivity. It is set to report its FY24 results on May 30, 2024. This upcoming report is crucial to validate the thesis that current management will deliver free cash flow, as promised.

You can read more of GG’s writing at growthgauge.substack.com.

Disclosure: The author of this article owns shares in CAT. The editor Claude Walker does not own shares in CAT. Neither will trade shares in any of the company mentioned for at least 2 days following the publication of this article. This article is not intended to form the basis of an investment decision and is not a recommendation. Any statements that are advice under the law are general advice only. The author has not considered your investment objectives or personal situation. Any advice is authorised by Claude Walker (AR 1297632), Authorised Representative of Equity Story Pty Ltd (ABN 94 127 714 998) (AFSL 343937).

Sign Up To Our Free Newsletter