Scientific measurement device manufacturer Trajan Group Holdings Ltd (ASX:TRJ) is named for the Roman general Trajan, who led the empire to its greatest territorial gains as well as building extensive infrastructure. Trajan’s founder and CEO Steven Tomisich appears to be building his own empire with a slew of acquisitions since listing. But is the CEO moving too fast, and will Trajan assimilate these acquisitions successfully?

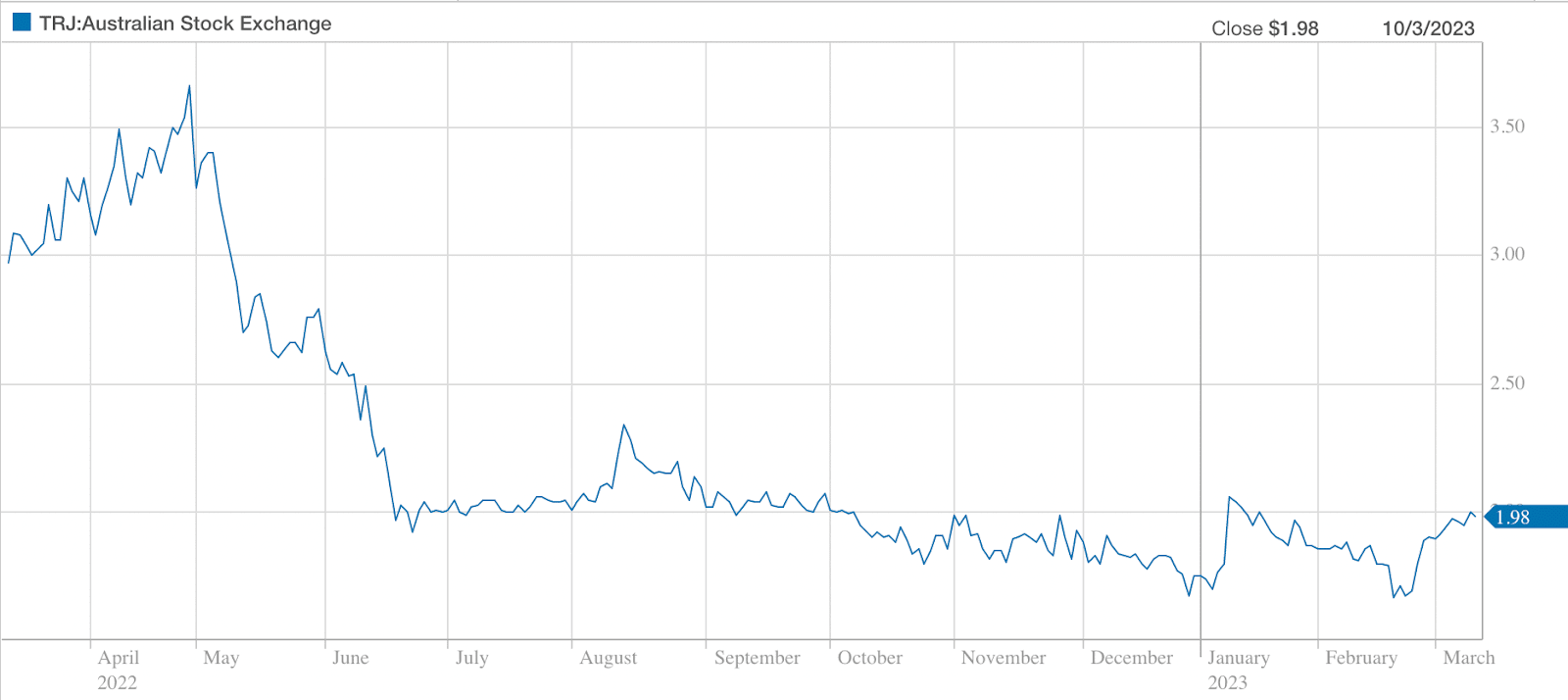

Trajan Group listed in June 2021 at $1.70 and got off to a flying start, hitting $4.41 in early 2022, before pulling back to currently sit around $1.95. I (Chris Coe) purchased a small parcel of shares in November 2021.

The rise in interest rates has seen a downturn in the share price of many growth companies. Investors may also be wary of Trajan’s rising debt to equity ratio, and the possibility of future dilution of shares if the company makes more acquisitions.

Trajan has a market capitalisation of just $301 million market capitalisation, so it may be flying under the radar of many investors. In this article, I argue Trajan could deserve a spot on your watchlist, given its potential for incremental revenue and margin growth, in the years to come.

What does Trajan Group Holdings (ASX:TRJ) do?

Trajan Group Holdings (ASX:TRJ) develops and manufactures scientific measurement devices.

Trajan provides devices that span the scientific measurement process. Examples include syringes, microscope slides, test tubes, home blood sample pens, to more complex devices such as machines to dispense liquids and separate elements in a given sample.

Trajan’s revenue is derived from developing and manufacturing scientific measurement products, parts and systems that are supplied to laboratory based customers for the purpose of identifying and quantifying specific components of a sample, generally in the food, environmental, biological and pharmaceutical sectors.

Trajan is based in Melbourne and has seven manufacturing sites across the US, Australia, Europe and Malaysia, and operations in Australia, the US, Asia, and Europe. Trajan earns more than 95% of its revenue outside Australia, mainly from North America.

A brief history of Trajan Group

Trajan was founded by Steven and Angela Tomisich, a couple with extensive experience in analytical chemistry and biomedical science, with the acquisition of two pathology consumables businesses in 2011 and 2013.

Also in 2013, Trajan made the significant acquisition of SGE Analytical Science, a chromatography and liquid handling business, operating in the highly specialised analytical syringe sector. This gave Trajan a host of new core capabilities and gave the company a global footprint through SGE Analytical Science’s customer base and distribution hubs.

Trajan made seven acquisitions between 2011 and listing on the Australian Stock Exchange in June 2021. It has since acquired five more businesses..

Trajan Group Holdings Financial Results For H1 FY 2023

Trajan Group results for the first half of the financial year 2023 show continued growth. Revenue was up 83.2% on the prior corresponding period to $80.1 million. Net Profit After Tax (NPAT) was $3.18 million, up from $153,000 in H1 FY 2022. Free cash flow was $8.1 million up from $1 million in the prior corresponding period. Increased sales due to acquisitions and organic growth were partially offset by increased raw materials prices, supply chain costs, and financing expenses. To account for higher input expenses, Trajan increased its product prices during the period.

The below chart shows revenue (millions) and gross profit margin growth (%) by financial year, including guidance for the next half..

Source: Trajan group Half 1 financial year 2023 report

Net assets increased $11 million to $126.8 million with cash on hand increasing to $21.1 million from $13.1 million at 30 June 2022. In H1 FY 2023, Trajan Group reduced net debt by 27.8% to $30.1 million.

While Trajan is making acquisitions, it has also produced organic revenue growth. Of the $80.1 million half year 2023 total revenue, $31 million was from the recent acquisitions, but $7.6M was organic growth. Excluding acquisitions, revenue would have increased by 18.6% on the prior corresponding period ($40.8M v $48.4M).

Trajan historically grew its profit quite steadily, until FY 2021, when Trajan incurred IPO related expenses. Then, in FY 2022, Trajan incurred significant acquisition and restructuring costs.

Trajan earned just 2.1 cents per share in H1 FY 2023, and its share price is almost $2. Even if it improves earnings substantially in the next half, Trajan trades on a fairly high multiple of earnings, compared to the market average. Therefore, Trajan must grow profits significantly, in the future, in order to justify its current share price. The chart below shows how revenue growth has accelerated over recent periods. Next, Trajan must show it can also improve net profit margins.

Trajan Group FY23 Guidance

Trajan has upgraded revenue guidance for the 2023 financial year to between $155 – $165 million and Normalised EBITDA has been upgraded to between $21.7 million – $25.8 million.

Trajan Group’s acquisitions since listing

Trajan has made five acquisitions since listing. Four in the 2022 financial year, and a smaller one recently.

Trajan announced in February 2023 it has entered into an agreement to acquire the HDExaminer software from Sierra Analytics Inc. for $US430,000. The software enables analysis of the structural information of protein generated by the Mass Spectrometer (device used to find the characterization and sequencing of proteins in a sample).

The largest acquisition was US company Chromatography Research Supplies, a manufacturer of analytical consumables in June 2022 for $63.8 million. This was funded through a share purchase plan, debt financing of $20 million, and $13.4 million from existing cash.

In December 2021 Trajan acquired US Analytical science and device company LEAP PAL Parts for $10.6 million, funded through existing cash and debt.

Blood microsampling products developer Neoteryx was also acquired in December 2021 for $29.5 million. Neoteryx was issued 4,659,843 shares in Trajan and received a cash payment of $US5.05 million, funded through debt. Trajan believes there will be expanding adoption of microsampling, where people take samples of their blood with small devices. The Neoteryx acquisition adds to its own portfolio of microsampling products.

Interesting sidenote: A revolutionary microsampling device was the story high profile fraudster Elizabeth Holmes of Theranos touted to investors.

In November 2021, Trajan acquired Axel Semrau GmbH, which develops and manufactures laboratory automation and chromatography software and detection systems. Cash consideration of $31.5 was funded through a mix of cash and debt.

Also in November 2021, Trajan purchased 9.6% of shares in Humankind Ventures for $1.3 million. Humankind Ventures provides at-home testing services for people to track and optimise their health.

Trajan has a solid history of acquisitions and these four are complementary to the business. As companies are acquired, fixed costs as a percentage of sales should decrease and profit should increase.

Trajan Group Is A Founder-led Company

Founder-led companies are always worth having a look at, as having skin in the game aligns founders’ interests with shareholders’ interests, especially if a large part of their wealth is invested in the company. The Tomisich Family currently own ~50% of outstanding shares in Trajan.

The founder purchased $17,115 worth of shares on-market at $1.72 in December and made an off-market buy of $632,499 worth of shares in November. He also purchased 15,000 shares as part of the recent share purchase plan.

Trajan Group Industry Dynamics

Trajan operates in the global analytical science industry. Analytical science involves the determination and measurement of the composition of substances, which could be solids, fluids or gases.

Customers use Trajan’s products and services when testing for food and beverage contamination, safety and process quality control, testing for environmental contaminants, and a broad range of biological and healthcare applications – these include pharmaceutical drug development and manufacturing, vaccine development and clinical research and diagnostics, pathology, and toxicology. Customers include NSW Health, large companies such as Pfizer and GlaxoSmithKline and environmental testing laboratories such as ASX listed ALS Ltd (ASX: ALQ), which I own shares in.

This is a relatively defensive industry as testing for contaminants is usually considered a necessary and non-discretionary item, and the equipment is usually a small percentage of total costs of the entire process. Typically the lifetime of an analytical instrument, such as the mass spectrometer or chromatograph is ten years. Over that time the customer may spend as much on consumables as they did for the purchase of the original instrument. An example of consumables for these instruments would be vials or syringes, or other components that come into contact with the sample.

The below chart shows what industries Trajan’s products are used in and the compound annual growth rate of each industry.

Source: Trajan Group Prospectus

There are some industry tailwinds for Trajan, such as an increased awareness and focus on environmental issues, and food and beverage testing and assurance.

A rising middle class, especially in emerging economies, will see an increased demand for higher quality and safer food products particularly for meat, such as beef, poultry and seafood products.

People are more aware of the globalisation of the food chain and want to know where and how their food is made. There is also an increasing concern around the impact of environmental contaminants such as plastic particles, and the potential impacts on the body.

Trajan’s competitors are large scientific device manufacturing companies, and also smaller start-ups looking to service a niche area. Trajan has a wide range of products for different markets and operates globally, so it is unlikely one single competitor would disrupt Trajan’s business.

There are high barriers to enter the scientific measurement device manufacturing industry and potential start-ups need expertise in scientific measurement. This is a highly specialised area that requires extreme precision in its testing products. Spending on research and development is also required to keep up with changing science and technology, and regulatory requirements and international standards for products need to be adhered to.

Some Risks to Trajan Group Holdings (ASX:TRJ)

An inherent risk in making acquisitions is that the businesses will not integrate well, or not add the value expected. Trajan’s CEO will need to remain disciplined and not overextend by buying large companies that do not work out, or branching into different fields where Trajan does not have expertise or which don’t complement the core business.

Having only been listed for a year and a half, there is not much public history to go on. As an owner of shares, I would hope the CEO’s experience of integrating companies prior to listing will pay dividends when it comes to the integration of Trajan’s latest acquisitions.

The company has already increased debt levels and conducted a share purchase plan and institutional placement to fund acquisitions. Future acquisitions would require the company to take on more debt and/or issue more shares, thereby increasing the debt-to-equity percentage and diluting existing shareholders.

In FY22 the largest customer accounted for 19.4% of revenue, which presents a big risk to profit if that customer decides to discontinue using Trajan’s products. No other customer accounts for more than 10% of revenue.

Trajan has been dealing with a number of pressures recently, including increased materials and freight costs, delayed supply chains, the Russia/Ukraine conflict, and absenteeism due to COVID-19. Trajan has been able to pass some of the cost increases on to customers and testing equipment is often a small percentage of customers overall costs.

My View On Trajan

I (Chris Coe) chose to buy a small parcel of shares as part of a diversified portfolio of growth companies. Trajan has a history of making acquisitions and integrating them successfully, and I am hoping the CEO continues on this path.

Technical analysis is not something I indulge in too deeply, but I am never in a hurry to buy when the share price is steadily trending down, as it is at present.

I think this is one to watch and see if the recent acquisitions can achieve incremental revenue and margin growth. In theory, as the company gains scale, its margins should improve. However, this is not guaranteed.

Disclosure: the author of this article owns shares in TRJ and will not trade them for at least 2 days following the publication of this article. The editor does not own shares in TRJ and will not trade them for at least 2 days following the publication of this article. This article is not intended to form the basis of an investment decision and is not a recommendation. Any statements that are advice under the law are general advice only. The author has not considered your investment objectives or personal situation. Any advice is authorised by Claude Walker (AR 1297632), Authorised Representative of Equity Story Pty Ltd (ABN 94 127 714 998) (AFSL 343937).

Sign Up To Our Free Newsletter