One of the standout sectors in the H1 FY 2023 results reporting season was transport stocks. Despite this, unlisted competitor Scott’s Refrigerated Logistics recently went into administration in February. This sets the scene for the surviving freight companies to take over some of those contracts.

CTI Logistics (ASX: CLX) reported net profit after tax for H1 FY 2023 half year was $10.6m, up 81% on the prior corresponding period. Meanwhile, Lindsay Australia Limited (ASX: LAU) reported NPAT up 37% to $16.8 million.

In both cases, these strong results were supported by record half year revenue, as supply chain constraints saw many customers build inventories held in these distributors’ warehouses.

However, we have yet to see any benefit to these companies from the demise of Scott’s Refrigerated logistics, so it is quite possible that results will remain strong in H2 FY 2023, despite the fact supply chain constraints may well see a reduction in customer inventory.

So let’s take a look at each of these two stocks.

CTI Logistics (ASX: CLX) Stock Analysis

We have covered this WA-based shipping, storage and contract logistics company already, arguing that it has a strong asset base to support (much of) its current market capitalisation. On top of that, its half year results showed whopping profit growth of 80%, due to an unusually benign industry dynamic.

First, the supply chain squeeze we saw over 2022 meant that the amount of product caught up in supply chains (and inventory) increased. This was positive for a company like CTI Logistics, that stores inventory, and delivers it. While CTI Logistics did suffer some inflationary pressures, it was able to more than offset this as increased demand saw more volume across a largely fixed asset base.

On top of that competitor Scott’s Refrigerated Transport went into administration in February. This may create opportunities for CTI Logistics to win extra contracts. Certainly, it is favourable timing for CTI, since the it’s development of a transport hub at Hazelmere is expected to complete in May 2023. Any additional contracts would help fill that capacity.

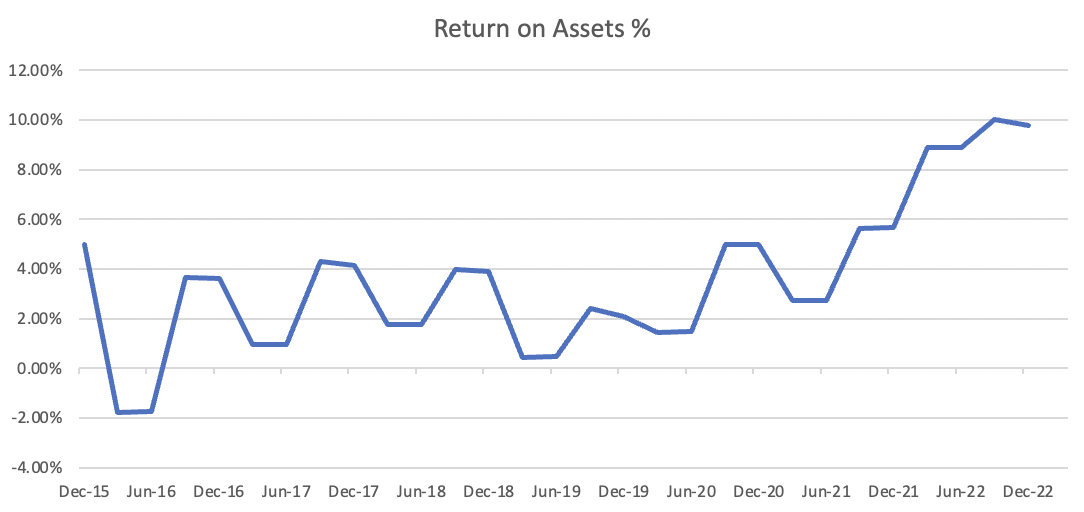

Overall, though, the big risk for CTI Logistics shareholders is that the company is currently earning unsustainable returns on its assets. The chart below takes semi-annual data on CTI Logistics’ return on assets and smooths them over each quarter to estimate a quarterly return on assets.

Any way you look at it, CTI has earned exceptional returns on assets over the last year, and my guess is that this measure will return to the mean, over time.

To me, that means profit is almost certain to drop from current levels, eventually. Indeed, the company itself says:

“In the context of inflation and increasing interest rates, along with continuing wage cost pressures, forecasting the operating environment and outlook remains difficult and we remain aware that future trading volumes and activity could be impacted as a result.”

However, even if earnings per share drops by 50% in the second half of FY 2023 (compared to the first half), then the company would earn over 21 cents per share in FY 2023, putting it on a P/E ratio of just 7.6 for FY 2023. If profit then remains at that level, the company would be trading on about 11.5 times earnings in FY 2024.

Right now, the trailing dividend yield is about 5.6%, fully franked (being about 8% grossed up).

Finally, the debt of $20.4 million looks very manageable, especially given free cash flow of over $10.5m in the last half alone.

Executive Chairman and founder David Watson owns around 30% of the business, and it does seem that he has shared the recent success of CTI Logistics with all shareholders via increased dividends.

While I have no plans to buy shares myself, I think CTI Logistics is probably an undervalued business that can continue to pay a solid dividend in the current environment. However, I would not consider taking a large position, because we don’t know how long the current operating environment will last.

If return on assets falls considerably, we could well see profits halve from here (or worse). My guess is that that scenario would probably provide a more attractive entry point than the current price.

That said, given the decent dividend, record revenue, and record profits, I see no reason why CTI Logistics’ strong run cannot continue a little while longer. Finally, it is important to remember that CTI is extremely illiquid. Therefore, it would only be appropriate for investors to invest a small amount.

Lindsay Australia (ASX: LAU) Stock Analysis

In the half year ended 31 December 2022, Lindsay Australia (ASX: LAU) grew group revenues 23.2% to $337.4m and underlying EBITDA to $42.8 million, up 36.2% on the prior corresponding period. Net profit was up about 36% to $16.8m. The interim dividend was 1.9 cents per share, which is well covered by earnings per share of 5.6c, and brings the trailing twelve month dividend yield to about 3.8% at the current price of 96.5 cents per share.

Lindsay’s hybrid logistics model (road/rail) and diverse geographic footprint have proven to be the wind beneath its wings. Its larger transport division contributed $48.3 million in underlying EBITDA, up 38.8%, while the smaller rural division contributed just $5.15m in underlying EBIDTA, a flat result.

Within the transport division, both the road and rail businesses saw organic growth, even despite unfavourable weather conditions, labour shortages (especially across the division’s driver pool) and growing cost pressures.

The company intends to continue investing in growth, with $34.3m of capital investment expected in the second half, including investment in road transport equipment and facilities.

Finally, Lindsay Australia faces a significant change on the horizon: founder and managing director Kim Lindsay is set to retire in June 2023. While his departure, after 20 years at the helm, is hardly positive, the support of substantial holder Washington H Soul Pattinson (ASX: SOL) may provide some solace to investors.

Ultimately, Lindsay Australia may well be in a good position to continue its earnings growth, at least in the short term. As a large national distribution network, it is very well placed to pick up contracts made available by the demise of Scott’s Refrigerated Logistics. And indeed its expansion plans no doubt support that strategy.

As at December 2022, the company had cash of about $36 million and debt just under $28m. Its largest liabilities are lease liabilities for both equipment and property. So it’s fair to say operating leverage could really bite, if the company found demand falling.

The company is currently expecting “Underlying EBITDA of between $68 million and $71 million in FY23.” This implies at least $25m underlying EBITDA in the second half. Even if earnings per share fell by 50% (from 5.6c to 2.8c) half on half, then Lindsay would be trading on about 11.5 times earnings.

In the last 10 years, Lindsay has always had a stronger first half result, so I would not be concerned by the weaker second half. Longer term, it is clear that the last three halves have shown very strong earnings. However, it is less clear if this is a sustainable benefit of scale, or a more temporary measure.

In the short term, with the company reinvesting to take market share, Lindsay Australia could easily see earnings surpass the relatively low expectations implied by the share price. Given the demise of Scott’s I like their chances of reasonably resilient results. That said, the nature of this business is that it is very sensitive to demand.

So while I think that the short term business (and share price) momentum looks quite good, I would think of it as a trade more so than a long term investment. If and when Australia enters a recession, I think it’s quite likely Lindsay would suffer a sharp reduction in profits.

Conclusion

If I owned Lindsay Australia or CTI Logistics shares, my concern would be that the businesses are currently over-earning, relative to their historic profitability. In the short term, the over-earning may continue, so if I held shares, I’d probably keep holding them for now. However, I would keep an eye out for deteriorating results, or signs of a recession in Australia.

Both companies have already benefitted from strong share price gains resulting from the recent strong profit growth, so I can’t help thinking I’m a bit late to the party, on these stocks.

Since December 2013, CTI Logistics has averages a tad over 5c per year in dividends (though these dividends have been fluctuating, and are unevenly spread out over the period). At the current price of $1.60, that’s a yield of 3.125%, grossed up to 4.46%. Not exactly inspiring.

Ultimately, my conclusion is that either of these businesses could be a good investment, at the right price, but I’m too afraid to buy them off the back of such (unusually) strong results. However, I could see the rationale for a shorter term trade, given the good business (and share price) momentum.

Sign Up To Our Free Newsletter

Disclosure: the author of this article does not own shares in CLX or LAU, and will not trade shares in DTL for at least 2 days following the publication of this article. This article is not intended to form the basis of an investment decision and is not a recommendation. Any statements that are advice under the law are general advice only. The author has not considered your investment objectives or personal situation. Any advice is authorised by Claude Walker (AR 1297632), Authorised Representative of Equity Story Pty Ltd (ABN 94 127 714 998) (AFSL 343937).