Audinate Group Ltd (ASX:AD8) is a global market leader in providing AV technologies via its Dante platform, distributing digital audio and visual signals over computer networks. You can read fairly extensive past coverage of Audinate stock via this link.

Audinate is expected to release its full year FY23 results on 21 August 2023 and since the 1H23 results the company has been very quiet on the announcement front. The 1st half results showed revenue in US dollars up 39% to USD $20.6 million with a net loss of AU $381,000 compared to the AU $2.1 million loss in the prior period.

However, Audinate increased their capitalised software to just over $7.4 million up from $4.7 million leading to a free cash outflow of $6.8 million, an increase of around 39% on the pcp. The overall spend on R&D remained consistent as a percentage of revenue compared to prior periods.

Gross margin declined to 71.2% from the historical average of around 75% due to a number of factors with the main contributors being the product mix of lower margin Viper board products as part of the Silex Video business (at margins below 50%), and the transition from Brooklyn 2 to Brooklyn 3. Margins are expected to move back to the historical 75% mark, over time.

Management maintained their outlook for the second half of the year with the path to growing revenue driven by increasing headcount. It was noted that the record levels of demand and backlog of sales support historical revenue growth. That would suggest an increase in the realm of 25-30%. Revenue in FY 2022 was USD $33.4 million, so that implies at least USD $41.75 million in revenue. That seems fairly achievable given the first half revenue was USD $20.6m.

While global macro uncertainty and lingering chip shortages have presented difficulties over the past couple of years, these headwinds seem to be easing.

Key Factors to Watch

Competition

Audniate is the superior player in audio products and within each presentation boasts of its clear market dominance.

It has in recent times conceded some ground to competitors. Ravena in particular has started to expand its total audio products per protocol. That said, Audinate is absolutely dominant with 12x the market adoption of its closest competitor, per the 1H23 presentation. However, this measure of dominance was down from 14x at 30 June 2022 and 19x at the end of 2021.

This entrenched market position not only provides a stable revenue stream but also creates barriers to entry for potential competitors. But whether this can be maintained as competition increases, is still something to monitor.

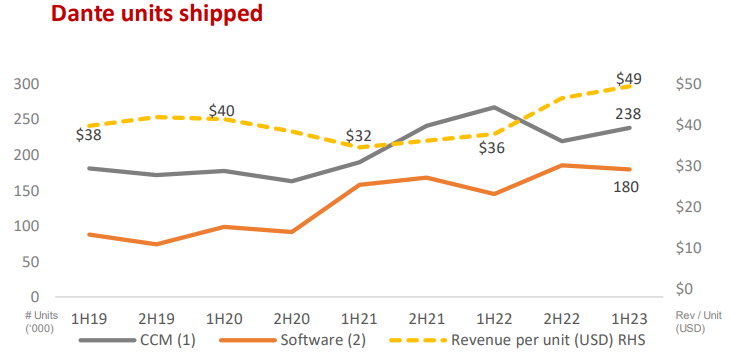

Units Shipped, Revenue per Unit & Design Wins

The number of chips, cards and modules (CCM) units shipped dipped in the first half as the Ultimo units suffered from supply constraints and the Broadway chip was discontinued with the Brooklyn 3 module taking its place. The performance of the Brooklyn 3 will be a key item to look for as it may increase revenue per unit. Brooklyn 3 and Viper Board sales, while both lower margins, have contributed towards the increased revenue per unit.

As part of the H123 call CEO Aidan Williams highlighted slide 27 as a sales pipeline and emphasised the importance of design wins as the leading indicator of future repeating revenue. Design wins went from 95 in FY21 to 126 in FY22, with a further 78 design wins in H123, we should see this translate to revenue growth.

Dante Video

Audinate has stated a FY23 goal of 10,000 video products shipped and US $3 million in revenue. In the first half the company reported shipping 6,000 video units and recording $2 million in revenue. But it will be important to check how the company achieves against this goal, for the full year.

I touched on revenue growth and margin earlier and while both are equally important I think the growth in per share metrics are a crucial way to assess Audinate’s performance.

Diluted earnings per share has been negative for some time, particularly post pandemic as chip shortages and supply chain issues wreaked havoc. The first half of 2023 produced a negative earnings per share of 0.49 cents down from a 2.80 cent loss in the prior period. That’s an improvement, but it’s worth noting the importance of capitalised software expenditure.

This boosts statutory earnings as the expenditure is capitalised on the balance sheet, and only recognised as an expense in the profit & loss statement, gradually over time, through amortisation charges. Competition in the audio networking market is increasing, and Auditnate needs to continuously innovate and stay ahead of its rivals so it is reasonable to assume this cost will continue to increase.

Perhaps a better way to assess the result would be a free cash flow per share calculation which takes into account the capitalised software.

While receipts from customers are growing with revenue, the conversion to free cash flow is yet to materialise given the considerable capitalisation of research and development, plus the need to build inventory. So we can expect continued cash burn in FY 2023.

Audinate had a little under $38 million in cash and term deposits at 31 December 2022. Therefore, even if the company continues to burn cash at a similar rate to the first half (just over $6m per half, around $12m per year), it could still survive two or three years without needing to raise cash.

Notably, in FY 2022 management did have short term incentives triggered by financial and non financial performance including increases in USD Revenue, AUD EBITDA plus audio and video wins. Existence of performance metrics like these can create perverse incentives when it comes to decisions around capitalisation of software development, because the less you capitalise, the higher the EBITDA performance will be. Some investors prefer companies that have lower capitalised development (more conservative accounting).

Valuation

Audinate currently trades at a market capitalisation of around $682m. After adjusting for cash, that gives us an enterprise value of around $644 million. Trailing twelve month revenue is about $56.9 million, so Audinate currently trades on an enterprise value to trailing twelve revenue multiple of about 11.3 at the current share price of $8.81.

As with other unprofitable growth stocks, Audinate’s multiple has come down since the heady days of late 2021, but still implies plenty of ongoing growth.

Audinate Group Ltd demonstrated strong revenue growth of 52% (in AUD terms) for the first half of the year. While it’s not great to see lower gross margins and increased capitalised software development, the longer term thesis that Audinate has pricing power due to building a quasi monopolistic level of dominance remains plausible. As long as Dante (Audinate’s protocol) remains the dominant standard, economic incentives will ensure equipment manufacturers are virtually compelled to include their chips.

Disclosure: The author of this article Nick Maxwell owns shares in Audinate. The editor Claude Walker does not own shares in Audinate. Neither will trade Audinate shares for at least 2 days following the publication of this article. This article is not intended to form the basis of an investment decision and is not a recommendation. Any statements that are advice under the law are general advice only. The author has not considered your investment objectives or personal situation. Any advice is authorised by Claude Walker (AR 1297632), Authorised Representative of Equity Story Pty Ltd (ABN 94 127 714 998) (AFSL 343937).

Sign Up To Our Free Newsletter