Yesterday, Beacon Lighting (ASX: BLX) reported their FY2023 results with record revenue of $312 million (albeit only modest growth of 2.5%) and a decline in profit of 17% to 33.6 million highlighting the current cost of living impact on retail consumers.

Beacon Lighting operating cash flow dropped to $48.9 million down over 6% on the prior year as a result of working capital movements, in particular increasing inventory spend, higher trade receivables and a reduction in trade payables. In addition to those working capital movements an increase in operating expenditure contributed to Beacon’s cash balance dropping from $28 million in 2022 to $20 million for FY 2023.

Beacon Lighting gross margin declined to 67.7% as a result of a continuing change in product mix. The dividend for the full year declined by 10.75% to $0.083 per share with the expectation that the future dividend payout ratio will be between 50% to 60% of the net profit after tax.

Beacon Lighting Focusing On Trade Customers

Beacon has made no secret that it is looking to strengthen its relationships with trade customers in FY2023 by re-launching Beacon Trade on an advanced loyalty tech platform. The move aims to enhance customer experience and provides rewards for trade clients, offering perks like Beacon Cash and exclusive prices.

As a result the Beacon Trade brand saw an increase of 21.6% in total trade sales and a 36.0% surge in online trade sales, along with significant member growth. This strong growth is impressive given the headwinds currently facing the building industry with the collapse of multiple well known volume builders and the continued declining trend in dwelling approvals.

The higher proportion of trade clients impacts the gross margin mix compared to traditional retail customers. Trade clients tend to be at a lower margin and require higher inventory levels due to the higher quantity in demand for products. Think setting up an entire new build with lights vs the retail customer entering to pick up a lamp.

Trade sales made up 29% of total revenue which equates to just over $90 million and masks the slowing of Beacon’s retail revenue.

Beacon’s Weaker Retail Sales Reflect Economic Conditions

It was a real tale of two halves for Beacon with the first 6 months of 2023 seeing sales grow by 8.8% buoyed by strong trade sales.

Rising interest rates, inflation, and economic uncertainty impacted the retail consumer in the second half creating a much more challenging market for the company.

While rates did begin to rise at the tail end of the 2022 financial year, the second half of 2023 was when customers of Beacon Lighting clearly felt the pinch, and that was reflected in the weaker retail sales.

Customers choose Beacon because of their expertise and specialisation as well as their quality and aesthetic product.

This leads to higher pricing and if you’re renovating and on a budget, as costs begin to tighten with every RBA increase I would suspect that customers would either begin to delay renovations or look for cheaper alternatives. I’m not a lighting expert by any means but if your budget is tight and you had to choose between a $99.95 Wall Light from Beacon or a $59.98 option from Bunnings or Temple & Webster, it’s clear tougher times would push some consumers away from Beacon..

Beacon Lighting (ASX: BLX) Store Numbers

The blame for this sluggishness was placed on delayed construction in property projects across Australia. Historically, Beacon has aimed to have between 4-6 new stores opened each year and with the delay in 2023 they are now looking to ramp up their output of stores for FY24 with the target to open 8 stores during the year. Chairman Ian Robinson confidently claimed that the target was achievable and that all stores would be open with more than 50% of those in the first half of FY24.

Beacon’s store growth for the year was flat at 117 company stores and two franchise stores. Two stores were opened while another two closed during the financial year.

New stores can take time to get sales up and running and while management noted this has improved in recent years, new storscan still have an initial negative impact on gross margins. Ultimately, Beacon sees the potential for a 195 store network, so there is room for continued growth in coming years, according to management

Beacon Lighting (ASX: BLX) Inventory

Product mix aside, inventory continues to rise. This is far from optimal in a higher rate environment.

At just under $100 million inventory remains 41% higher than 2019 pre covid levels. Granted, some supply chain issues so it might be necessary. However, this iss still an area to watch, particularly with weakening consumer sentiment and a soft retail market.

Indeed, the company increased its provision for stock obsolescence by more than 50% and write-downs were $823k up from $17k in the prior year. While these numbers are minor when compared to the overall inventory figure, the numbers are moving in the wrong direction.

Beacon Lighting Outlook and Valuation

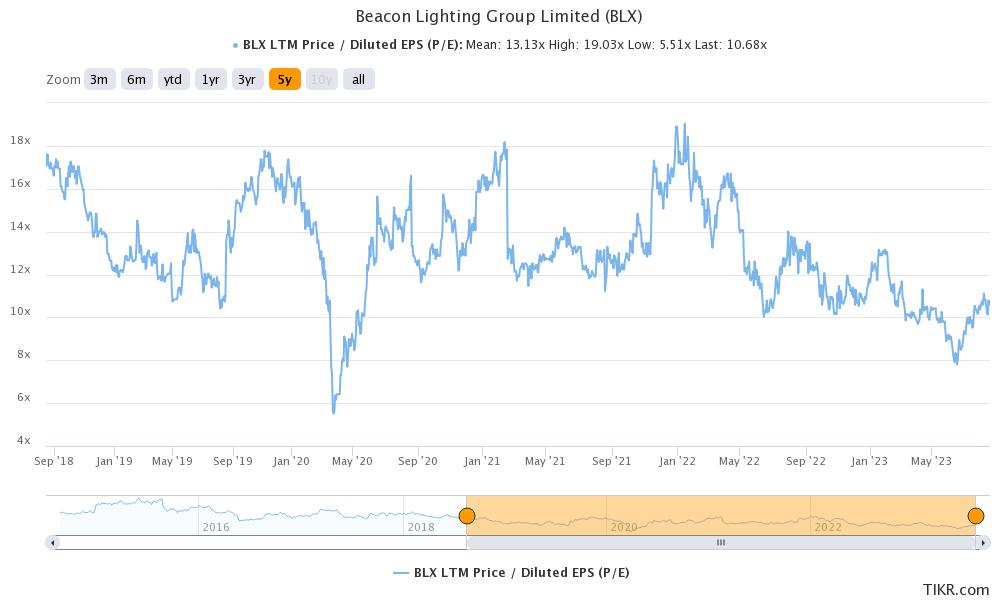

Following the decline in earnings per share to 15.05 cents and a closing share price of $1.80 Beacon trades on a price to earnings ratio of just under 12 and boasts a dividend yield of 4.6%. The 5 year P/E average for Beacon is around 13 which may suggest that any further decline in retail or trade customers may yet to be factored in, particularly if new builds continue to struggle.

While Beacon Lighting faces headwinds from inflation and economic uncertainties affecting retail consumers, the company remains optimistic about its order book and the potential for further store expansion in FY24. The company’s valuation and outlook suggest cautious optimism, with a focus on maintaining relationships and exploring growth opportunities.

While Beacon trades at an undemanding multiple, we can’t find any compelling reason to own the stock.

Sign Up To Our Free Newsletter

Disclosure: The author of this article Nick Maxwell down not own shares in BLX. The editor Claude Walker does not own shares in BLX. Neither will trade BLX shares for at least 2 days following the publication of this article. This article is not intended to form the basis of an investment decision and is not a recommendation. Any statements that are advice under the law are general advice only. The author has not considered your investment objectives or personal situation. Any advice is authorised by Claude Walker (AR 1297632), Authorised Representative of Equity Story Pty Ltd (ABN 94 127 714 998) (AFSL 343937).