Carsales.com Ltd (ASX:CAR) reported its results for FY23 yesterday. The market serenaded the release with the Carsales share price finishing up 7% to $26.33 as at yesterday’s market close, reflecting the positive nature of the the FY 2023 Carsales results.

Revenue increased 53% to $781 million and proforma revenue (which assumes a full contribution from acquisitions made during the period) rose 18% to $798 million. The latter demonstrates strong organic growth for the Carsales business.

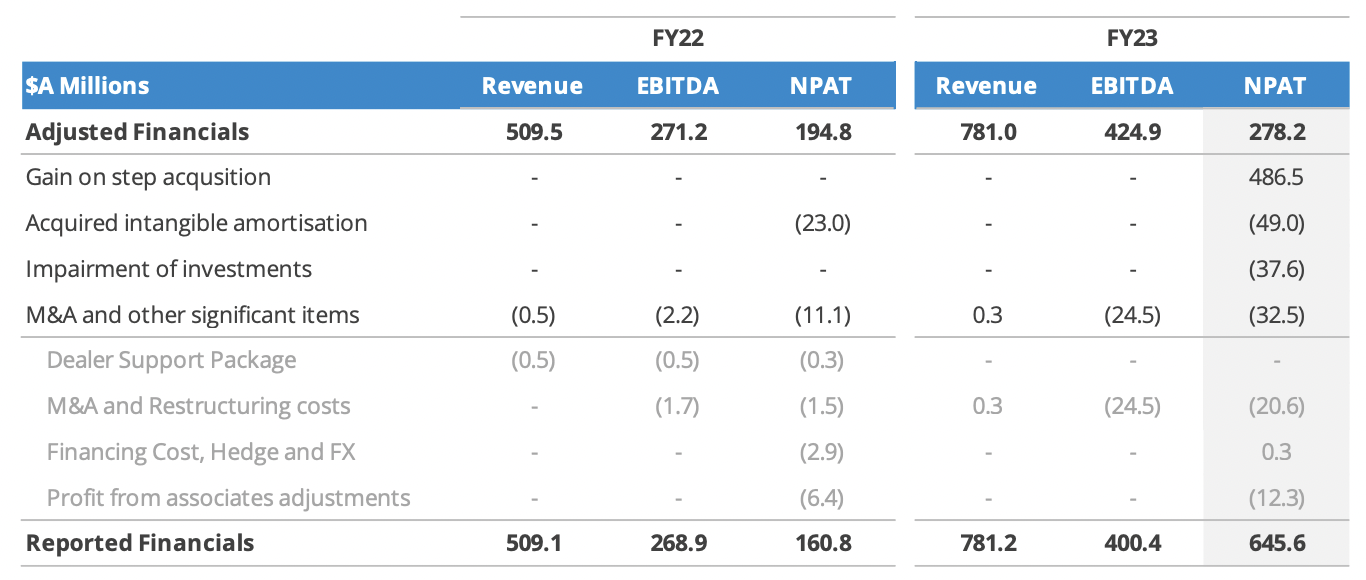

Carsales EBITDA improved 49% to $400.4 million while Carsales proforma EBITDA was up 19% to $495.7 million. Carsales Adjusted EBITDA increased 57% to $424.9 million.

The Carsales net profit after tax (NPAT) increased 301% improvement to $645.6 million on a statutory basis and rose 43% to $278.2 million using adjusted NPAT figures. There is a large gap between these two figures and I will explore the reasons for this later on.

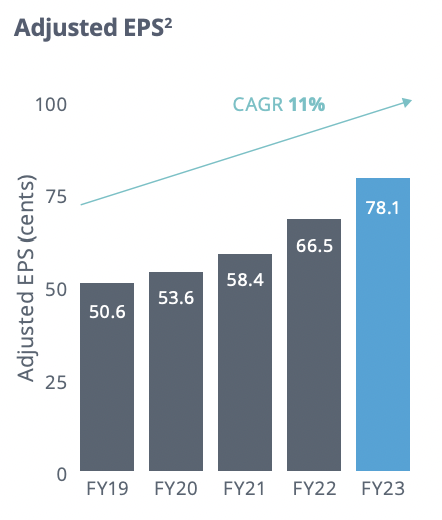

Carsales Adjusted EPS improved 17% to 78.1 cents and based on this figure Carsales shares trade on a punchy PE multiple of 33.7. Earnings per share is the most appropriate metric to gauge overall group performance given management issued 93.1 million new shares for acquisitions during the year increasing total outstanding shares by a third.

Turning to the Carsales balance sheet; net debt increased 88% to $973 million partly due to the use of debt funding for the Trader Interactive acquisition. This is a large increase but still represents less than two times proforma EBITDA so it is a comfortable amount of debt for such a dominant, high margin business (with EBITDA margins over 50%).

Carsales.com cash flow conversion was typically high with pre-tax operating cash flow of $395 million or 99% of reported EBITDA.

Carsales capital expenditure was $86 million in the period, well covered by the group’s depreciation and amortisation charge of $107 million which included $49 million of acquired intangible amortisation.

The following table from the company’s investor presentation reconciles the adjusted and reported figures. Of particular note is the $24.5 million of M&A and restructuring costs and the $37.6 million impairment of investments in FY23.

The M&A and restructuring costs were driven by two substantial transactions during the period being the further 40% purchase of Brazil based webmotors and the acquisition of the remaining 51% of the US based Trader Interactive.

$22.3 million of the $37.6 million of impairments related to the write down of Tyres division which suffered from high freight and warehousing costs and saw its goodwill value reduced to zero. Tyres is Carsales’ online tyre offering and a quick glance at the one year share price for tyre distributor National Tyre & Wheel Ltd (ASX:NTD) implies its challenges were shared by the broader Australian tyre industry over the past year.

Looking to FY24, Carsales has guided to improved revenue and EBITDA on a proforma basis as well as EBITDA margin expansion with all divisions expected to see improvement capping off an impressive set of results.

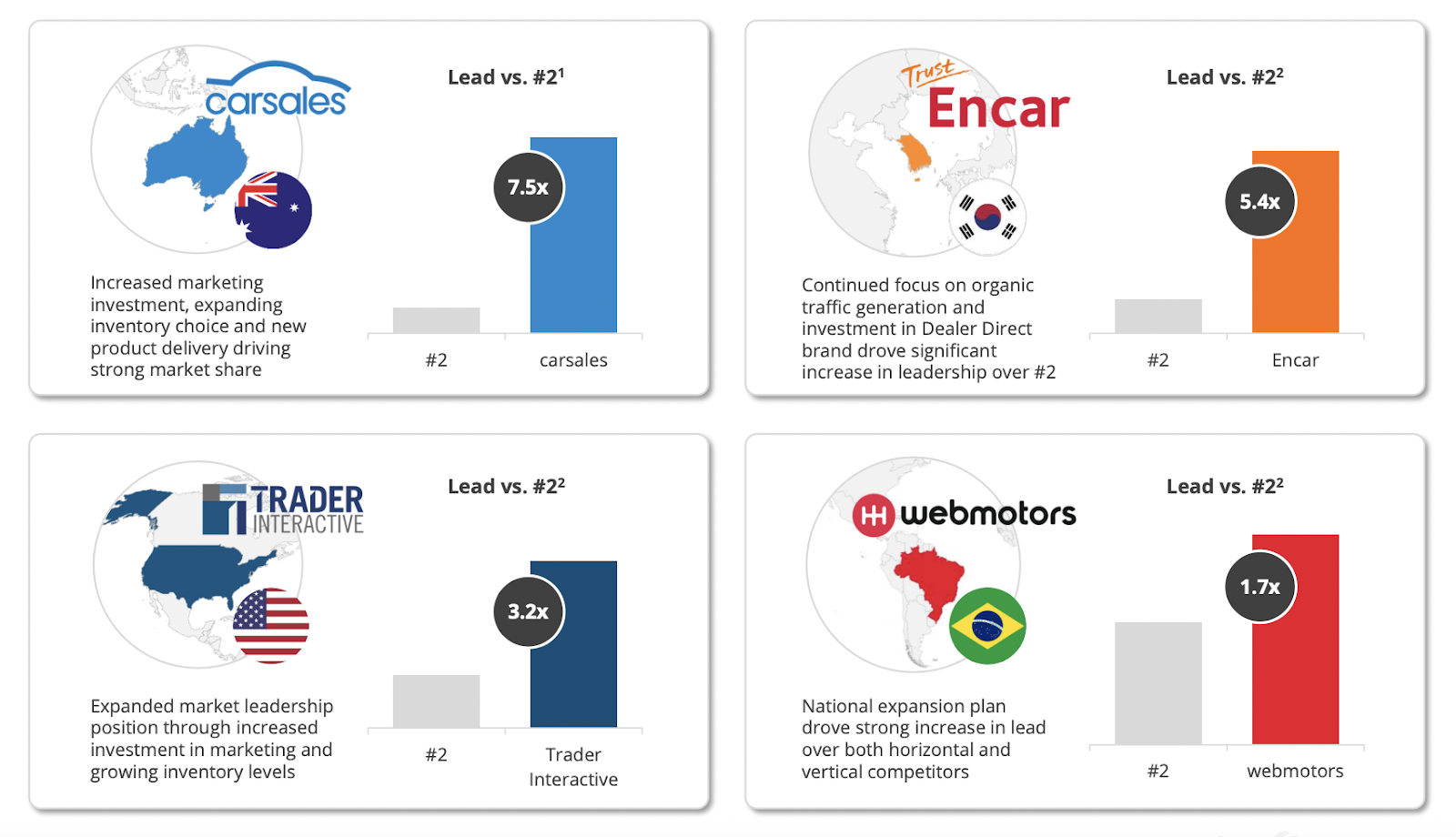

Carsales not only owns the dominant online car selling marketplace in Australia but is increasingly a global business with operations in the US, South Korea, Brazil and elsewhere.

The Australian business is now fairly mature but still delivered decent growth in FY23 with revenue increasing 13% to $399.1 million and adjusted EBITDA up 14% to $258.6 million.

The performance of the Private business segment was particularly impressive with revenue growing 30% over the prior year as technology investment helped to make it even easier for consumers to sell and buy cars online.

Due to limited reinvestment opportunities at home, management has embarked upon an ambitious international acquisition program since 2013 and on a proforma basis more than 50% of revenue is now derived from outside of Australia.

Crucially, each of its core businesses is the outright market leader in its local market. Outsized returns accrue to the market leader in classified businesses due to powerful network effects, though the level of dominance (and therefore pricing power) can vary from market to market. It is a winner takes most industry and incumbents are rarely threatened by competition.

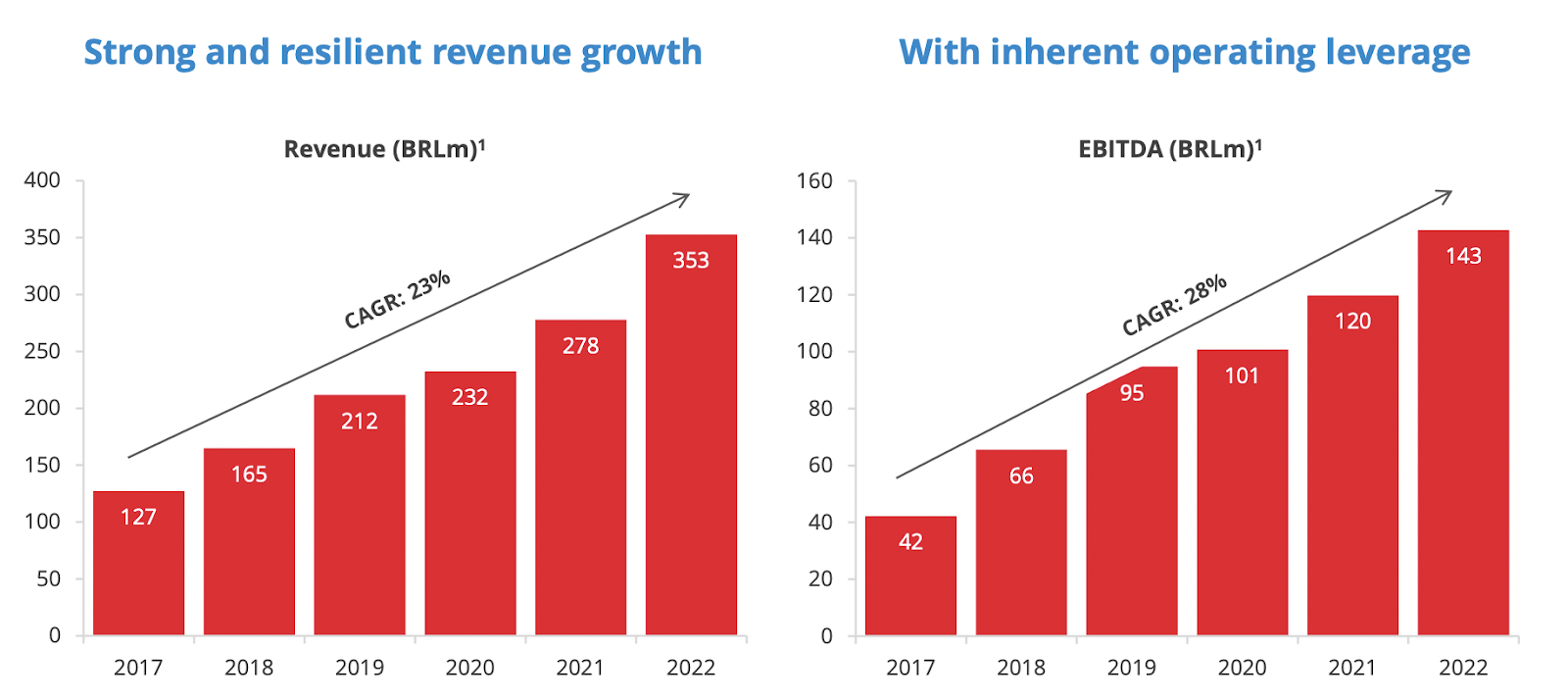

Most recently, Carsales increased its ownership of Brazil based webmotors from 30% to 70% in March this year paying $353 million representing an EBITDA multiple of 21.7. Carsales acquired the original 30% stake in webmotors back in 2013 for $87.7 million when revenues were a fifth of what they are today. Webmotors delivered strong results in FY23 with revenue and ebitda up 29% and 31% respectively in local currency.

Brazil is the fifth largest auto market globally, but webmotors currently generates a quarter of the revenue of carsales’ Australian business which operates in a much smaller market in terms of population and so it appears that webmotors has a long growth runway ahead.

In 2022, Carsales completed the remaining 51% acquisition of US based Trader Interactive at a price representing 21.3x EBITDA. Unlike the rest of the group Trader Interactive is not focused on cars, but owns marketplaces selling trucks, RVs, powersports and heavy equipment. However, like the rest it is a market leader across its categories and in FY23 delivered 14% revenue growth and 17% adjusted EBITDA growth in local currency.

The final major foray overseas relates to Encar, the Korean car marketplace. Carsales purchased the company over two transactions in 2014 and 2017 paying a total of $370 million. It generates 5.4 times the web traffic of its closest competitor and generated $98.6 million in revenue (up 11% in local currency) and $49.6 million in EBITDA (up 12% in local currency) in FY23.

Part of management’s plan is to extract additional value from these businesses by implementing technologies and introducing products and pricing strategies which have proven successful in Australia. Whilst this is likely a sound approach overall, I suspect cultural and other differences may limit its effectiveness. For example, Australia’s GDP per capita is more than seven times that of Brazil and so it seems unlikely that carsales will be able to extract as much revenue per consumer from the Brazilian market as it does from Australia any time soon.

Simply acquiring market leaders will not necessarily lead to outsized returns for shareholders if prices paid are too high. One way to get a clear sense of whether all this deal making is translating to sufficient shareholder value creation is to look at return on incremental capital over time.

Would you like to access all our subscriber only coverage of results season, plus our active Buy recommendations? If so, join the waitlist today!

Carsales return on capital employed (ROCE) analysis

Back in 2013 prior to the purchases discussed above, Carsales generated a whopping return on capital employed (ROCE) of 84% based on EBIT of $117.5 million and average capital employed of $139.7 million. In 2023 ROCE was much lower at 13% as it earned an adjusted EBIT of $374.2 million on an average capital base of $2.8 billion. So EBIT increased by $256.7 million from 2013 until 2023 whilst capital employed increased by $2.7 billion over the same period giving a return on incremental capital of just under 10%.

The picture is even worse than this in reality because over the last decade, carsales has written off investments worth roughly $100 million, which has the effect of reducing capital employed ,and hence slightly inflating return on capital in recent years. Furthermore, the 2013 profit numbers were clean as there was no acquisition accounting whereas the FY23 figures include substantial adjustments as we have already seen.

In light of these incremental returns and given Carsales shares are fairly fully priced with a forward price to earnings ratio of 29 at the time of writing, it seems unreasonable to expect much future valuation uplift.

Therefore, we might expect shareholder returns to mirror recent returns on incremental capital as long as management continues along the same path. Indeed, Carsales has delivered total shareholders returns of 11% over the past ten years during this acquisitive phase which is remarkably close to its return on incremental capital.

Whilst such returns are unspectacular, they are fairly low risk given the dominant positions held by carsales marketplaces globally (with the possible exception of webmotors which is vulnerable to emerging market risks).

On a brighter note, the future prospects of the likes of webmotors and Trader Interactive and the pricing power inherent in market leading online classifieds businesses more generally mean that there is now plenty of opportunity for organic growth. If management were to change tack from dealmaking towards refining the current group businesses then investors might enjoy improved returns, providing potential upside. However, given an incentive structure which is heavily weighted towards EBITDA and EPS targets rather than ROCE, we might be inclined to think that more of the same is in store.

Sign Up To Our Free Newsletter

Disclosure: neither the author of this article Matt Brazier, nor the editor Claude Walker own shares in CAR and neither will trade in those shares for at least 2 days following the publication of this article. This article is not intended to form the basis of an investment decision and is not a recommendation. Any statements that are advice under the law are general advice only. The author has not considered your investment objectives or personal situation. Any advice is authorised by Claude Walker (AR 1297632), Authorised Representative of Equity Story Pty Ltd (ABN 94 127 714 998) (AFSL 343937).

The information contained in this report is not intended as and shall not be understood or construed as personal financial product advice. You should consider whether the advice is suitable for you and your personal circumstances. Before you make any decision about whether to acquire a certain product, you should obtain and read the relevant product disclosure statement. Nothing in this report should be understood as a solicitation or recommendation to buy or sell any financial products. A Rich Life does not warrant or represent that the information, opinions or conclusions contained in this report are accurate, reliable, complete or current. Future results may materially vary from such opinions, forecasts, projections or forward looking statements. You should be aware that any references to past performance does not indicate or guarantee future performance.