This morning wholesale energy industry software provider Energy One (ASX: EOL) announced its FY 2023 full year results, and also announced a “confidential, indicative, incomplete, conditional and non-binding proposal” from a global investment firm, STG, at a price of $5.85, meaning that the share price closed up 34.5% today. On top of that, this article will consider the recently announced cybersecurity breach.

Let’s take it step by step; but first, if you’d like to access all our subscriber only content, join the waitlist to become a supporter, via this link.

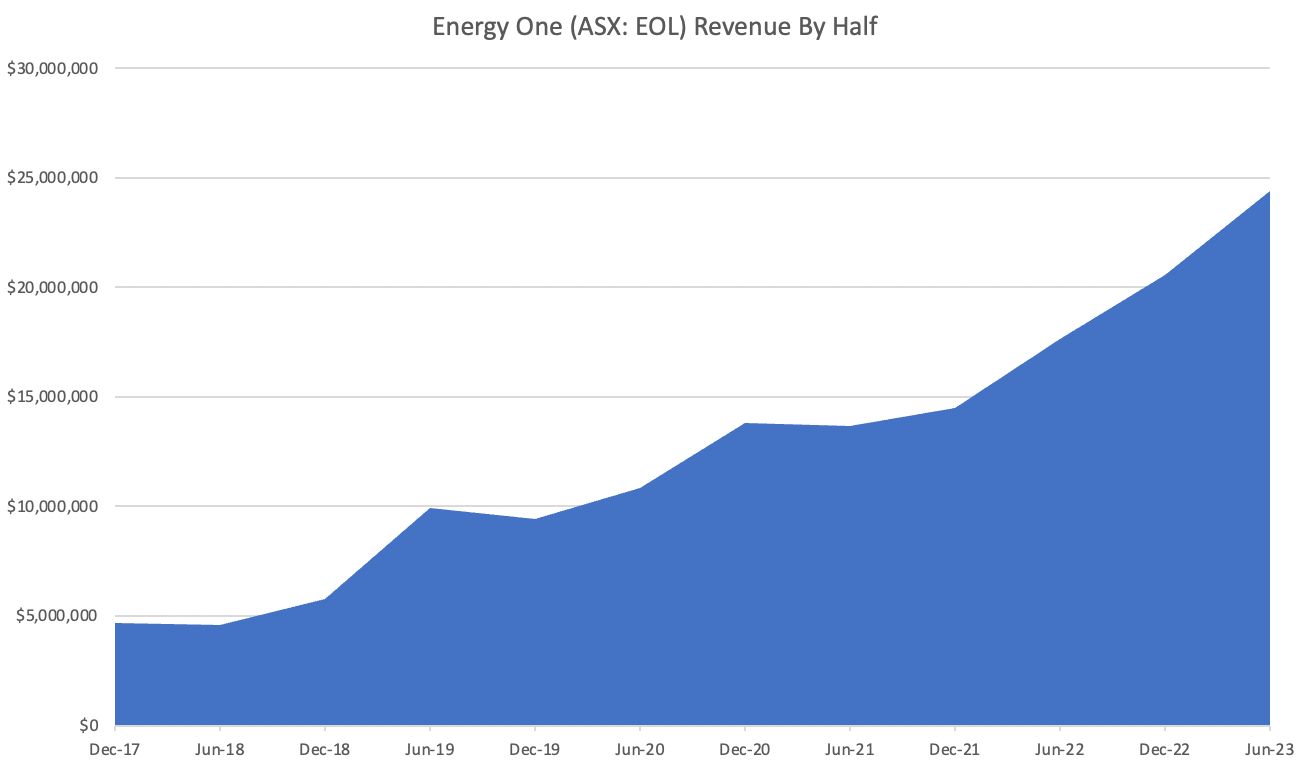

Energy One (ASX: EOL) FY 2023 Results

Energy One reported revenue growth of a whopping 39%, to $44.7 million. However, its annualised recurring revenue (ARR) was only up 19% to $43.8 million, being completely organic growth. Excluding the impact of FX, ARR growth was about 16%, and this is probably a better guide to achievable organic growth rates, going forward.

That said, FY 2024 is shaping up as a bumper year for Energy One’s revenue growth. The CEO said:

“Since my last report we have continued to win accounts with renewables and other participants for our packaged solutions, especially for physical energy players in the form of scheduling software and 24/7 services for solar and wind farms and the like, both in Australia and in UK/Europe.

Further, we have won 2 large accounts in recent months, as well as 4-5 medium accounts and numerous small accounts. Further, we anticipate winning a significant new European-based account in the coming months. This customer is in final contract negotiations with us on what would be a material contract. While there is no guarantee of a signature, we remain confident that our superior technology solution is the best fit for their needs.

We can report that customers are now returning to the market with a distinct uplift in enquiries and trade show attendance. The company has a very strong pipeline of opportunities that we expect to continue working on the year ahead.”

This is extremely bullish commentary from an otherwise very conservative CEO. In particular, the large material European customer could be the massive win we have been waiting for. Not only do large contract wins bolster the bottom line, but they also prove as a huge selling point to win other large customers. That first large customer is often a game changer for a small software stock, so we can only hope that Energy One is in a position to announce the deal before any takeover is consummated. The timing of the takeover offer could be immensely convenient (for the buyer) given the large contract that is in play. But I diverge.

Moving on to profit, the statutory result was weak (as forecast), albeit stronger in the second half. The reason for the weak profit result is that the company is investing so heavily in expansion. These costs include “additional investments in cybersecurity; legal, contractual and technical standards; technical (systems and software) and key global personnel and expertise…” On the bright side, the company says that “To our knowledge, we have an early or first-mover advantage globally, as no other vendor offers a similar global solution.”

As you may notice from the chart above, the dividend has also been cut completely. Personally, I believe they should have cut the dividend last year, and it’s a pity they didn’t. The result is that the balance sheet is quite weak, with net debt of about $19.7 million. This doesn’t need to be a problem, since the company could easily raise enough capital to pay off all its debt. However, unless the company does a fair capital raising (pro-rata rights issue) then we, as small shareholders, face a risk of unfair dilution, and that would be a big problem.

I know that it has been a bumpy ride as shareholders, so you might ask why I’m so sure the company could raise capital. Well, I would point to the offer at $5.85, but also the fact that this is a profitable software stock with honest, competent management, a huge global market, a decent competitive position, and massive long term tailwinds.

Small cap fund managers have told me it is too illiquid to buy, but I think small cap funds would be interested if a capital raising gave them the opportunity to get a decent holding at a good price. However, that does not allay – and may increase – the risk of an unfair capital raising, which is a valid concern for all shareholders.

Moving on to the cashflow, which is the culprit when it comes to the weak balance sheet, we can see that it has suffered from both acquisition payments, and also investment in the technology (in the form of capitalised software costs). That said, it is absolutely worth noting that the investments Energy One are making are still very modest relative to revenue, so I’m not suggesting this investing is wrong (far from it). But it does hurt cashflow, as you can see below.

Another factor impacting cashflow was a buildup of receivables. I asked the CFO about this and he said, “The receivables build is a couple of components being a build of project related WIP and billings as well as FX as the spot rate at 30 June 2023 and 2022 are quite different. We expect the build through projects to unwind through 2024.”

All in all, Energy One is deliberately – having communicated its intentions beforehand – reinvesting its profits in a sensible and attractive growth strategy. To quote the CEO:

“Taking the investment in globalisation out of the equation would have resulted in a 22% increase in PBT, normalisations excluded. To this end we are committed to making prudent investments to accelerate the long-term growth of the company.”

With organic growth running at about 16% in FY 2023, FY 2024 shows all the signs of being a stronger year for organic growth, though profit will remain suppressed and minimal due to ongoing investment. We also have the chance that Energy One reports a breakthrough large contract which could then act as a “proof case” to win other large contracts. These results were acceptable, though the balance sheet remains suboptimal; and that possibly explains the weak share price, due to the spectre of an unfair capital raising.

Energy One Cyber Attack

Towards the end of August, Energy One announced that they had been victim of a cyberattack. They said that “Energy One has continued to do business with our valued customers through this incident. Our response partners at CyberCX have so far identified only activity within Energy One’s corporate systems. No malicious activity has been identified on customer-facing systems.”

Already, for quite some time, Energy One has been working towards an improved security posture. In fact, back in September 2020 they said:

“The ISAE implementation provided us [with] an implementation of an important subset of controls and control activities of the ISO 27001 framework. To move further on our implementation track for the ISO project we currently have designed all the ISO 27001 documents. The next step now is to translate these documents / policies into clear procedures / automated checks and coach our employees in using them.”

Suffice it to say, this clearly should have been more of a priority, and it’s fair to say that the company has made a mistake in not prioritising cybersecurity more than it has. However, on the flipside, their disclosure and transparency around the incident has been good, compared to other companies who might try to cover up such a thing. So therefore I think a mistake has occurred, but it does not go to integrity, and therefore isn’t anywhere near as bad as a mistake that undermines my confidence in management integrity.

Obviously, with a large contract in the works, and a few good sized wins, the information on Energy One’s corporate networks would have been very valuable to anyone who was considering buying shares.

Energy One will be holding a public shareholder briefing at 2pm on Wednesday, 30th of August accessible by this link. On the off chance that my personal family obligations occur at the same time, I may not be able to attend, so I would appreciate if somebody could ask about attribution of the cyber incident. From the public announcements, it sounds like the hackers had access to information which would have let them know about Energy One’s increased pipeline and contract wins, though it would also be good to clarify this.

It is very important, in my view, that Energy One discovers who did the cyber attack, so they can refer them to the authorities, in order to disincentivise future attacks. If the current consultants are unable to answer that question, Energy One may need to talk to a larger cybersecurity company with a larger proprietary intelligence database.

Energy One Takeover Offer at $5.85

Today, Energy One announced a confidential, indicative, incomplete, conditional and non-binding proposal from a global investment firm, STG. STG has $10b under management and bills itself as “a private equity firm focused on fueling innovative software, data, and analytics market leaders in the mid-market.” It’s pretty obvious they see a lot of potential for Energy One, and if indeed Energy One is about to win a breakout contract, then their timing is particularly good.

This is the major event impacting the share price today.

Notably, the announcement says that “the Board of the Company (other than Mr Vaughan Busby) intends to recommend that Energy One shareholders vote in favour of the Potential Transaction and to vote or procure any Energy One shares they own or control be voted in favour of the Potential Transaction.”

This implies that Mr Vaughan Busby may be stepping up into the “white-knight” role for those long term shareholders who wish to participate in the long term opportunity that Energy One is pursuing. If Mr Vaughan Busby votes his shares against the proposal, then there is a good chance it will not go through.

I have requested a more up to date copy of the share registry, but according to the most recent one I have, Mr Busby owns around 4.265 million shares. During the day, I have been in contact with another large shareholder, who, alongside a couple of other shareholders he is in contact with, hold around 1.6 million shares. And they do not seem keen on a takeover.

Looking at the registry, I do recognise a fair few names, and based on my interactions with other shareholders on twitter, I estimate that there are at least 200,000 worth of additional shareholder votes against this takeover. And as I speak to more people that number could grow considerably.

All in all, I think it is reasonable to expect that if people are of the same view I am (and that’s a big if) and if Mr Busby is our white-knight (and that’s a big if) then there is every chance that at least 6 million shares (and possibly quite a lot more) would vote against the proposal.

At present, there are only 29,947,020 Energy One shares on issue, that 6 million against would represent a hefty 20% in opposition. Based on the information I’ve gathered so far, and contingent largely on Mr Busby’s intentions, I think we are very likely to see at least 20% in opposition.

Furthermore, we only need a few smart larger holders, and I have a few in mind, to oppose the takeover, and we easily get to another 1.5 million in opposition. Add to that a strong, rather than weak, retail shareholder opposition, and we can probably add another 200k against. That gets us to around 7.7 million against – or roughly 25% of the company. So this takeover at $5.85 is far from guaranteed. In my opinion, Energy One might be in play, but the takeover is not a foregone conclusion.

As I understand it, in order to compulsory acquire shares, the acquiring company would generally need 90% acceptance. I think this is a bit of a long shot, at $5.85.

Edit: Another possibility is a special resolution adopting a scheme of arrangement, which as I understand it allows a takeover with 75% of the vote.

However, if STG decided to do an on market takeover, then they could quite possibly accumulate 50% of the company. That would put them firmly in the driver’s seat.

Instead of a veritable titan of business administration like Ian Ferrier, a good long term steward like Andrew Bonwick, and the long term architect of operational growth in Shaun Ankers, we might bow to the will of a foreign private equity firm. To put it mildly, I would not have much confidence in that situation.

So what might happen? There are four likely scenarios that come to mind (though these are not exhaustive).

Scenario 1

Shareholders resist this bid, which undervalues the company. The bidders, or another party, come in with a higher bid. Eventually, the bidders make an offer that is too compelling, and they takeover the company. We still lose the potential for a multiyear multibagger, but at least we get more than $5.85.

Scenario 2

Shareholders agree to this bid. My shares are forcibly acquired, and I am sad; because in my opinion being forced to sell at $5.85 is like being forced to sell Altium or Pro Medicus or Objective Corp or Xero before they had the chance to prove their immense market opportunity and high business quality.

Scenario 3

Shareholders resist the bid. Eventually STG walk away and there are no other bidders. The share price drops, perhaps to around $4 to $4.50, where it was prior to the proposal.

Scenario 4

STG takes a look at Energy One, and decides not to proceed with its offer of $5.85. The share price drops harder, perhaps to $3.50 to $4.

What should short term investors do?

Since I recommended Energy One, shareholders have had a tough time. As recently as June, anyone who bought on my recommendation was underwater.

If you’ve been on the rollercoaster, and you hated it, well now is the time to get off, and I would seriously rethink investing in small caps at all – this sort of rollercoaster is the rule, not the exception.

If you hold shares in Energy One after this takeover offer then there is every chance the share price will go down. If, as I would like, the takeover does not proceed, then it is quite possible the share price could fall to around $4. For me, Energy One is a 10 year thesis.

There is nothing wrong with taking a short term profit, and if that’s what you’re looking for, I’d book it now.

What will I do as a long term investor?

As a long term investor in Energy One, my preference would be to participate in what I believe is a growing, well managed company with a very strong high recurring revenue business model and honest competent management. I don’t want the current set up to change, as I think it is a great set up, and I struggle to find one I prefer on the ASX.

If you can find any small ASX company with high insider ownership, profits, organic revenue growth of over 15%, high retention rates, long term tailwinds, and global reach, all available for < 4x ARR, please tell me about it. I will happily buy you a beverage in exchange for that.

Therefore, my immediate response to this announcement is to do nothing. If I were asked to vote on at transaction at $5.85, I will vote against it. For now, I will busy myself talking to as many other shareholders as I can, to get a better feel for whether there is support for a transaction at this price.

I will likely write some sort of update in the next week or so, in response to both further research and also the conference call on Wednesday.

Additional note 12.11am 29 August: Thinking about this is keeping me awake.

I believe that Energy One could well quadruple its revenue in a decade, implying growth at little more than the current rate of around 16% assuming no more acquisitions. And you do not need much vision to realise that Energy One could well make net profit margins of 15% once it achieves that sort of scale.

Even if margins were lower than 15%, and/or Energy One did less than 16% per year growth, then annual profit could be $20m in 10 years. By then, EOL would probably have an even higher P/E multiple (looking at the market today, anyway). But even if it only had a P/E multiple of 40, that would be a market capitalisation of $800m, compared to the indicative offer which values it at ~$175m.

I do not believe that it is generally helpful to give these sort of long term estimates, as they could obviously be very very wrong, but I do so now to explain better why I am not excited by a takeover at $5.85.

To access all our subscriber only content, join the waitlist to become a supporter, via this link.

Disclosure: the author of this article owns shares in EOL and will not trade shares in EOL for at least 2 days following the publication of this article. Please keep in mind the author may buy or sell shares after this date. This article is not intended to form the basis of an investment decision and is not a recommendation. Any statements that are advice under the law are general advice only. The author has not considered your investment objectives or personal situation. Any advice is authorised by Claude Walker (AR 1297632), Authorised Representative of Equity Story Pty Ltd (ABN 94 127 714 998) (AFSL 343937).

The information contained in this report is not intended as and shall not be understood or construed as personal financial product advice. You should consider whether the advice is suitable for you and your personal circumstances. Before you make any decision about whether to acquire a certain product, you should obtain and read the relevant product disclosure statement. Nothing in this report should be understood as a solicitation or recommendation to buy or sell any financial products. A Rich Life does not warrant or represent that the information, opinions or conclusions contained in this report are accurate, reliable, complete or current. Future results may materially vary from such opinions, forecasts, projections or forward looking statements. You should be aware that any references to past performance does not indicate or guarantee future performance.Save time at tax time: If you’d like to try Sharesight, please click on this link for a FREE trial. It saves heaps of time doing your tax and gives you plenty of insights about your returns. If you do decide to upgrade to a premium offering, you’ll get some discount (the best deal available, I’m told) and we’ll get a small contribution.