Prophecy International Holdings Limited (ASX: PRO) is a software and SaaS company serving both mid to large enterprise and government customers on a global scale.

The company reported its full year results at the end of August with little fanfare. Revenue grew by a promising 19% to a record $19.6 million and Annual Recurring Revenue (ARR) grew by 26% to $23.2 million. Disappointingly, the loss for the year grew by 47% to $2.47 million and operating cash flow went from an inflow of $2.9 million in 2022 to an outflow of $1.2 million in 2023.

So why could this be a hidden gem? First, let’s dig a little more into the company.

So What is Prophecy International?

As mentioned above Prophecy is a global software business with clients including State and Federal Governments, military and defence agencies, Banking & Finance, Energy, Oil & Gas, Health, Retail and Technology sectors.

The company commenced operations in 1979 and listed on the ASX in 1997. The business today looks very different to what it was back 40 years ago. Having shed legacy segments in 2017 Prophecy now has two products today. eMite, which was purchased in 2015 and Snare, which was acquired through the purchase of Intersect Alliance in 2011.

eMite

eMite develops real-time analytics and dashboard solutions with its mission to collate data and present it in a useful fashion.

eMite targets the contact/call centre industry and more broadly the Customer Experience (CX) market segment. The product aims to enhance efficiency and improvements in operations and customer engagement. The business prides itself on customers being able to create integrations and customised dashboards without a coding or data science background.

Updated Investor Presentation 31 August 2023

The software can draw its data from multiple systems and third party applications like Salesforce, Microsoft, Oracle, Atlassian, Snare, and Genesys. eMite also provides adaptors to onboard data from more generic data sources like a database or an Excel file. It will then generate Key Performance Indicators (KPI’s) based on real time and historic data. These can be customised to the needs of the business. The company believes it has a number of advantages over its competition. Management boasts that they are the fastest to onboard data and can handle enormous quantities. The more data to manage the more significant the integration and therefore the likelihood the client continues to utilise the product. This can make for sticky software.

Having read through the limited reviews I could find, I decided the visualisation of the product and real time data were strengths for eMite. However, I also noted this cheeky self- review; if you don’t love yourself…

Snare

Snare is in the highly competitive, cyber security space. This is interesting because cyber security is constantly increasing in complexity, and has a long tailwind.

It provides critical government recommended or mandated security controls, including cyber threat detection, security information and event management (SIEM), alerting, forensics and centralised log management.

The monitoring solution is designed to answer three questions:

“Did someone get in?”

“How did they get in? “

“What did they see/take/change?”

The software product allows customers to collect security data from a variety of end point devices and cloud-based systems. Snare’s competitive advantage is the military grade product having been designed by ex-military personnel. The solution can be deployed on premise, in the customer virtual private cloud and in highly secure air-gapped environments. As a result, Snare is a compelling product for heavily regulated government and business. Snare prides itself on providing simplified log collection and data storage. The product is centrally managed and does not require a specialist to operate.

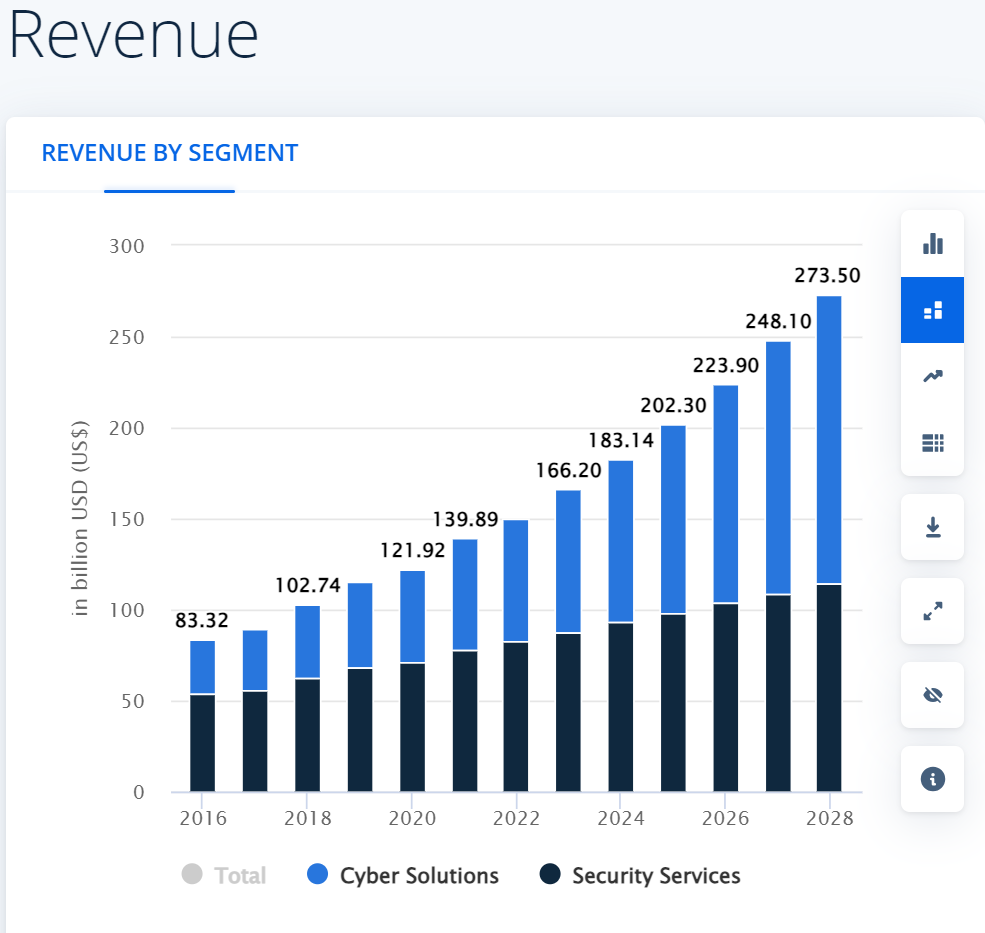

Cybersecurity is a highly fragmented industry.

While there are many competitors and some of them are amongst the largest companies in the world, they can’t cover every niche. This leaves a large enough addressable market for many players to fit. Statista estimates that the total revenue from cyber solutions and security services will reach US $273.5 billion by 2028:

While the two products are not linked they both share the commonality of high data ingestion.

Prophecy is focussed on a partner-led growth strategy. eMite is sold exclusively through implementation partners which include Amazon’s AWS Marketplace and Genesys. While Snare is sold both directly to the customer and through Managed Security Service Providers (MSSP’s) and Managed Service Providers (MSP’s).

In August 2022 Prophecy signed a master service agreement with Optus covering the supply of both eMite and Snare to Optus group companies and customers. This has been followed up in recent times with a partnership agreement with Oracle to co-sell Snare and eMite to more than 430,000 of Oracle’s customers.The success of these types of deals were proven with Snare’s March 2023 deal with the UK Royal Air Force and previous deal with the UK Royal Navy facilitated by key partner and reseller Fujitsu.

The company recently demonstrated both products which can be viewed on YouTube here.

So Who Runs Prophecy International?

Prophecy is led by CEO Brad Thomas who has been at the helm for close to 7 years.

The former triple paralympic medalist is passionate about culture led change. He began with the business through eMite shortly after it was acquired. One thing to note is that Thomas holds 86,681 shares in the company. This accounts for less than 1% of the key personnel holdings of 11,473,106 shares.

Of those key personnel, long standing executive director Edwin Reynolds holds almost 8 million shares. Reynolds joined Prophecy as general manager in 1987 and was appointed Non-executive Chairman in December 2006. His 10% holding of the company ensures alignment with shareholders and has been a fairly consistent purchaser over the years.

While not a red flag in my book, it would be nice to see the CEO with a little more skin in the game, as a vote of confidence, especially given the lacklustre share price movement over the last few years.

What Could the Market be Missing About Prophecy International?

As mentioned at the top the full year financial results were okay but nothing spectacular.

The positive signs are that revenue continues to grow with ARR benefiting from Snare’s recent strategy change to move from perpetual licensing to a subscription model. Subscription revenue accounted for 50% of the Company’s total new Snare sales in FY23 up from 25% in the prior period. Total group ARR increased by 26% year on year to $23.2 million.

While perpetual licences are the preferred contracts for government agencies, the shift to a subscription licence would make it easier to pass on price increases and new modules to customers.

2023 Statutory Accounts

A tough comparison period

In FY22 Prophecy locked away its largest contract in history.

The eMite deal with Humana represented $6.07 million in total contract value over three years. In the same period Snare also secured its largest ever individual sale of over $700,000 to the UK Government. This led to an ARR increase of 74% to $18.7 million. In comparison the company ‘only’ increased ARR this year by 26%. The company has more than doubled its ARR since 30 June 2021 from $11.5 million.

Why the loss?

Expanding revenue is great but if employee expenses exceed that growth, it’s a problem. Increasing expenses were driven by a combination of factors including:

- Inflation and the demand for skilled employees

- Taking the Manilla technical staff team in house having previously used a third party

- Development spend.

- Customers taking longer to consider products. The longer it takes to onboard a customer, the more staffing power is required to see the sale through.

- Migrating its own data centres into the cloud

While the ‘war on talent’ isn’t going anywhere, Prophecy management are confident that they won’t be looking to add to headcount. A number of the above points are concluding, so I think the likelihood of another jump in costs is low. My thesis is that revenue will continue to grow while costs grow more modestly or stay roughly flat.

Despite the cash out flow for 2023, the company had a significantly improved second half.

Cash at bank as at 31 December 2022 was $9.7 million and finished the full year at $11.3 million. While a weakening AUD played a part, the significant driver of growth was in cash receipts of $12 million compared to $8.5 million in the first half. Payments to suppliers were steady half on half at $11 million, hinting at the potential for a future cash flow positive result. However, a number of significant large customers were invoiced for their annual eMite subscription in the second half which perhaps warped the result.

A Cash Flow Inflection Point?

The Prophecy International team believes they can be cash flow positive in the first half of 2024 and for the year. The company is currently targeting a small earnings before interest tax and depreciation (EBITDA) profit. If Prophecy International can continue to maximise the relationships it has built with its channel partners, perhaps we are at an inflection point for the business. Time will tell, but we do have some metrics to follow leading up to the first half results.

On top of that, on the full year results call, Prophecy International CEO Brad Thomas boasted a lofty goal of reaching $50 million in revenue in the next few years.

If we assume the $23 million of 2023 ARR level is converted to revenue, plus it wins additional government contracts, we could see FY24 revenue between $25 – $26 million. This would imply revenue growth of around 30% and the company would require a further 40% growth each year to reach $50 million by June 2026. Ambitious.

In the near term, if Prophecy could achieve ~$25 million in revenue with moderate growth in costs we could see a profit closing in on $1.5 – $2 million. At a current market cap of $44 million a price to earnings multiple in the mid 20’s which I feel is reasonable should this level of growth be achieved. A number of larger growing tech businesses are in another dimension when it comes to these types of valuations.

I currently hold shares in Prophecy with a close eye on the next 6-12 months. While the financial results for the past year may not have set the world on fire, the underlying growth story remains intriguing. While there are challenges ahead I believe Prophecy is worth further research as a potential hidden gem in the ASX small cap space.

Cover Image “Hidden Gem” attribution to jesswoodhouse.com

Disclosure: The author of this article Nick Maxwell does own shares in PRO. The editor Claude Walker does not own shares in PRO. Neither will trade PRO shares for at least 2 days following the publication of this article. This article is not intended to form the basis of an investment decision and is not a recommendation. Any statements that are advice under the law are general advice only. The author has not considered your investment objectives or personal situation. Any advice is authorised by Claude Walker (AR 1297632), Authorised Representative of Equity Story Pty Ltd (ABN 94 127 714 998) (AFSL 343937).

The information contained in this report is not intended as and shall not be understood or construed as personal financial product advice. You should consider whether the advice is suitable for you and your personal circumstances. Before you make any decision about whether to acquire a certain product, you should obtain and read the relevant product disclosure statement. Nothing in this report should be understood as a solicitation or recommendation to buy or sell any financial products. A Rich Life does not warrant or represent that the information, opinions or conclusions contained in this report are accurate, reliable, complete or current. Future results may materially vary from such opinions, forecasts, projections or forward looking statements. You should be aware that any references to past performance does not indicate or guarantee future performance.