Surface engineering company Laserbond Limited (ASX:LBL) released its half year results earlier today and the market did not like them. The share price is down 24% to 55 cents at the time of writing.

When we last covered Laserbond on Ethical Equities, I concluded:

“Whilst half on half revenue excluding technology was slightly lower and there is a decent chance that the coming year will be one of consolidation, I think Laserbond shares remain good value over the long term and I will be holding on to my shares.”

At the time the shares were priced at 57 cents and so have pretty much done a round trip.

Following last year’s results, Laserbond’s share price rose to over 90 cents. Clearly, the market did not agree that the coming year would be one of consolidation. I thought that the stock had become overvalued and so sold 60% of my shares at an average price of 85 cents. I disclosed this on my blog at the time and Claude did the same in an email to subscribers.

Fast forwarding to today, I was holding a roughly 2% position size heading into the results announcement. Upon first glance at the numbers, I thought the shares were oversold and bought a small quantity at 51 cents. Then, upon revisiting my valuation I changed my mind and immediately sold them for the same price. My current view is that I’d consider adding at under 40 cents and do not intend to sell at these prices in the absence of new information.

The reason I revised down my valuation is because Laserbond failed to deliver double digit revenue growth this half as promised in its FY 2019 outlook statement. The same guidance was reiterated at its AGM in October when management disclosed that sales for the first quarter were up 18%.

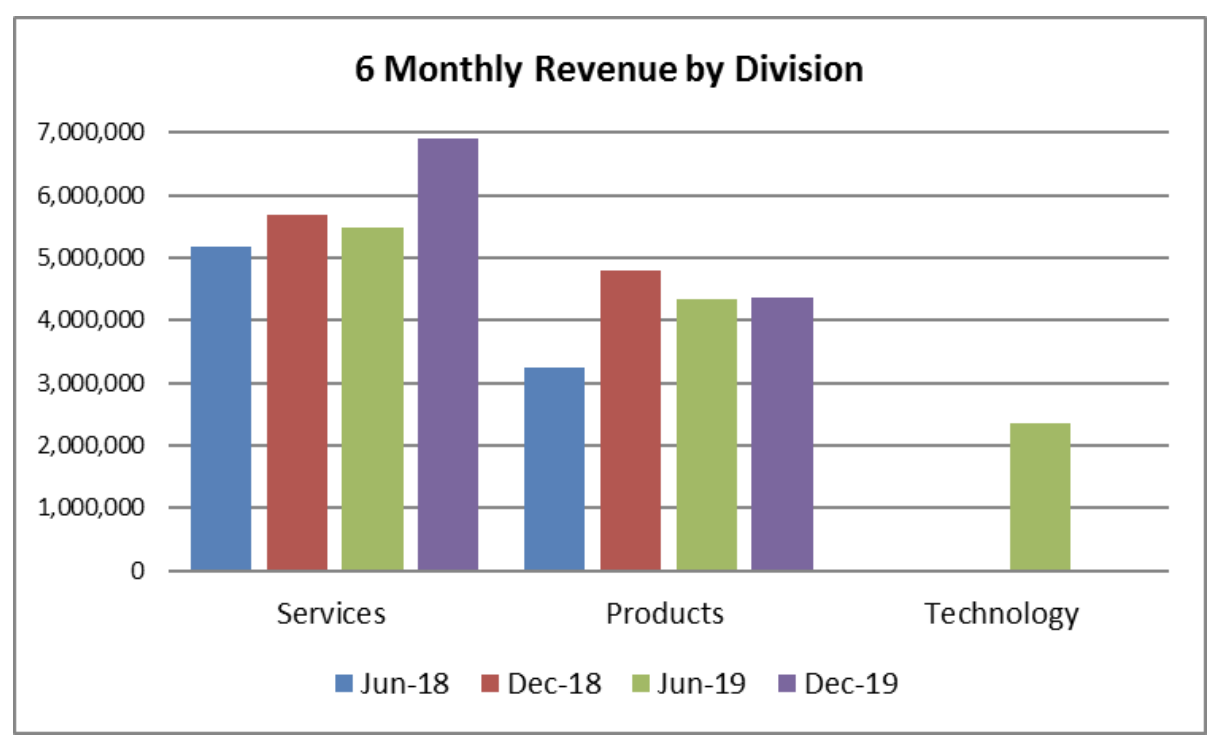

Total revenue was up 7.3% to $11.2 million, with Services up 21.1% to $6.9 million and Products down 9.1% to $4.4 million. The performance of the Products division is what disappointed me because my thesis is based upon this part of the business being the main growth driver for the group, in time yielding economies of scale. I had expected more rapid growth from this division than we are currently seeing, hence my valuation downgrade.

Management said that the weak Product sales were due to timing and remains very optimistics about the future prospects of this business segment. They commented that orders actually increased 1.7% over the first half of last year, but this hardly represents double digit growth.

To be fair, Laserbond is an industrial manufacturer with a lumpy sales profile and so it could be argued that six months is too short a period to pass judgement, especially given the miss was fairly small. And management reiterated both double digit revenue guidance for the full year and their target of $40 million in sales by 2022 in this half year report. Management also expects that a new OEM customer win in December will add $0.7 million Product revenue per year and for orders to ramp up from a large US customer for its Steel Mill Rolls.

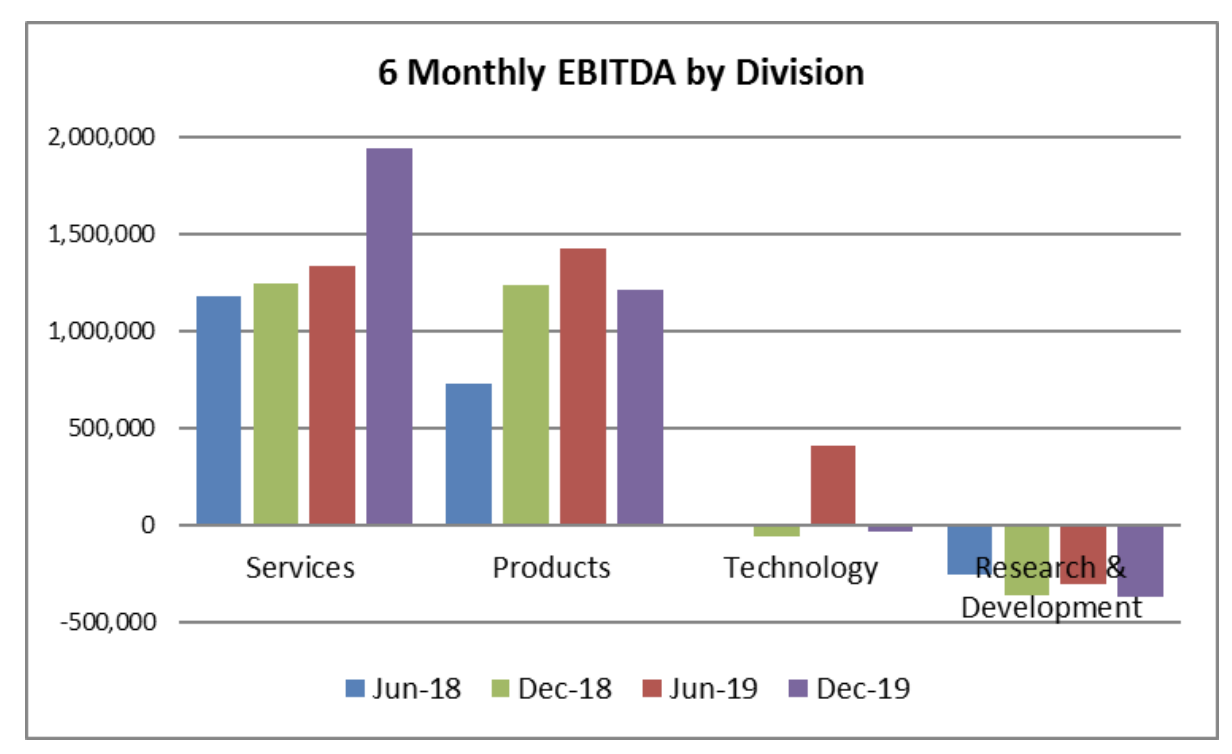

Along with strong growth in the Services division, the highlight of today’s report was the 240 basis point improvement in gross margin to 49.6%. Statutory net profit after tax (NPAT) fell 2% to $1.2 million, but was up 15.7% to $1.2 million on an underlying basis. Underlying results exclude the impact of grant income included in last year’s figures.

The board declared a 0.5 cent interim dividend in line with last year. The balance sheet remains strong with $1.7 million in cash offset by $3.1 million in hire purchase lease liabilities. Cash flow from operations was low at $0.6 million compared to $1.8 million in the first half of last year. This was due to a $1.3 million adverse movement in working capital which will average out over time and so does not concern me.

Laserbond’s results for the second half of last year benefited from a technology sale to a UK multinational. There is a recurring element attached to this deal which will contribute revenue from March 2020. This will not be equivalent to the upfront fee and so unless management secures another technology licence sale in the coming half, there is a chance that Laserbond’s full year results will disappoint once again.

We are halfway through the year and my expectation that FY 2020 would be a year of consolidation for Laserbond looks to be correct. There is nothing in today’s report that makes me think the company’s long term prospects have significantly deteriorated, but I am more cautious about the sales trajectory of Products than I was previously. I think that today’s price fall is more a consequence of unrealistic market expectations than this being a particularly poor result.

Laserbond is a cyclical industrial manufacturer with some valuable technological know-how. At the time of writing the stock has a price-to-earnings ratio (PE) of around 20 based on my forecast FY 2020 earnings. I think this is fair to fully valued for this type of company and I intend to continue holding at these prices in the absence of a better opportunity.

Matt owns shares in Laserbond and will not trade the stock for at least two days following the publication of this article. This post is not intended to be advice. If in doubt, read our disclaimer.