Medadvisor Ltd (ASX:MDR) released an improved set of results for FY23 earlier today as presaged by a strong performance at the half year.

Revenue increased 44.6% to $98 million and EBITDA improved from a loss of $11.3 million to a loss of $3 million.

Gross profit grew faster than revenue, up 69.7% to $59.4 million as gross margin rose nine percentage points to 60.6%. Gross margin progress relates to a shifting product mix at Medadvisor’s US business, Adheris, which I will examine more closely later in this article.

Loss before tax ameliorated from $17.7 million to $10.5 million and loss per share more than halved from 4.63 cents to 2.07 cents.

It is worth noting that the group incurred significant depreciation and amortisation charges of $5.4 million during FY23, up from $4.9 million last year. These relate mainly to past acquisitions and ongoing internal investment in fixed assets is minimal ($0.2 million in FY23 and $0.3 million last year). Therefore, Medadvisor EBITDA is probably a better guide of the direction of business performance than other profit measures in this instance.

Medadvisor cash was $14.2 million offset by $12 million of debt as at 30 June. Net current assets were negative $5.1 million raising the spectre of a further capital raise given Medadvisor is yet to reach cash flow break even.

On the other hand, some Medadvisor investors may take comfort from the following statement in today’s release:

“As we enter FY24, our focus is on delivering sustainable Revenue growth, positive EBITDA, and enhanced operating cashflows.”

Restructuring costs of $3.4 million in FY23 ought not to repeat in FY24 and are expected to deliver $2 million of annual savings. If so, this might be enough to stave off a further issue of equity all else being equal.

All else is rarely equal though, and I’d be surprised if it proved so in this case given Medadvisor benefited from some one-off covid related revenue in its US business in FY23.

For FY23, operating cash outflow was $1.5 million compared to $0.2 million last year and free cash outflow including lease payments was $2.9 million up from $2 million.

The Medadvisor share price closed up 9.5% at 23 cents on a low volume day with just $114 thousand worth of shares traded. The volume weighted average price was 20.94 cents, in line with the prior close of 21 cents.

As a reminder and for those who are not aware, Medadvisor provides technology which connects patients to pharmacies and pharmaceutical companies. The business was founded in Australia where it has over three million users and boasts over 95% of community pharmacies as customers. Medadvisor also has a substantial business in the US.

Australia

In Australia, patients can download the Medadvisor app for free which allows them to order medicine remotely from their local pharmacy. This is attractive for both users and pharmacies because it reduces queue time when collecting prescriptions. Users also receive notification reminders for when to take medicine and when to refill scripts.

Medadvisor’s pharmacy software is called PlusOne and is how pharmacies receive communication sent from the patient app. In addition to reduced queue times, pharmacies using PlusOne benefit from improved customer loyalty and potentially higher revenue per customer because of better medical adherence.

One feature that enables improved adherence is automatic script renewals which notifies a doctor when a prescription needs renewing. Additional features include drug delivery management and customer record keeping.

Pharmacies pay a subscription for Medadvisor’s software which costs $189 per month for a standard package. Payment, text message and other transactional fees typically add a further ~$80 per month based on company data for FY 2022.

Source: Medadvisor accounts

In Australia, Medadvisor enjoys a dominant market position in a defensive growing sector with sticky customers. This should make for a terrific business, but the division consistently loses money as you can see above. This is at least partly due to the relatively small size of the Australian market which in turn explains the company’s decision to enter the US.

That said, I suspect it would be fairly straightforward for Medadvisor to turn a profit in Australia by stripping out costs and pushing through price increases.

These actions are already in motion. The Australian business incurred $3.4 million of restructuring costs in FY23 (explaining the increased operating loss with savings expected next year) and Medadvisor implemented a 19% price rise in January 2023. The latter resulted in less than 2% customer churn affirming the quality credentials of this part of the group.

$4.5 million of the $5.9 million revenue growth in FY23 relates to the acquisition of Guildlink during the year for $9.1 million. This implies that organic growth was 10% during the year.

I estimate that Medadvisor’s Australian division is conservatively worth at least $50 million. This is based on the fact it generates $20 million of high margin recurring revenue and has a monopoly.

The US

Medadvisor has a substantial business in the US thanks to the acquisition of Adheris in late 2020. Adheris generated $78.1 million in revenue in FY23 (up 46% on the prior period) and an operating loss of $2 million, down from $10.5 million.

Unlike Medadvisor’s Australian business, Adheris does not provide an ordering system for pharmacies. Instead, it sends information about drug therapies to patients who have opted in to receive such communication via their pharmacy. Whereas pharmacies are the main customers for Medadvisor’s Australian business (though the MedAdvisor App can also be used to communicate messages from pharmaceutical companies), Adheris generates revenue primarily from pharmaceutical companies whose goal is to increase adherence.

Prior to Medadvisor’s involvement, Adheris mainly communicated with patients via letters through the mail. Since the takeover, Adheris has developed a digital platform called THRiV and consequently communication is increasingly done through digital channels. Incidentally, medical adherence communication is a growing (but still small) revenue stream for the Australian business too.

Adheris is a seasonal business with the December quarter typically seeing an uplift due to the flu season. Last year saw a particularly pronounced jump in Q2 revenues as we can see below. This was partly due to covid top up vaccination programs which are unlikely to repeat in future years, at least not as lucratively.

Source: Medadvisor quarterly statements

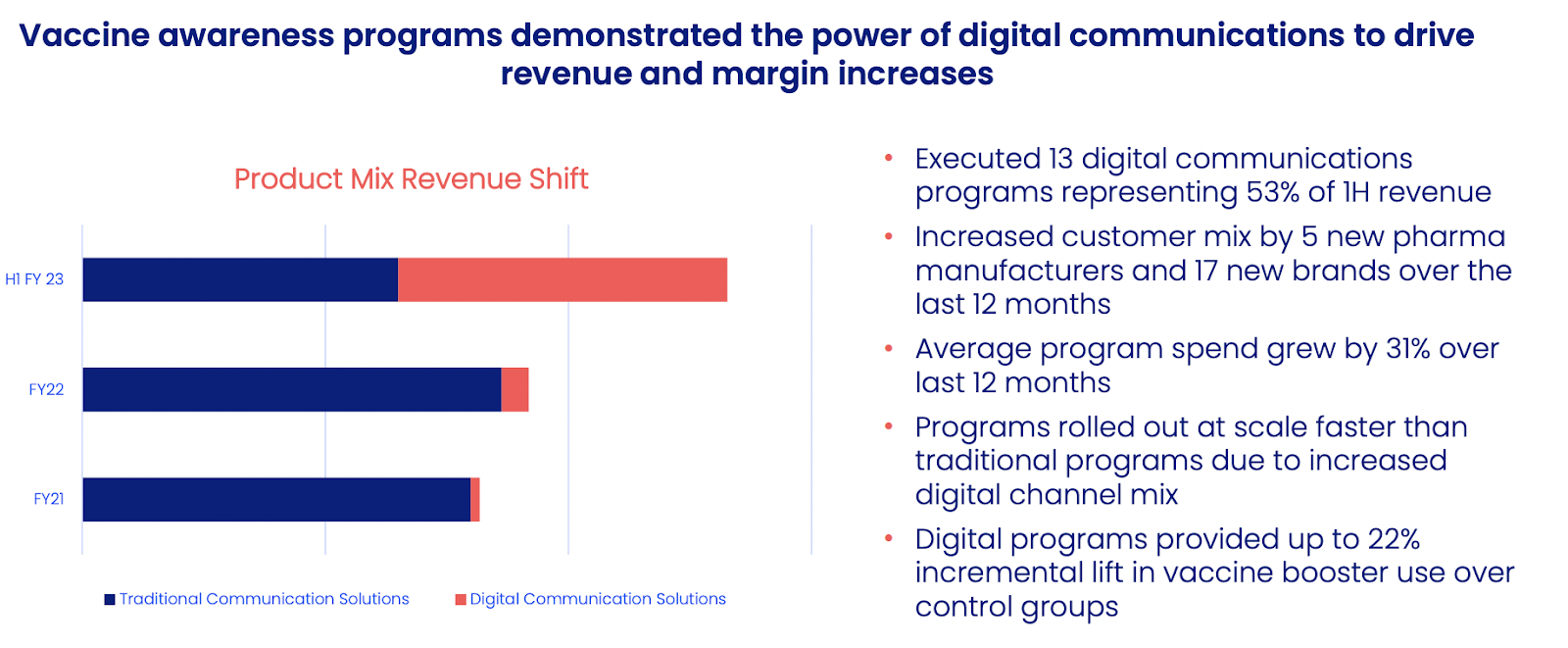

The transition to digital is still ongoing as Adheris steadily converts its existing pharmacy network to support digital communications. Currently, 90 million patients can receive digital communications, an increase of 96% over last year.

Adheris claims to have a database of 230 million patients and so on this basis the digital transition is around 40% complete.

There are three key benefits of the new digital platform which ought to drive profitability.

- Digital channels are lower cost when compared to traditional mail driving gross margin progress. Adheris gross margins rose 43.3% to 54.6% over the past year.

- Digital is usually the preferred form of communication for consumers which translates to greater reach for pharmaceutical companies. Medadvisor’s average vaccine program spend in the US Winter 2022 season increased 31% versus the prior year on the back of the uptake of digital solutions.

- Digital enables the capture of data such as click through rates which enhances analysis of program ROIs.

Source: Medadvisor HY23 investor presentation

Although gross margins are improving, Adheris is not as profitable as Medadvisor’s Australian business which boasts gross profit margins of circa 85%. The reason for this is that Adheris shares revenue with pharmacies in order to access their customers via “abatement” fees.

These fees vary by pharmacy chain. It stands to reason that larger chains are able to command higher fees, although I can’t be certain as it is not something that Medadvisor discloses publicly. However, if I am right then further consolidation of US pharmacies would be a potential headwind to Adheris.

Adheris is not as strong a business as the Australian operation as it is beholden to pharmacies who own the relationship with the patients. Whereas it is difficult to see Medadvisor competition emerging in Australia, it is quite possible that US pharmacies could sell access to their customers to potential competitors of Adheris.

Management & US market structure

US based CEO Rick Ratliff joined in July 2022 and was previously CCO at ConnectiveRx (an indirect competitor to Adheris).

ConnectiveRx is focused on helping patients to access drug funding and improving adherence. It communicates with patients primarily through drug commercials. As CEO Jim Corrigan explains,

“Usually at the end of those drug commercials, there’s a message asking viewers to contact various companies if they need some help from an economic standpoint, and that’s where ConnectiveRx comes into play.”

ConnectiveRx also targets prescribers via information sent through electronic health records (EHRs). They claim to have coverage of 72% of prescribers through this channel.

From what I can tell, ConnectiveRx currently lacks the pharmacy enabled direct to patient communication channels of Adheris.

Other Medadvisor board members include Adheris founder Lucas Merrow and Kevin Hutchinson who was the founding CEO of Surescripts. Surescripts is another of CEO Rick Ratcliff’s former employers where he was founding COO and later CEO.

Surescripts connects prescribers to pharmacies via EHR integration to enable electronic prescriptions. Its network covers 99% of the US population according to the company’s website.

I do not believe that Surescripts currently competes with Adheris as Surescripts is focused on electronic prescriptions and does not communicate directly with patients. However, given Surescripts owns the e-prescriber space there seems little opportunity for Medadvisor to duplicate its highly margin Australian model in the US.

ConnectiveRx reportedly attracted bids of around US$1.4 billion in 2019, but owner Genstar decided not to sell at the time. Meanwhile, Surescripts is so dominant that it was sued by the US Federal Trade Commission for illegal monopolisation in 2019.

If Adheris is anywhere near as successful as Rick Ratcliff’s previous two employers then Medadvisor’s current shares offer exceptional value. It is somewhat of a boon to have both Rick Ratcliff and Kevin Hutchinson on the board of Medadvisor given their success in scaling other healthcare IT networks.

The risk is that Adheris proves to be a lower quality business than Rick Ratcliff’s prior employers. This is more of a risk to shareholders than Rick Ratcliff given he was awarded options representing 3.5% of the diluted share capital of the company during FY23 with an exercise price of 14 cents, well below the current share price.

Other Medadvisor board members and executives also received substantial option awards totalling a further 2% of the company in FY23. At least these options are partly “out of the money” with half having an exercise price of 21 cents and the other half exercisable at 35 cents.

Shareholders

Smallcap manager Perennial Value Management Limited has been aggressively buying up shares in recent months. It has increased its holding from 40 million shares in May 2022 to 82 million shares or 15% of the company as at 18 July 2023.

Other significant shareholders include private equity backed US med tech company Cotiviti with 8.1% and a representative on the board in the form of non-exec Brett Magun.

Following the Guildlink acquisition, the Guild Group (a provider of insurance and other services to the Australian pharmacy industry) has a 17.4% ownership and representative Anthony Tassone is on the board.

Listed distributor and pharmacy chain owner EBOS Group Ltd (ASX:EBO) holds 26.5 million shares or just under 5% of shares outstanding.

Valuation

Medadvisor has an undiluted market capitalisation of $115 million at the time of writing. As I mentioned previously, I think that the Australian business alone is worth $50 million which implies a valuation of $65 million for the Adheris business. At current exchange rates this is around $12 million (23%) more than what Medadvisor paid when it acquired Adheris in 2020 (US$35 million). Meanwhile, Adheris revenue has increased roughly 50% from US$35.3 million in FY21 to ~US$52 million in FY23.

Management is hoping to guide the group to profitability for the first time in FY24 and has recently taken cost cutting measures to this end. However, I am doubtful that they will succeed since Adheris benefited from high value covid related projects in H123 and it seems unlikely that these will be repeated in the coming year.

Source: Medadvisor 2022 AGM presentation

On a more positive note, there is no hint of accounting shenanigans to date. Capital expenditure is minimal with almost all software development expensed through the profit and loss statement. If and when management finally declares profitability, it is likely to be as advertised rather than the product of aggressive accounting treatment.

As Claude has previously articulated, Medadvisor has a chequered past and its US division is lower quality compared to the Australian operation. However, the transition of Adheris to a higher margin digital model combined with recent cost cutting measures lead me to think that the group may at last be approaching profitability.

On balance though, high stock based compensation and the risk of yet another capital raise currently make Medadvisor uninvestable in my view, despite a cheap valuation.

To find out the stocks we like best, join the waitlist to become a supporter, via this link.

Disclosure: neither the author of this article Matt Brazier, nor the editor Claude Walker own shares in MDR and neither will trade in those shares for at least 2 days following the publication of this article. This article is not intended to form the basis of an investment decision and is not a recommendation. Any statements that are advice under the law are general advice only. The author has not considered your investment objectives or personal situation. Any advice is authorised by Claude Walker (AR 1297632), Authorised Representative of Equity Story Pty Ltd (ABN 94 127 714 998) (AFSL 343937).