Online travel agent and hotel inventory aggregator Webjet Limited (ASX:WEB) announced bullish underlying half year results earlier today. Total transaction value (TTV) rose 25% to $2.3 billion, revenue increased 24% to $217.8 million and underlying net profit after tax before acquisition amortisation (NPATA) rose 44% to $55.1 million. Underlying earnings per share before acquisition amortisation (EPSA) rose 29% to 40.7 cents.

Statutory results were a different story, with NPATA down 34% to $20.9 million and EPSA down 41% to 15.4 cents.

Net debt excluding client funds rose 126% to $53.7 million over the period, but remains comfortable relative to group earnings.

Adjusted operating cash flow was $47.1 million, or 102% of statutory earnings before, interest, tax, depreciation and amortisation (EBITDA). Statutory operating cash flow was $4.9 million and free cash flow was -$10.4 million.

Clearly, much depends on whether statutory or underlying results give a truer reflection of the company. We will examine this question more closely later in this piece.

The board declared an increase in interim dividends to 9 cents per share, up from 8.5 cents last year.

Full year guidance was revised down from $162 million to $172 million at the time of the AGM to $147 million to $165 million. This is due to the impact of Covid-19 and management commented that were it not for the virus, it would have been upgrading guidance. It expects that Covid-19 will only have a short-term impact and we tend to agree.

Webjet can be broadly thought of as two distinct businesses, an online travel agent (B2C) and a global wholesale supplier of hotel beds to travel agents (B2B), WebBeds. Revenue and profit were both flat versus the prior corresponding period in the mature B2C division (although it was adversely impacted by a weak environment). The growth engine of the group is B2B which is now roughly twice the size of B2C in revenue and profit terms. Therefore, Webjet’s valuation is largely dictated by the value of its B2B segment. B2B also happens to be where the discrepancy between underlying and statutory profit lies.

Accounting matters

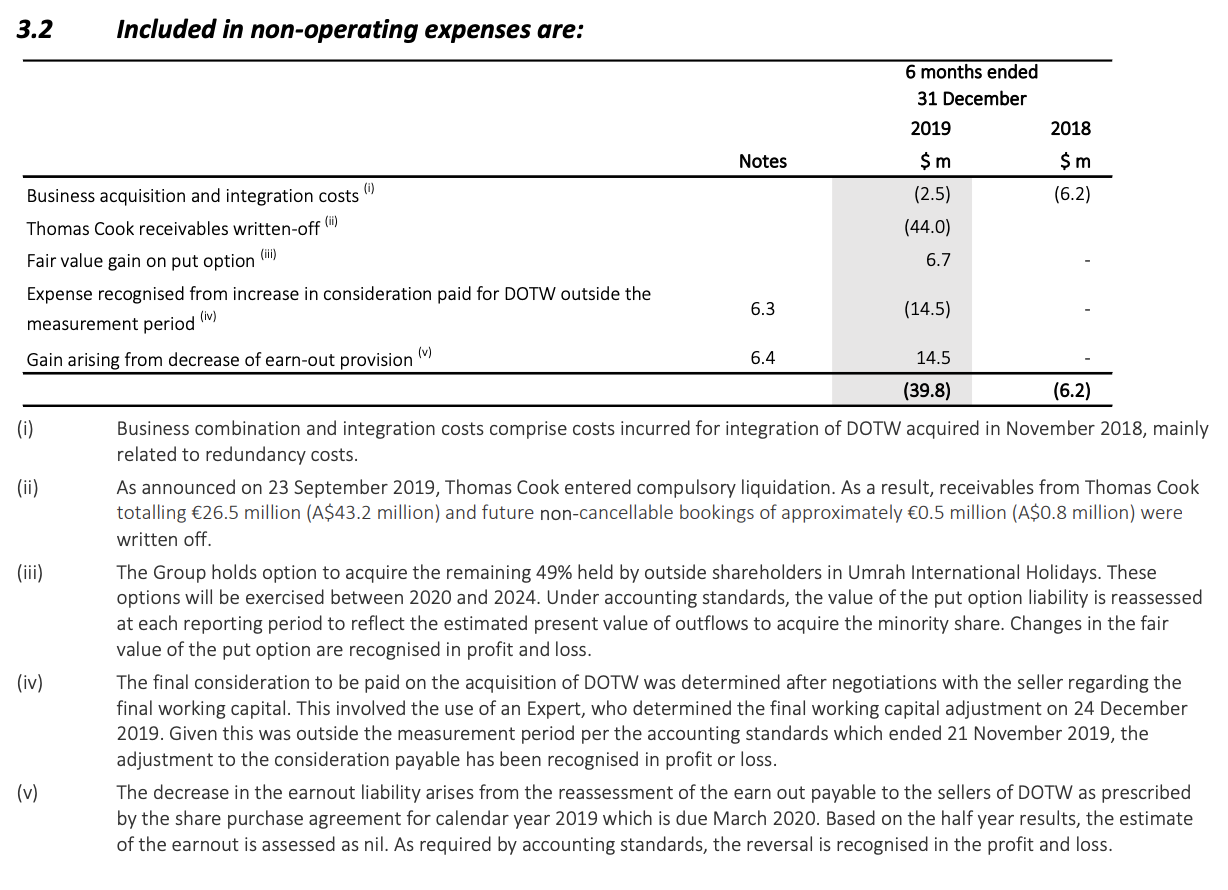

Non-operating expenses

Webjet has made a number of acquisitions to help grow WebBeds. We are leary of roll-up models in general, but are broadly supportive in this case. We believe that Webjet’s B2B business benefits from a network effect whereby more inventory leads to more customers and vice versa. Therefore, it makes sense to acquire rivals to accelerate this process (provided the price is not excessive) and ensure that other competitors don’t get too far ahead. WebBeds is now the second largest wholesaler of hotel inventory globally, somewhat justifying this strategy.

An additional scale advantage is lower costs per dollar of TTV. Webjet has seen steadily improving margins in its B2B business and expects this to continue.

However, one downside to making large acquisitions is that they make the accounts messy. For example, acquisition and integration costs can have a material impact on profit and span a couple of years for each deal. Investors need to trust that profit will recover once the acquisitions are bedded down. For a serial acquirer like Webjet, it can be many years before investors get to see a “clean” set of accounts and this half year report again contained plenty of adjustments.

It was good to see that just $2.5 million of acquisition and integration costs was charged to the income statement this half which suggests that the integration os DOTW is largely complete.

We discuss the Thomas Cook receivables write-off under the section on receivables below.

The fair value gain on put options represents a fall in the the present value of cash required to acquire the remaining 49% minority share in Umrah International Holidays, a Middle Eastern joint venture established last year. Is this because Umrah is underperforming?

According to CFO Tony Ristevski, adjustments for the consideration and earn-out payment for DOTW (both $14.5 million) offset by chance and should be considered separately.

The earnout payment relates to EBITDA targets for the combined WebBeds business for the year ending 31 December 2019 agreed with the DOTW vendors at the time of the acquisition. The $14.5 million gain in this period reflects the fact that these targets were missed.

The increase in consideration paid for DOTW relates to a discount that Webjet thought it was getting on the purchase price of DOTW due to some unrecoverable receivables.

Last year, Webjet recognised goodwill for the acquisition of DOTW on its balance sheet including a $16.7 million refund due to working capital adjustment. It turns out that Webjet will not be receiving a discount, hence the charge to the income statement this half. As it was over a year since the acquisition date by the time the matter was settled, Webjet had to incur a charge to the income statement rather than adjustment to goodwill on the balance sheet.

Receivables

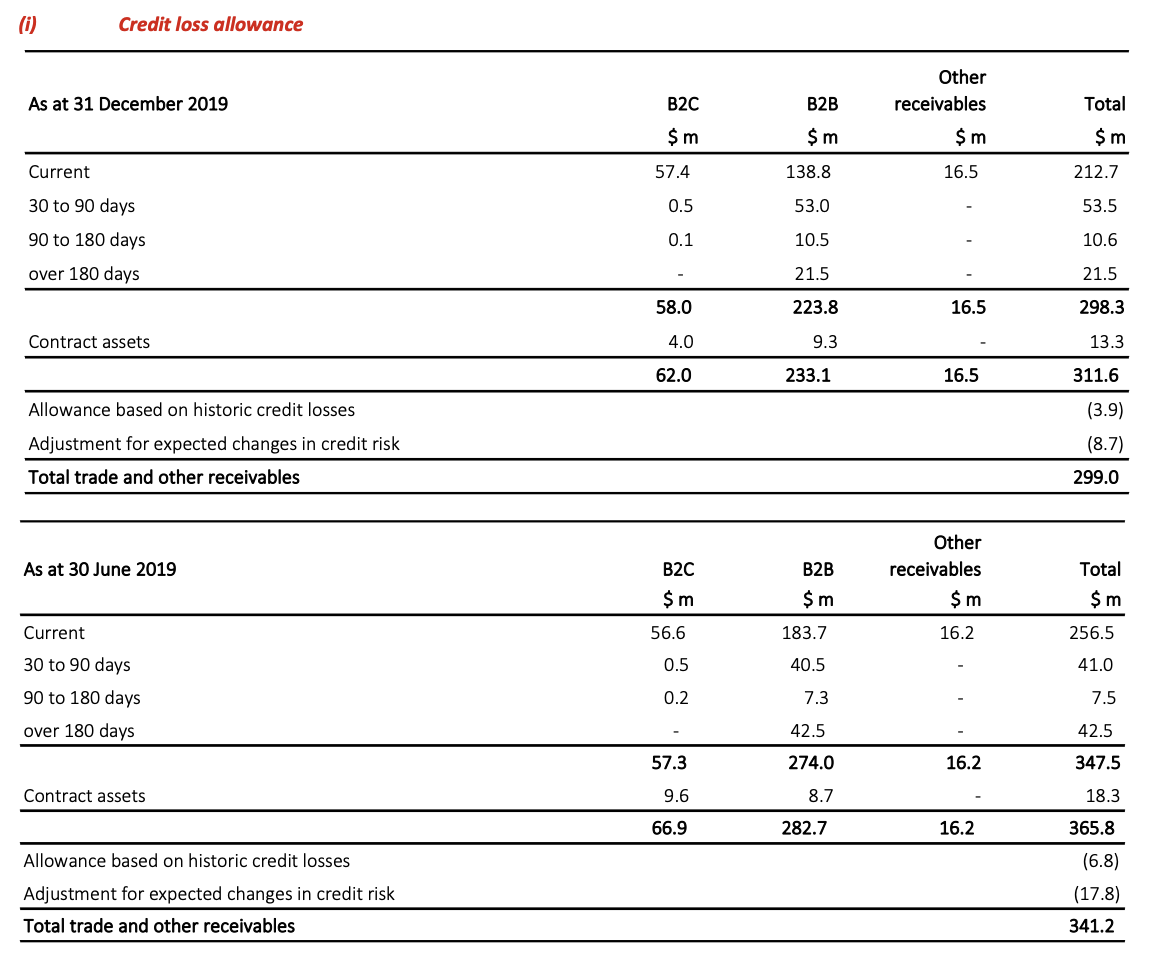

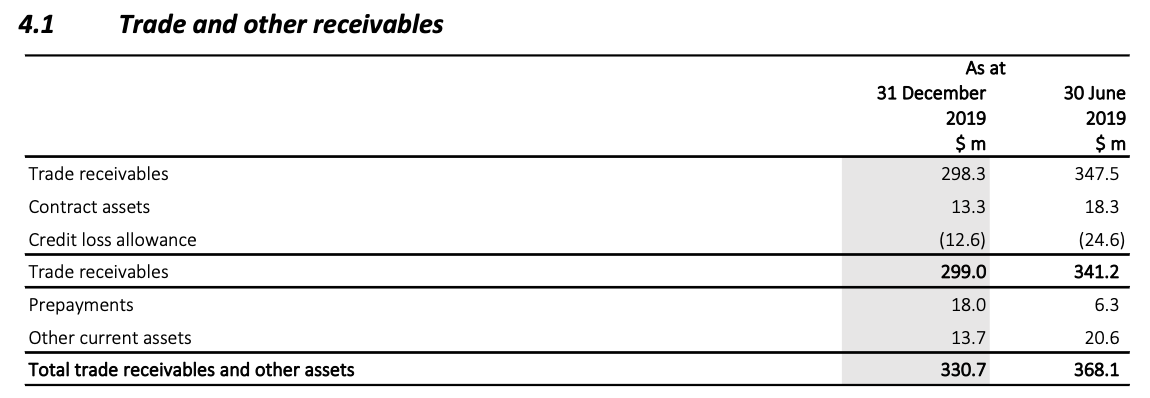

The vast majority of Webjet’s receivables relate to its B2B business as consumers typically pay Webjet in advance.

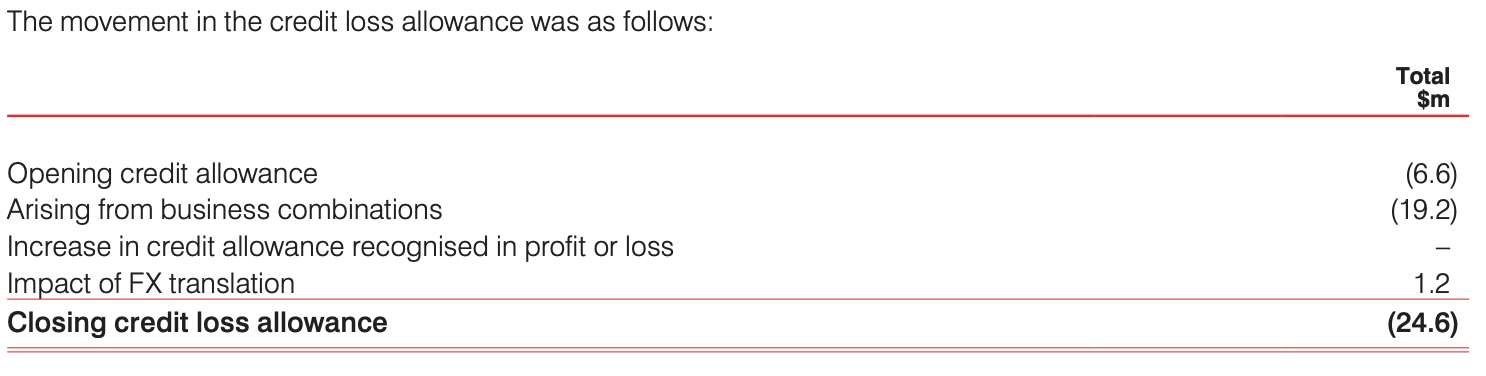

Above you can see that receivables fell from $347.5 million to $298.3 million over the period. The worrisome “over 180 days” balance almost halved to $21.5 million.

However, the situation was helped by a $12 million fall in credit loss allowance (ie write offs) and an additional $44 million write off of Thomas Cook receivables after it went into liquidation during the half (disclosed in non-operating expenses earlier).

It is also worth noting that the 30 June credit loss allowance includes $19.2 million recognised when the company acquired DOTW. As you can see above, Webjet did not book an impairment charge through the income statement last financial year.

The strength of WebBeds ultimately depends on the strength of its travel agent customers. The demise of Thomas Cook wiped out about half of Webjet’s EBITDA for the half. Most of Webjet’s B2B customers are much smaller than Thomas Cook and so customer concentration risk is low. However, the fact that such a large operator went down could be indicative of the health of the broader travel agent industry. Low customer concentration is of little help if all your customers are susceptible to common mounting pressures, the obvious one being the rise of direct booking by consumers over the internet.

In light of this, it would appear that Webjet ought to operate a fairly aggressive impairment policy and this does not seem to be the case. The current credit loss allowance looks light at 4.2% of trade receivables, down from 7.1% at 30 June and Webjet incurred no credit impairment loss last year.

Conclusion

Covid-19 is likely to be a short term negative to Webjet’s business after which B2B should resume its upward trajectory. However, it is quite possible that management has underestimated its impact in current guidance. It is simply impossible to know at this stage what the total repercussions will be.

WebBeds benefits from structural growth in the travel industry, particularly in Asia where it is the second largest operator. It is also likely to continue seeing profit margins rise as it grows due to efficiencies of scale.

The trouble with B2B is counterparty risk and whether this is being properly accounted for. Should the Thomas Cook bad debt be treated as an exceptional item or are other WebBeds’ customers likely to befall the same fate? In particular, is there a risk that some of WebBeds’ Asian customers go under due to Covid-19 which is not reflected in today’s updated guidance?

These unanswered questions lead us to think there are better places to invest, at least until the coronavirus risk subsides.

We (Claude and Matt) both sold our shares in Webjet earlier this week and do not intend to trade the stock again for at least two trading days following the publication of this article. We don’t intend this post to be advice. If in doubt, read our disclaimer.

If you’d like to receive a occasional Free email with more content like this, then sign up today!