Radiology software company Pro Medicus (ASX: PME) today released its full year results for the 2023 financial year. It reported a 33.6% increase in revenue to $124.9 million and a 36.5% increase in profit after tax, to $60.6 million. Earnings per share of 58 cents easily supports the total annual dividend of 30c cents per share.

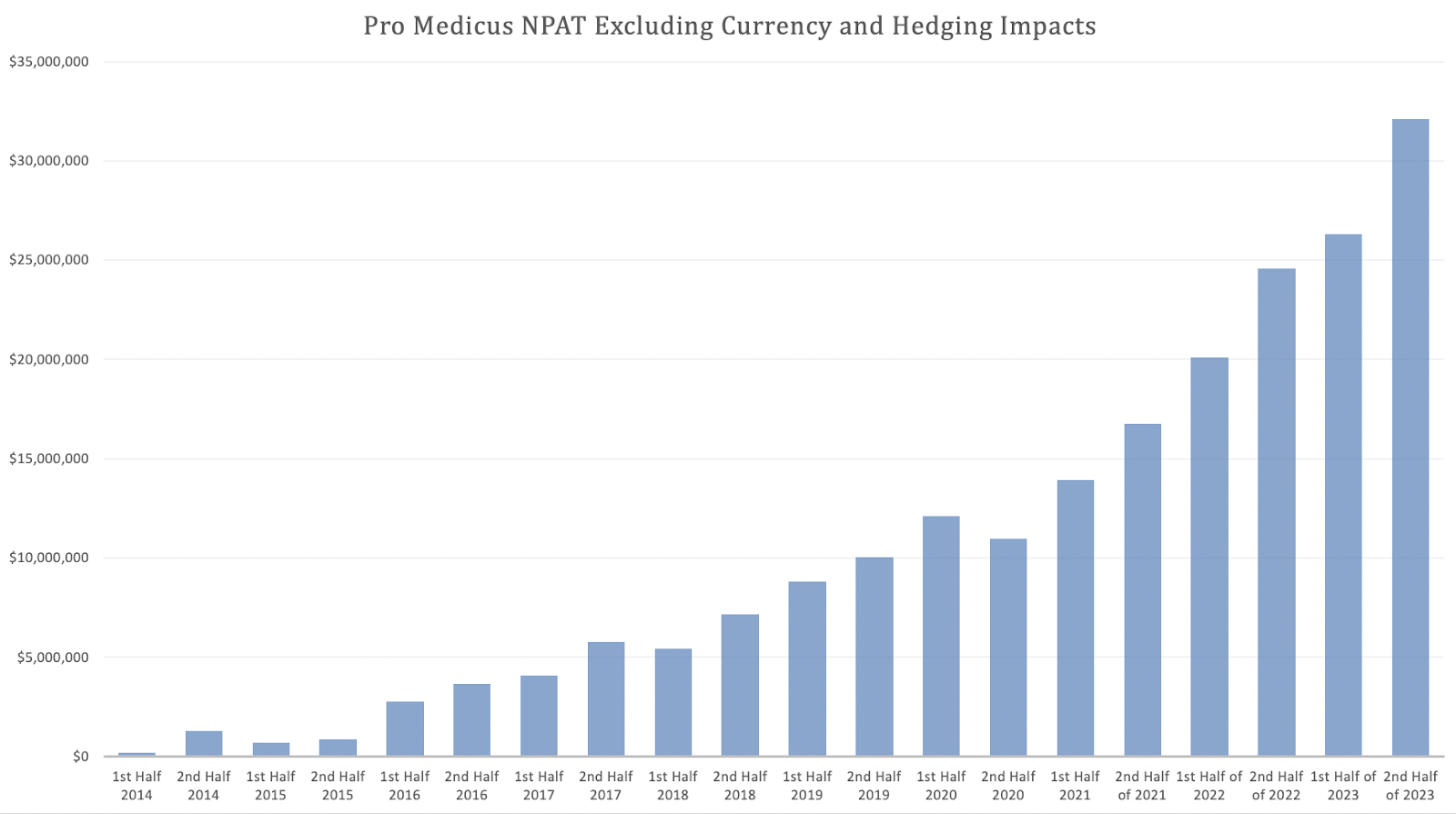

While the record Pro Medicus net profit after tax in FY 2023 did benefit from an unusually large gain on currency hedging, even removing that impact, the second half profit result showed accelerated growth. You can see the strong half on half profit growth depicted in the chart below.

Note also that Pro Medicus has benefitted from higher interest rates, because of its large cash holding. In FY 2023 Pro Medicus received over $2.4m in interest payments, compared to under $700k in FY 2022.

Pro Medicus continued its run of increasing its EBIT margins. In H1 FY 2023, it achieved an impressive 67% EBIT margin, but the H2 FY 2023 result was a new record, with an EBIT margin of 70.6%, despite increasing employee expenses faster than previously. However, once again this figure benefitted from currency and hedging gains, with the full year underlying EBIT margin of 67.2% being a better guide to margins in FY 2024 and beyond. Either way, this was a great result in terms of margins, which has been one of the major metrics on which Pro Medicus has outperformed expectations.

As you can see by revisiting our historical collection of Pro Medicus Stock Analysis, the company has continually increased EBIT margins over the last few years. Once upon a time expected EBIT margins were below 60%. The fact that EBIT margins have increased shows admirable cost control, though once again, currency and hedging impacts boosted the result in H2 FY 2023.

This cost control demonstrates the quietly confident nature of management who have resisted analyst calls to increase spending (often based on the naive assumption that increased marketing automatically increases sales, when it does not). Even now as employee expenses do increase, they are expected to do so gradually.

Pro Medicus CFO Clayton Hatch mentioned on the conference call that the company was hiring in implementation and technical roles, and this was driving employee expense growth in the vicinity of 10% – 12%. This increase is higher than in the past, but lower than revenue growth.

On that subject, Pro Medicus CEO Sam Hupert commented that “We are always refining our implementation… with the aim of doing things quicker… we have been steadily increasing those numbers to support new client implementations, so increasing headcount plus refining the process plus cloud, no hardware purchasing… mean we are actually implementing quicker than we did before… we don’t want to be in a position where you win stuff and can’t put it in…”

This focus on speed to implementation is a key “tell” of a quality software business, because the inverse – slow implementations – is often indicative of an overly complex and poorly designed software stack. Given that implementation revenue is always lower than product revenue, longer, more expensive implementations degrade the economics of a software business relative to faster, cheaper implementation. The progress the company is making on its implementation speed, is in my opinion evidence that it is improving or maintaining its competitive position.

Moving away from capital allocation skill, I also wanted to mention a key indicator of management integrity, which is their refusal to give specific guidance. This protects the company from the nearly inevitable (eventually) reputational damage that arises when a company misses guidance, so it is in the interests of long term shareholders. Furthermore, the willingness to resist the pressure of capital market analysts (who simply want to be spoon-fed their estimates, to make their own lives easier) is just one example of why I have extreme confidence in the honesty and integrity of the Pro Medicus leadership. Refusing to give specific guidance is rare, but it is almost always in the interest of long term shareholders, for whom advance notice of a specific year’s result will not be majorly important.

Would you like to access all our subscriber only coverage of results season, plus our active Buy recommendations? If so, join the waitlist today!

Pro Medicus Results Show Strong Growth In North America

Pro Medicus is a market leader in Australia with its radiology information system, but the main game has been North America, where Pro Medicus sells the Visage 7 Viewer, the Visage 7 Workflow, and Visage 7 Open Archive. While the Viewer is the star product, the latter two products produce material revenue having been developed in-house by Pro Medicus.

Below, you can see how H2 FY 2023 was another great year of revenue growth from these products (combined). The acceleration in half-on-half revenue growth rate is great to see, as usually we see growth rates drop as a company grows revenue.

Pro Medicus Free Cash Flow And Balance Sheet

I believe the best way to calculate free cash flow for Pro Medicus is to take operating cashflow and subtract payments for capitalised development costs, payments for plant and equipment and payments for lease liabilities. This ignores its investments in financial assets (designed to generate improved returns on its large cash holdings). It also ignores share buybacks, which are voluntary (and minimal, for what it’s worth).

Using that methodology, Pro Medicus generated about $55.8 million in free cash flow in FY 2023, representing 92% of NPAT. This is an incredibly good conversion of net profit to free cash flow, but would have benefitted from some degree of luck. Sometimes, Pro Medicus has had much lower conversion of NPAT to free cash flow, so it’s worth remembering that it does fluctuate a bit due to timing of payments and receipts. In any event, this year was a very strong one on that measure.

After this excellent result, Pro Medicus now has $121.5 million cash and investments on the balance sheet. It has zero debt.

Pro Medicus (ASX: PME) Growth Outlook

Recent deals with Memorial Sloan Kettering Cancer Hospital, worth $24m over 7 years and Gundersen Health System, worth $20m over 7 years mean that Pro Medicus has plenty to get started on in FY 2024. However, the key thing to remember about Pro Medicus is that most of its revenue is charged on a “per radiology study” basis. In the chart below, the pink represents the volume based revenue.

This business model means that Pro Medicus grows as long as its customers grow. While the radiology industry is only growing at a low single digit growth rate, the CEO said on the conference call that “Growth in our client base is definitely above industry average… [Visage is] an enabler, [clients] are able to open new sites and manage them through Visage, that they couldn’t before”.

On top of that, Pro Medicus can grow by selling the newer Workflow and Archive products to existing Viewer customers. Finally, Pro Medicus also receives price increases when it renews its contracts. Although no major renewals are scheduled for FY 2024, the CFO commented that there are three big ones, Mercy, Mayo and Franciscan, all due for renewal in FY 2025.

Pro Medicus is also expanding into cardiology, and launching its AI-powered breast density algorithm. It is expecting initial revenues from both these products within the next 6 months, which is very exciting, but not guaranteed. However, there may be a significant gap between initial revenues and material revenues. The CEO commented that “the first step to getting material revenue will be to get key reference sites in place.”

Pro Medicus Competitive Advantage

Although the company has dropped the language around being 18-24 months ahead of competitors, I suspect this is because that has proven to be wildly conservative, based on this recent interview with the CEO.

Notably, the CEO says that “Pretty much all the opportunities are for Cloud, with an increasing number for multiple products, including many that are looking at our “full stack” or all three products.” Furthermore, on the conference call he said “As far as we know none of the competition is full cloud capable at this point.” In saying this he was distinguishing between storing data in the cloud and having the application run in the cloud.

Finally, it’s increasingly easy to find radiologist verification that Visage 7 is the best system on the market. Below, I’ve screenshotted a few jovial comments that demonstrate the high regard in which Visage 7 is held.

Finally, the CEO commented that “The acute global shortage of radiologists keeps getting more and more acute by the day” and “Radiologists are either looking for or insisting on wfh as part of their package.”

Because Visage 7 massively facilitated flexibility for radiologists, I expect this phenomenon will also increase Pro Medicus’ competitive advantage.

Are Pro Medicus Shares Cheap?

With earnings per share of 58 cents, and a share price of $74, Pro Medicus trades on a P/E ratio of about 127. Obviously, the Pro Medicus PE ratio implies plenty of optimism about its growth prospects. For example, if it grows 20% per year for 5 years, and the share price stays the same, it would still be on a PE ratio of 51!

However, it’s worth noting here that – although I have held Pro Medicus shares continuously since the share price was 86 cents – selling some Pro Medicus shares too early, based on what I thought was an overly optimistic PE ratio has been the single stupidest financial decision I have ever made. I no longer think it is clever to take profits on this stock, just because the PE ratio is high.

Rather, I am more mindful that it is the highest quality growth business on the ASX, and has skillful, honest and competent management. As long as those conditions hold, I believe growth funds (many of which invest Australians’ superannuation) will keep allocating more and more capital to Pro Medicus, in order not to underweight the stock, relative to the index. To date, any growth funds who have been underweight Pro Medicus, have seen their performance suffer as a result. To my mind, flows into superannuation are going to be keeping the Pro Medicus PE ratio high, because there are so few genuinely high quality software businesses on the ASX.

On top of that, Pro Medicus founders Anthony Hall and Sam Hupert have shown stand-out integrity by letting the market know ahead of time their intentions to sell shares. They have sold only small parts of their holding, and together, still control the company, with over 50% of the shares on issue. If this approach remains in place, then there is likely to be relative scarcity of Pro Medicus shares, compared to other high quality software companies where the founders sell more frequently.

So while I cannot claim that I view PME shares as undervalued based on a discounted cashflow model, I am skeptical that PME shares will ever become undervalued while the current business model and leadership remain in place. And given the strong competitive positioning, high margins, and very strong growth outlook, I’m don’t think Pro Medicus shares are particularly overvalued.

For now, I will continue to happily hold Pro Medicus, which is currently over 15% of my ASX portfolio. I haven’t yet updated my target buy price, but when I do, I’ll be reserving it for A Rich Life Supporters.

The bottom line is that FY 2023 was another excellent year for Pro Medicus which produced record results and continues to strengthen its competitive position.

This is a sample of the kind of analysis we share with our subscribers. Join our waitlist today to gain access to our Supporters-Only Content.

Disclosure: the author owns shares in PME and will not trade PME shares for 2 days following this article. This article is not intended to form the basis of an investment decision. Any statements that are advice under the law are general advice only. The author has not considered your investment objectives or personal situation. Any advice is authorised by Claude Walker (AR 1297632), Authorised Representative of Equity Story Pty Ltd (ABN 94 127 714 998) (AFSL 343937).

The information contained in this report is not intended as and shall not be understood or construed as personal financial product advice. You should consider whether the advice is suitable for you and your personal circumstances. Before you make any decision about whether to acquire a certain product, you should obtain and read the relevant product disclosure statement. Nothing in this report should be understood as a solicitation or recommendation to buy or sell any financial products. A Rich Life does not warrant or represent that the information, opinions or conclusions contained in this report are accurate, reliable, complete or current. Future results may materially vary from such opinions, forecasts, projections or forward looking statements. You should be aware that any references to past performance does not indicate or guarantee future performance.