Mining software and consulting company RPM Global (ASX: RUL) recently reported its results for FY 2023, boasting a net profit after tax of $3.7 million on revenue of $97.4 million. Revenue was up about 18%, converting last year’s loss into this year’s profit. Free cash flow, defined as operating cash flow less investing cash flow and lease repayments, was about $6.4 million.

This free cash flow was all used up (and then some) in buying back shares, at an average price slightly below the current share price of $1.61. The company finished the year with slightly more cash than the prior year, $34.7 million, thanks to foreign exchange fluctuations.

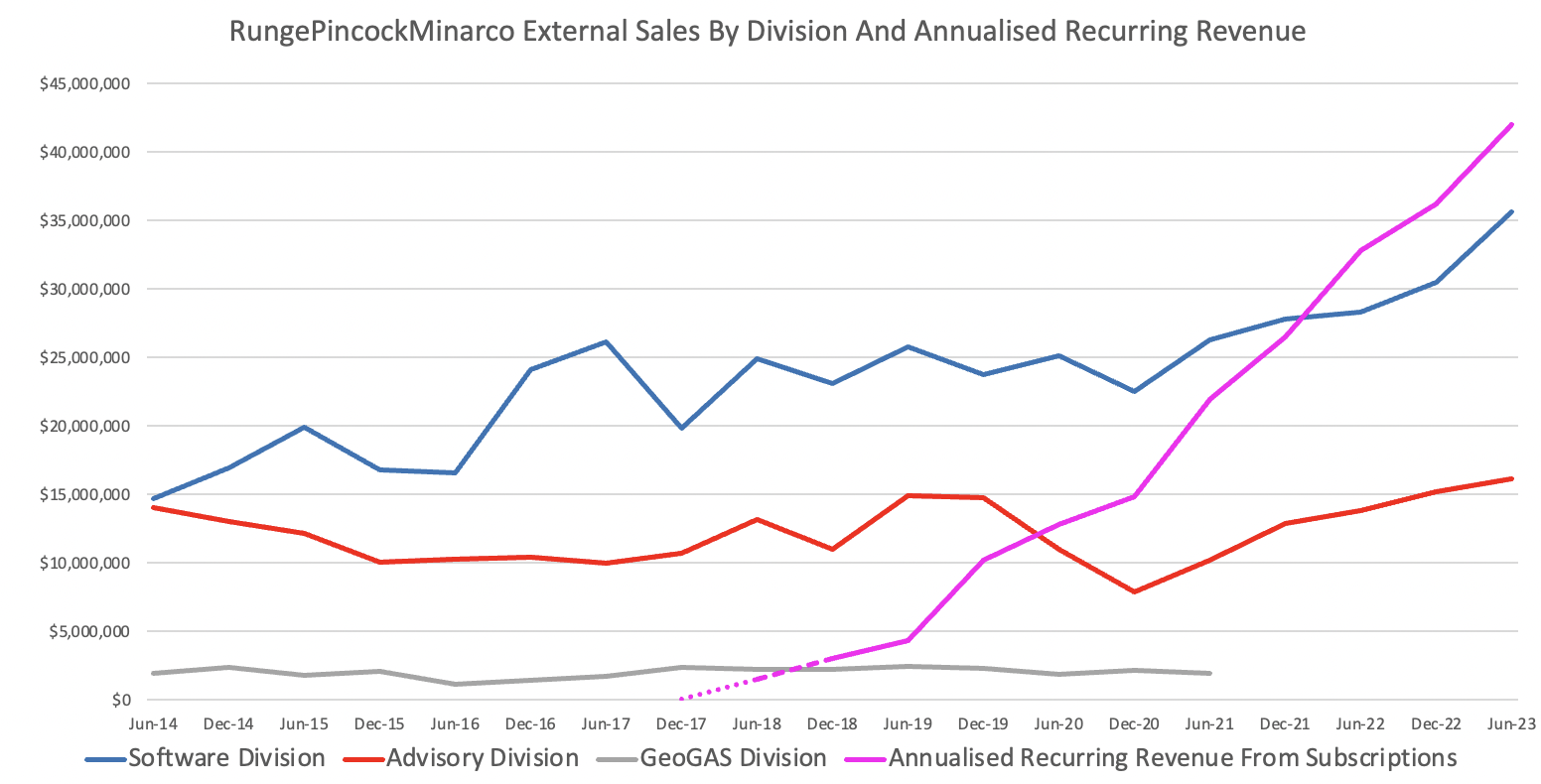

Checking in with my thesis for owning the stock, it was good to see both software sales and software subscription annualised recurring revenue (ARR) reach record levels in the second half, as you can see below. Ultimately, I think that this software subscription ARR can be very high margin revenue (say 15%+ NPAT margins). The advisory division is low margin and less reliable.

Managing Director Richard Mathews assured shareholders that “The operating leverage provided from the $132.2 million in pre contracted software revenue will support EBITDA growth in FY24.”

Furthermore, he said “In each of the last five years the company has set new software sales records and we expect to do so again in FY24. AMT, XECUTE and ShiftManager are all expected to perform strongly in the year ahead.” This bodes well for the software business.

Probably the most encouraging comment he made was that:

“AMT (the company’s asset maintenance solution) is poised to become the mining industries [sic] de facto standard for mobile mining equipment maintenance for the Tier 1 and 2 miners and mining OEM’s.” Dominating any niche in software is great for profits, but also important for providing a beachhead for the cross-sale of further products in the product suite.

However, I am less optimistic about the consulting business. The Managing Director Richard Mathews said the:

“softening of readily traded commodities like iron ore against an inflationary backdrop, has seen Tier 1 miners introduce different forms of travel, third-party services and recruitment bans to help manage their financial margins. Some have gone as far as completing a number of rounds of restructuring thereby releasing professional talent into the market which we have been able to employ. RPM’s advisory work is not expected to be materially impacted by this approach as we tend to do less work for the Tier 1’s as they typically have their own inhouse teams.“

I definitely don’t think the softening in the mining industry bodes well for the consulting division, though the company is continuing to grow both its engineering and ESG consulting businesses. While the outlook for the next 6 months is strong, I believe there is a real risk that the consulting business could move backwards in future periods. Nervousness about this segment is my number one concern about the stock, longer term.

Looking at profitability, it was good to see half-yearly net profit before tax reach a record level for recent years, as shown on the chart below.

That said, based on its earnings per share of 1.6 cents in FY 2023, RPM Global has a P/E ratio of about 100, so shareholders really need the statutory earnings per share to grow, in order to justify the current price.

Confusingly, the company is really emphasising its “underlying ebitda before management incentives” and “profit before tax before management incentives.” This makes me reflect on the personalities of the top managers. Management incentives occurred in both FY 2022 and FY 2023, and – if goals are achieved – would also occur in FY 2024.

Because management incentives are not really one-off in nature, and can occur every year, I don’t understand how it helps shareholders to exclude management incentives when reporting earnings.

Overall, it seems to me that advertising a profit before management incentives invites potential acquirers to think what they could earn if they replaced management with less “incentivised” personnel. Therefore, this makes me wonder whether directors are interested in some kind of takeover offer, in due course.

On the other hand, it is possible that management are merely looking to attract shareholders with such high suggestibility that they think profits before management incentives are a good way to value the business. I have my doubts about whether that will work, but I’ve certainly seen crazier things on the stock market, and this is certainly an innovative approach to shareholder communication.

Either way, my view is that in order to succeed as an investment RPM Global will need to continue to grow revenues and genuine net profit after tax.

The good news is that profit growth is forecast, with the company giving guidance for profit before tax before management incentives of $12.5 million to $14.0 million in FY 2024. Your guess is as good as mine what this means in genuine profit after tax. For example in FY 2023, RPM Global made $9.2m before tax before management incentives and actual net profit before tax was about $4.8m which was whittled down to $3.46 million after tax, foreign exchange impacts and (quirkily) the increasing obligation of a defined benefit scheme.

Still, guidance suggests the genuine profit after tax will grow in FY 2024, but it’s not clear how much it will grow by. The biggest swing factor will be how much (if any) of the additional profit is automatically paid to management to keep them nice and incentivised! The only estimate in S&P Capital IQ from Moelis suggests NPAT of $8.2 million, on $16.6m EBITDA (after management incentives, presumably.)

To be conservative, I’d estimate a NPAT of around $5m to $7m. That’s still good growth and at the midpoint would put the company on about 61x earnings; still expensive but within the realms of reason. Nonetheless it’s worth noting that I’m a bit less bullish than Moelis, in the short term.

Looking to the top line, revenue is expected to grow between 6.7% and 11.7% to $105m – $110m. That seems pretty modest to me, but I imagine that the advisory business is quite hard to forecast, so the actual result could easily come in either above or below that number.

At the current share price of $1.60, RPM Global trades on about 8.7 times its high quality recurring subscription software revenue (being $42m). As a reminder, that number is sure to grow as it transitions license + maintenance fee contracts over to pure subscription. If we include the maintenance revenue, annualised recurring revenue is about $55m. You could argue that RPM Global is on around 5 – 6 times the annualised software subscription revenue it can reasonably expect to achieve in the next couple of years. Personally, I’d happily bet this figure keeps going up for a good long while, though the speed of growth is debatable.

When it comes down to it, we have a profitable, cashflow positive business, with aligned and… er… heavily incentivised… management that is growing its ARR nicely, selling sticky, mostly mission critical software. At a market capitalisation of $366m it has the potential to one day get into the ASX 200, which in turn has the potential to attract price insensitive forced buyers (passive funds and closet indexers).

It’s hard to get much of a sense of management given they don’t do shareholder calls after results, preferring instead to hold private meetings (I assume; I haven’t been offered one).

I do wonder whether better informed fund managers would figure out any issues before me, due to having better access to management. Of course that could also happen because they are smarter than I.

On the upside, I always find the written management commentary to be informative and useful and it is good to see the company returning excess capital to shareholders via the share buy back. That should boost earnings per share slightly over the long term.

Notwithstanding a couple of reservations, RPM Global ticks most of the boxes for me. It is not my highest conviction long-term investment, but I’m happy to have the stock in my portfolio and I still consider it undervalued at current prices.

If you would like to be among the first to receive articles like these, and even suggest small-cap mailbag articles yourself, then you can click here to join the waitlist to become a Supporter.

Disclosure: the author of this article owns shares in RUL and will not trade them for 2 days following this article. This article is not intended to form the basis of an investment decision. Any statements that are advice under the law are general advice only. The author has not considered your investment objectives or personal situation. Any advice is authorised by Claude Walker (AR 1297632), Authorised Representative of Equity Story Pty Ltd (ABN 94 127 714 998) (AFSL 343937).

The information contained in this report is not intended as and shall not be understood or construed as personal financial product advice. You should consider whether the advice is suitable for you and your personal circumstances. Before you make any decision about whether to acquire a certain product, you should obtain and read the relevant product disclosure statement. Nothing in this report should be understood as a solicitation or recommendation to buy or sell any financial products. A Rich Life does not warrant or represent that the information, opinions or conclusions contained in this report are accurate, reliable, complete or current. Future results may materially vary from such opinions, forecasts, projections or forward looking statements. You should be aware that any references to past performance does not indicate or guarantee future performance.