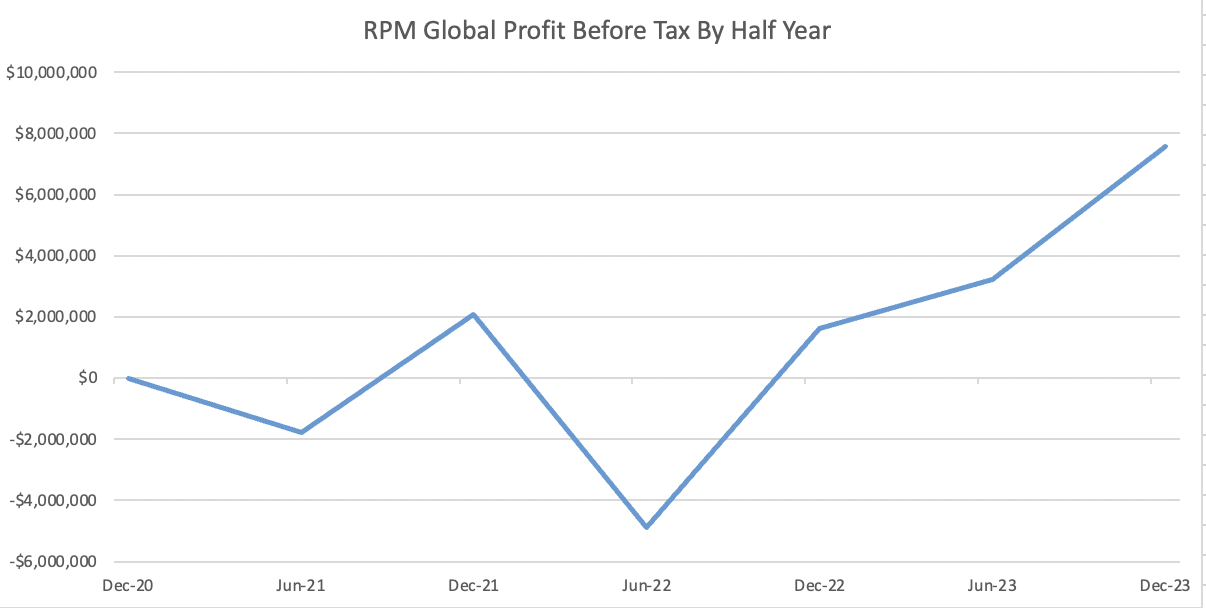

Late last week, mining software and consulting company RPM Global (ASX: RUL) reported its H1 FY 2024 results, boasting revenue up 20.7% to $56.2m and net profit before tax up from $1.6m in the first half last year to $7.55m.

Due to prior year tax losses, net profit after tax came in at $6.84m. RPM Global “still has $43.7 million of tax losses carried forward in Australia,” so we can expect a fairly low tax rate for quite a few years, yet.

Nonetheless, profit before tax is probably a better measure of underlying performance. Happily, the H1 FY 2024 result saw strong improvement, supporting the thesis that RPM Global will benefit from operating leverage from here as its revenue grows.

Notably, the profit before tax result benefitted from a one-off $3.1m payment because a customer was acquired and bought back a royalty stream. If we back out this $3.1m payment, then net profit before tax would have been about $4.45m. That’s not as impressive as the statutory figure, but still implies very strong growth both on the prior corresponding period, and 39% growth on the immediately preceding half.

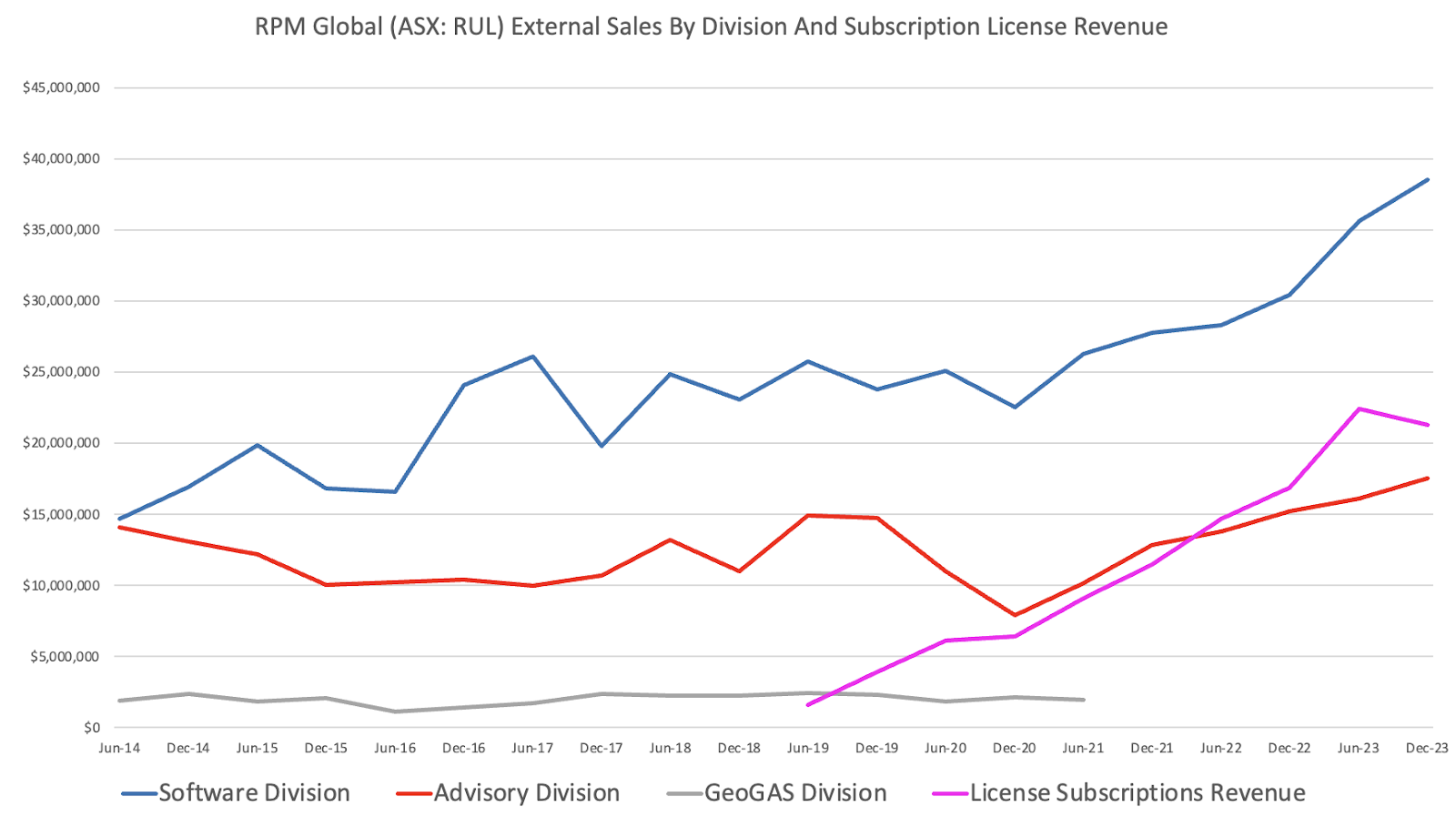

However, the story was not quite so rosy when it came to subscription revenue.

As you can see below, revenue from license subscription revenue was actually down versus H2 FY 2023. This was due to the fact that $2.4m of revenue had been pulled forward from FY 2024 to FY 2023 when a (separate) customer ended their contract early (paying out the remainder).

Notably, RPM Global (ASX: RUL) did not mention this pull-forward of revenue in its FY 2023 results, when it made subscription revenue look better than it otherwise would have been. For this reason, despite the strong performance of the company, I still have relatively low trust in management compared to other companies I own. As a result, I would be less likely to tolerate poor performance from RPM Global than other holdings.

If we do adjust for the $2.4m pulled forward (and assume it would have been spread evenly over FY 2024), then subscription revenue is still on a nice positive trajectory. Despite losing this contract, the company says that, “Year-to-Date ARR churn has remained steady at 3%.”

RPM Global actually held a conference call for the first time after these results, and CEO Richard Mathews did admit that it was a mistake not to call out the $2.4m pulled forward when the company reported the FY 2023 results. That’s a real positive, but you really have to wonder about the thought process that leads to a company deciding not to report that one-off benefit in FY 2023 when they know it is going to negatively impact the growth rate when it does not recur in H1 FY 2024.

Are there other one-off benefits that they have not disclosed in the H1 FY 2024 results?

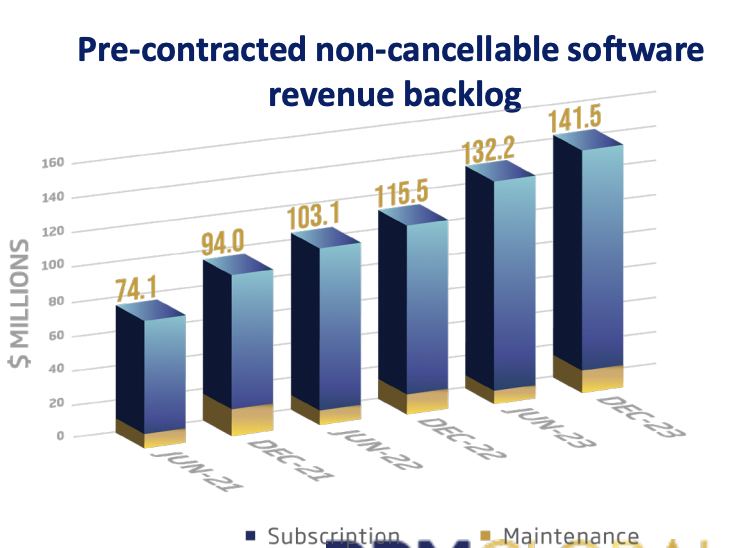

Besides the fall in subscription revenue, the worst aspect of this report was that the half-on-half growth in the revenue backlock declined.

As you can see below, RPM Global added only $9.3m worth of non-cancellable software revenue backlog in H1 FY 2024, compared to $16.7m added in H2 FY 2023, and $12.4m added in H1 FY 2023.

RPM Global Cashflow and Balance Sheet

RPM Global typically has much weaker cashflow in the first half, compared to the first half. This is because “Most of the software maintenance support revenue is invoiced at the start of the calendar year and paid in the second half of the company’s financial year,” and because “Short-term incentives are accrued in 2H but are paid out in 1H of the following financial year”.

As a result of these factors, free cashflow was negative $7.4m, calculated by subtracting investments in PPE, investments in intangibles, and lease repayments from the operating cash out flow of about $5.5m. This excludes the $3.1m received for the royalty stream.

Despite this significant cash burn, the company still had $23.3 million in cash and no debt at the end of the period.

RPM Global Guidance & Valuation

As usual, RPM Global gave unhelpful guidance that excludes unspecified management incentives. This unhelpful guidance is for Profit Before Tax excluding management incentives is projected to be in the range of $16.5 million to $18.0 million.

I have no idea what this means for actual real profit after management have been paid, but given the first half PBT result (excluding management incentives) was around $7.55m we can conclude that (excluding management incentives) the second half should be at least 18% better than the first.

Allowing for a little bit of management incentive (at the very least) this could mean that the company earns ~3.2 cents per share in the second half, up on ~2.8 cents in the first half, for a total of ~6 cents per share for the full year. On the conference call, the CEO drew attention to the fact that because the company is buying back shares, earnings per share are growing faster than profit. My forecast assumes the company continues to buy back shares, though this is obviously not guaranteed.

If that were to be achieved, RPM Global would be on trailing P/E ratio of about 30 at the current share price of $1.80. Revenue grew at 20% in H1, and operating leverage means profit should grow faster than revenue. Even if profit only grows at 25%, 15% and 10% over the 2025 – 2027 period, that would put the company on a P/E ratio of less than 19.

While I would never expect RPM Global to fetch as high a multiple as a pure software company (given its significant advisory business), I do think that it would trade on a P/E multiple of more than 19.

More importantly, if you take a long-term view, there is clearly potential for a re-rate as RPM Global grows in size.

Typically, once a software company graduates into the ASX 200, it achieves a much higher multiple. For example, Xero trades on 166 times earnings, Pro Medicus trades on 123 times earnings, Altium trades on 75 times earnings, and Technology One trades on 52 times earnings.

I am not saying that RPM Global should ever trade on these multiples, but I am suggesting there is plenty of evidence that once software businesses make it into the ASX, they do benefit from higher multiples as the pool of potential buyers expands.

Due to the prospect of continued earnings growth and more interest in the stock as it gets closer to the ASX 200, I continue to believe RPM Global presents an attractive opportunity at the current price despite its drawbacks. I will continue to hold my shares and consider them attractive at current prices.

Disclosure: the author owns shares in RUL and will not trade RUL shares for 2 days following this article. This article is not intended to form the basis of an investment decision. Any statements that are advice under the law are general advice only. The author has not considered your investment objectives or personal situation. Any advice is authorised by Claude Walker (AR 1297632), Authorised Representative of Equity Story Pty Ltd (ABN 94 127 714 998) (AFSL 343937).