Sonic Healthcare Ltd (ASX:SHL) announced its full year results for FY23 yesterday. The market reacted adversely with the share price falling 5.7% to $32.03 on the day.

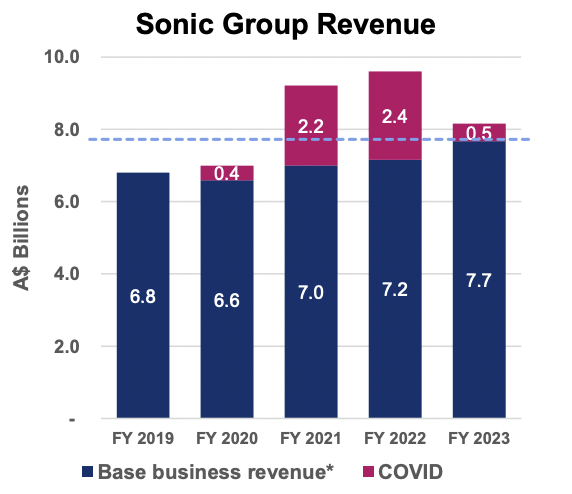

Sonic Healthcare revenue reduced 13% to $8.2 billion as covid related testing revenues tumbled 80% from $2.4 billion to $485 million. Revenue excluding covid testing (base business revenue) improved 11% to $7.7 billion.

Constant currency organic base business revenue increased 7% compared to FY22 with an acceleration in the second half of the year (6% in H1, 9% in H2). Organic growth has continued into the new financial year with July up 8% indicating the underlying business is in rude health.

Source: Sonic FY23 presentation

Sonic Healthcare EBITDA reduced by 40% to $1.7 billion due to the fall in higher margin covid related revenue and NPAT fell 53% to $685 million. Similarly, Sonic Healthcare basic EPS fell 52% to 145.8 cents.

Legacy covid related labour and infrastructure costs particularly impacted profit margins in the second half of FY23, but this effect ought to unwind going forward. Sonic Healthcare EBITDA margin was 22.5% in H1 versus 19.3% in H2.

Management guided for EBITDA in the range of $1.7 billion and $1.8 billion in FY24. This implies growth of 5% at the midpoint as a further reduction in covid related sales is expected to partially offset progress in base business.

Any growth will likely be wiped out at the NPAT level as a 25% higher interest charge is expected in FY24 due to higher rates along with an increase in the effective tax rate.

Sign Up To Our Free Newsletter

Both Sonic Healthcare FY23 EPS and profit guidance for next year were just over 5% below consensus analyst expectations going into the result which likely explains the fall in the Sonic Healthcare share price on the day.

However, management pointed to renewed growth in FY25 as acquisition synergies are realised, efficiency programs are implemented and regulated price rises come into effect.

Turning to the balance sheet and net interest bearing debt increased $74 million to $886 million, a modest rise considering currency movements contributed $43 million. This debt load is more than comfortable as it represents just 0.6 times EBITDA.

Operating cash flow prior to interest and tax was strong at 110% of EBITDA as receivables moderated on the back of lower revenue.

Capex including lease capital repayments was $868 million which exceeded depreciation of $631 million during the year. This represents a sizeable increase in investment compared to prior years and mirrors management commentary around investment in automation and rationalisation of lab infrastructure.

Business segments

Sonic is primarily a global provider of pathology services, but it also runs a sizeable Australian radiology group. In addition, it operates some medical centres and other miscellaneous business lines representing 5% of the group.

Source: Sonic Health FY23 presentation

The US business saw 4% base business organic growth in FY23. Management says that it has implemented an “enhanced revenue collection system” at a pilot site with a national rollout expected in FY24 to deliver “material upside potential into future years”.

Australian pathology grew 11% in organic base business terms and management called out an increase in genetic testing as one of the drivers. This possibly hints at the emergence of a tailwind in the form of precision medicine, but more on that later.

Germany experienced organic base business revenue of 10% driven by anatomical pathology, molecular and genetic testing. In case you were wondering, anatomical pathology is “the processing, examination, and diagnosis of surgical specimens in hospital and public mortuaries” according to the NHS.

There were two German acquisitions in the second half of the year expected to deliver around $200 million in incremental revenue.

The UK saw 6% base business organic growth with progress made in winning NHS laboratory outsourcing contracts.

Switzerland recorded organic base business growth of just 1% which was a creditable performance given fee cuts impacted revenue by 7%. Once again, volume growth was the result of anatomical pathology and genetic testing demand. The group acquired Swiss based Synlab Suisse at the end of the year which is expected to contribute $175 million in revenue.

Australian radiology enjoyed organic revenue growth of 11% along with margin expansion of 150 basis points to deliver a 20% improvement in EBITDA.

Elephantine opportunities

Sonic boasts almost 30 years of uninterrupted dividend increases, all of which have been overseen by CEO Dr Colin Goldschmidt and CFO Christopher Wilks. This combination of impressive shareholder value creation and longevity of executive tenure is almost unheard of and speaks to the business resilience, relentless execution and an extremely long-term mindset.

Source: Sonic Health FY23 presentation

The management duo talk of a “relentless” focus on culture which has enabled them to attract the top pathologists which in turn provides a competitive advantage when tendering for specialist and hospital based business. It is claimed that “The Sonic Difference” enables the group to win market share year after year

The slightly flattening incline of the above chart is a sign of moderating shareholder returns in recent years perhaps due to Sonic’s size. As UK smallcap investor, Jim Slater once said “Elephants can’t gallop” and these days Sonic has an elephant-sized market value of around $15 billion.

However, the dawn of precision medicine may be a reason to think that this tusker could break out into a gentle canter.

According to the FDA,

“Precision medicine, sometimes known as “personalized medicine” is an innovative approach to tailoring disease prevention and treatment that takes into account differences in people’s genes, environments, and lifestyles.”

This means that increasingly, new drugs are launched alongside a so-called “companion diagnostic” to identify the subset of patients who will benefit from the therapy. This contrasts with the traditional “one size fits all” approach within the pharma industry.

It is easy to see how Sonic Healthcare should benefit from this fundamental change in healthcare. There will be secular growth in the number and variety of tests carried out in order to correctly match patients to the right drugs. Rather than just testing for the presence of a specific disease as in the past, it will be necessary to conduct additional genetic and biomarker tests to identify which drug a specific patient is likely to best respond to.

If we do see accelerated growth in test volumes (and growth in anatomical pathology and molecular and genetic testing in FY23 points to this outcome) then this could drive higher profit margins for Sonic. Group profitability certainly benefited as a result of high throughput from covid testing during the pandemic and perhaps the same could be true in this case.

On the other hand, I imagine that it is fairly simple to ramp up volumes of a single blood test whereas it might be more complex to do so with a broad range of diverse tests required by precision medicine. This could undermine any potential economies of scale and hence margin expansion. Still, a sustained acceleration of revenue is possibly on the cards, even if margins do not improve.

Automation is perhaps another trend which plays into Sonic’s hands. In theory, scale operators such as Sonic should benefit most given superior access to capital and high testing volume throughput.

Indeed, management called out this opportunity in the FY23 release:

“Sonic expects that the use of artificial intelligence in pathology and radiology will cause step-changes in efficiency, quality, and capacity in coming years, and we are investing in IT and infrastructure, including for digital pathology, to unlock these material upsides.”

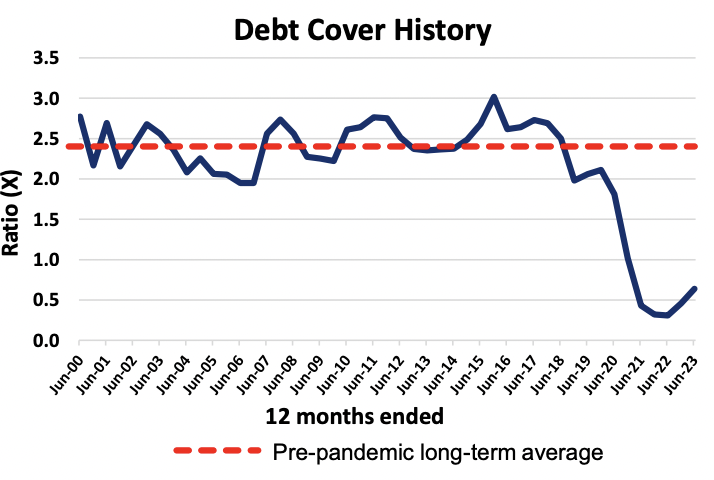

A third reason for investor optimism is that the supernormal profits Sonic generated during the pandemic have left it with an almost pristine balance sheet, with far more borrowing capacity available than on average historically. Management has indicated its intention to ramp up acquisition activity in the nearterm and put this excess capital to work.

Source: Sonic FY23 presentation (Debt Cover = Net Debt/EBITDA)

We are already starting to see this with the three European acquisitions in the second half of FY23 for a total enterprise value of $890 million.

Baseline consideration

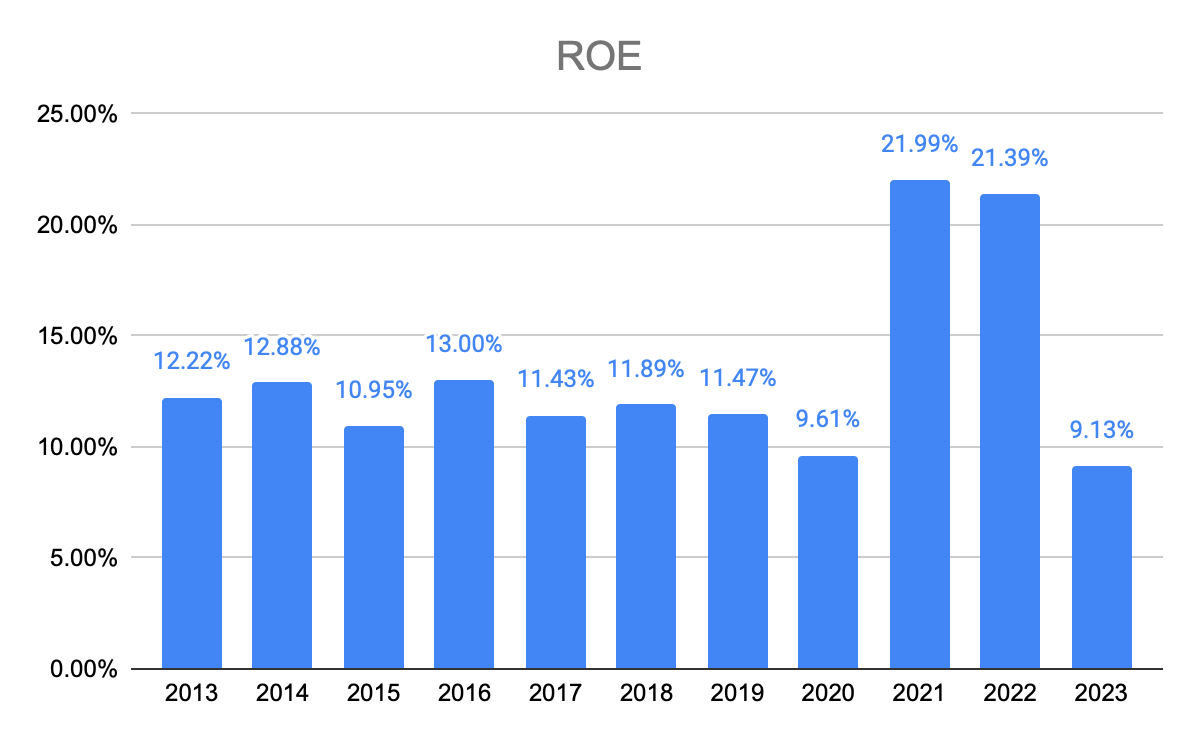

The extent to which the above factors will drive improved returns needs to be set in the context of the historical performance of the company. As we can see in the below chart, return on equity hovered around 11% over several years prior to covid. I think this is an appropriate baseline for expected returns post covid and is roughly in line with the compound annual average total shareholder return over the past decade of 10.8%.

Looking ahead, perhaps shareholder returns in the low teens is a reasonable expectation after we sprinkle in the effect of the emerging tailwinds detailed above. In the event that Sonic does not see any benefit from these trends, shareholders can expect to enjoy a continuation of low risk low double digit or high single digit returns. This is a palatable downside scenario.

I think that the market reaction to yesterday’s earnings release reflects short-term factors only rather than being a judgement on the long-term health of the business. Sonic is delivering underlying organic growth in the mid to high single digits and elevated levels of internal investment portend to improving margins going forward. Furthermore, the valuation isn’t overly demanding for a highly defensive market leader with the Sonic Healthcare PE ratio of 22 and its dividend yield of 3.2%.

There are likely to be higher returns available for those comfortable moving along the risk curve, but in my view Sonic is a good option for a cornerstone position in a conservative portfolio.

Would you like to see behind the paywall? Click here to join the waitlist to become a Supporter of A Rich Life.

Disclosure: neither the author of this article Matt Brazier, nor the editor Claude Walker own shares in SHL and neither will trade in those shares for at least 2 days following the publication of this article. This article is not intended to form the basis of an investment decision and is not a recommendation. Any statements that are advice under the law are general advice only. The author has not considered your investment objectives or personal situation. Any advice is authorised by Claude Walker (AR 1297632), Authorised Representative of Equity Story Pty Ltd (ABN 94 127 714 998) (AFSL 343937).

The information contained in this report is not intended as and shall not be understood or construed as personal financial product advice. You should consider whether the advice is suitable for you and your personal circumstances. Before you make any decision about whether to acquire a certain product, you should obtain and read the relevant product disclosure statement. Nothing in this report should be understood as a solicitation or recommendation to buy or sell any financial products. A Rich Life does not warrant or represent that the information, opinions or conclusions contained in this report are accurate, reliable, complete or current. Future results may materially vary from such opinions, forecasts, projections or forward looking statements. You should be aware that any references to past performance does not indicate or guarantee future performance.