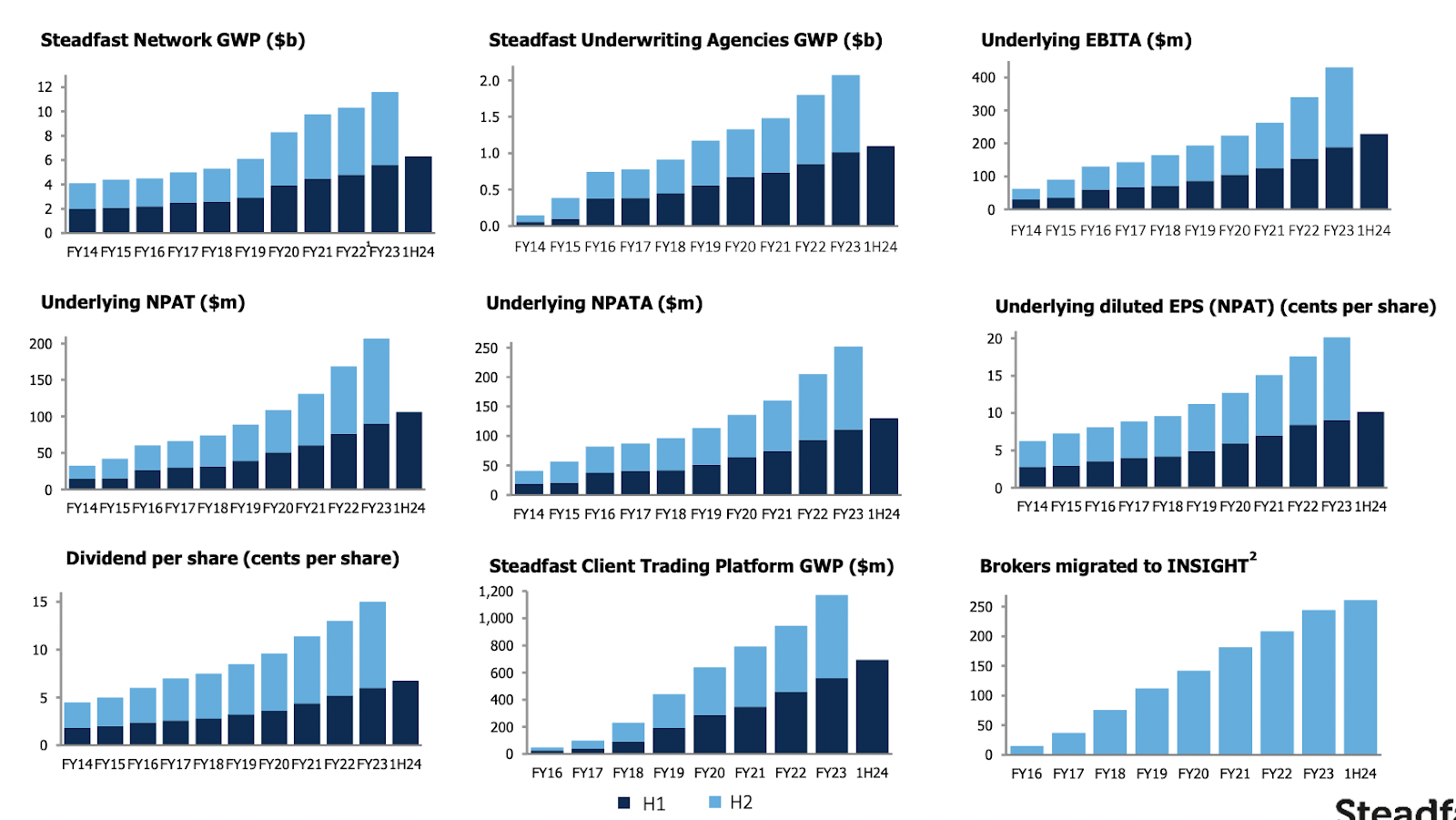

Steadfast Group Ltd (ASX:SDF) reported a typically robust set of results in February. Underlying revenue grew 19.3% to $790.4 million, underlying EBITA rose 21.4% to $229 million and underlying NPAT increased 17.5% to $106 million.

Steadfast’s share price dipped slightly upon the release, but has since recovered some ground. Some of the key metrics I consider are shown below.

Underlying NPATA, which adjusts for amortisation related to acquisitions, improved 16.9% to $130 million. This is my preferred profitability metric for this business because it most closely represents cash profits.

There was some share dilution during the period related to the acquisition of underwriter, Sure Insurance, and to provide additional capital for further deals. All in all, the share count rose by 6.5%.

This follows a placement upon release of the FY2022 results to fund the acquisition of broker, Insurance Brands Australia (IBA), which caused a 4.7% increase in share count at the time.

A combination of the two capital raising exercises over the past 18 months explains why EPS rose less than profit. EPS was up 12.2% to 10.2 cents and up 11.7% to 12.5 cents on an NPATA basis while dividends rose 12.5% to 6.75 cents.

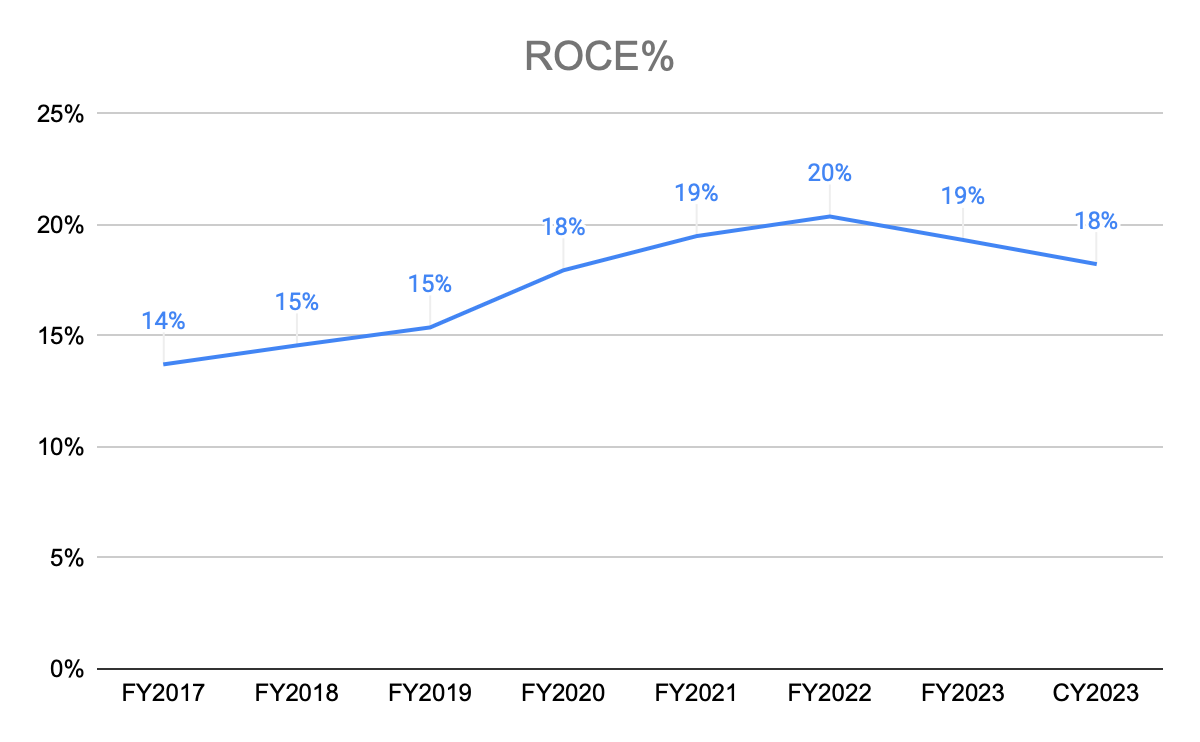

ROCE dipped to 18.2% for the 2023 calendar year, but this is to be expected given the major acquisitions completed over the past couple of years. The timing of large capital outlays can temporarily distort annual measures such as ROCE and EPS and I suspect this is the case here.

Regardless, 18% remains a very healthy level and points to continued disciplined capital allocation. Disciplined capital allocation is particularly important with acquisitive groups like Steadfast because they tend to allocate large amounts of capital rather it to shareholders (though Steadfast does have a trailing yield of 2.7%).

Management took the opportunity to reiterate FY2024 guidance which was upgraded in November at the time of the Sure Insurance acquisition. For the full year, Steadfast expects to grow underlying EPS (NPAT) by 11% to 16% and underlying NPATA is expected to be between $290 million and $300 million.

The balance sheet remains conservatively geared. At 31 December 2023, net debt inclusive of deferred consideration was $426.2 million, roughly 0.8 times the midpoint of EBITA guidance for FY24 of between $520 million and $530 million..

An attractive feature of Steadfast’s business model is that significant cash is held on trust for which it earns interest. This offsets the cost of corporate borrowing and protects the group against interest rate risk. At 30 December cash held on trust was $975 million, more than double net debt.

Cash flow was strong with pre-tax cash flow from operations of $213.7 million compared to $194.9 million in the first half of last year.

Generally speaking, Steadfast has low capital expenditure requirements and spend in this area totalled $3.5 million during the period.

In the calendar year 2023, post-tax cash flow from operating activities of $281.4 million exceeded underlying NPATA of $271 million highlighting the cash generative nature of the business

Sure Insurance acquisition

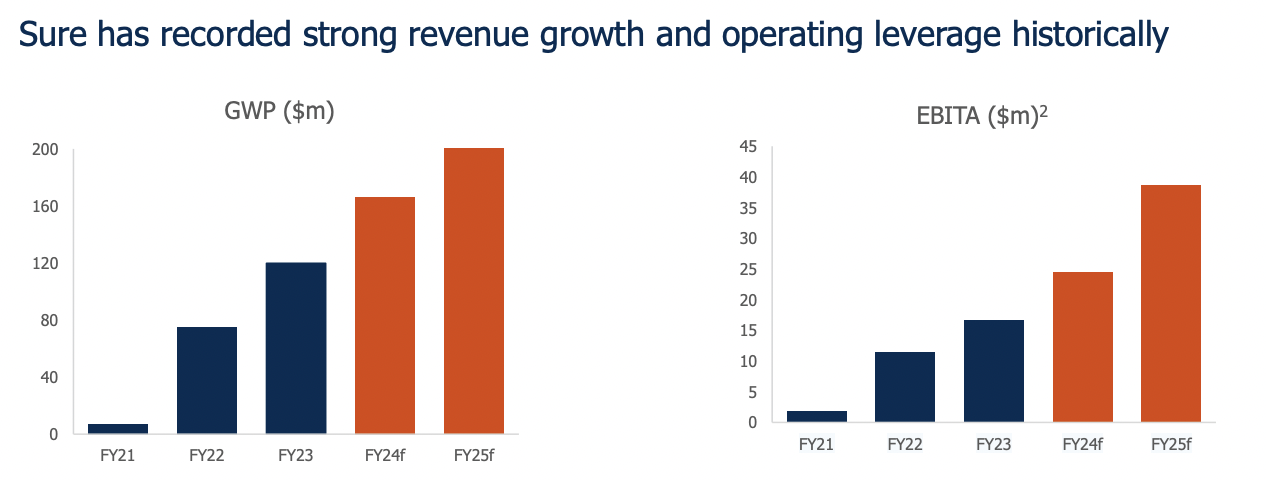

During the period, Steadfast acquired 70% of Queensland based underwriting agency Sure Insurance for $148.8 million upfront, plus earnouts depending on EBITA performance in FY24 and FY25.

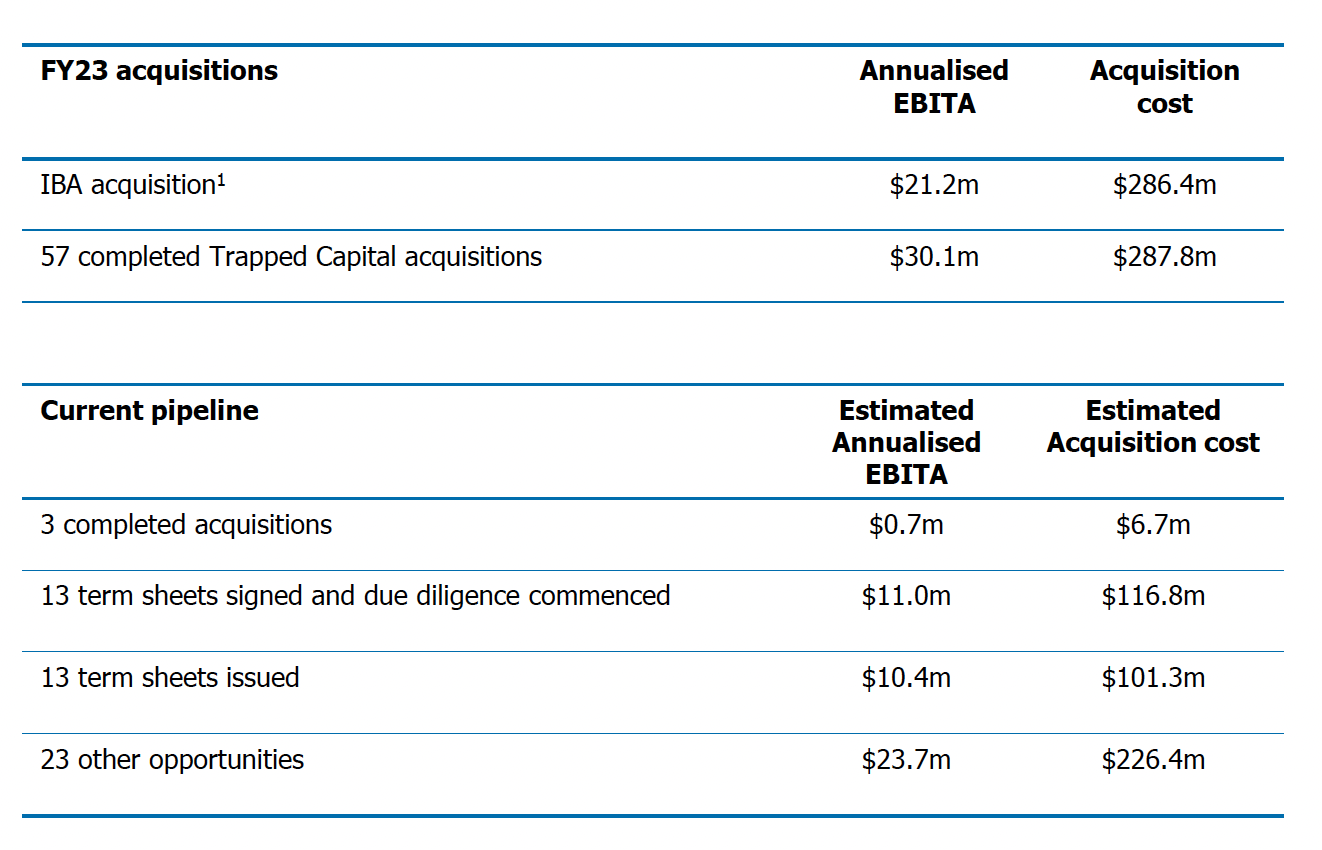

Assuming forecasts are met, Steadfast will pay a total of $280 million which represents an EBITA multiple of 10.33 and management expects the deal to be 1% earnings per share (EPS) accretive in FY24. This pricing is in keeping with other deals as can be seen in the following table taken from Steadfast’s FY 2023 results.

The purchase also appears to stack up on a strategic basis given Sure Insurance is a specialist regional Queensland residential property insurance underwriter. This fits with Steadfast’s strategy of acquiring niche providers which are typically subject to less direct competition.

Sure Insurance has a strong growth profile and there is a good chance this will be maintained under Steadfast’s ownership given favourable market dynamics, a low market share and the benefits of tapping into Steadfast’s distribution scale.

It strikes me that regional Queensland property is highly exposed to the risks of climate change which probably means that insurance prices there will continue rising over coming years. Inflation is good for underwriting agencies and brokers because they “clip the ticket” on premiums but are not exposed to insurance liabilities.

It might seem distasteful to think about profiting from a global calamity, but this is the situation we find ourselves in and provision of insurance helps to alleviate the fallout rather than contribute to it. Who knows, perhaps net zero will be achieved in time or regional Queensland will be relatively unaffected. Under those scenarios Sure may turn out to be merely a decent investment for Steadfast rather than an exceptional one. That would still be a fine outcome for Steadfast shareholders.

Steadfast Valuation

Taking the midpoint of FY2024 NPATA guidance, Steadfast shares trade on a price-to-earnings ratio just shy of 22 or an earnings yield of 4.6% and pay a handy dividend yield of 2.7%.

As can be seen below, the stock is currently moderately cheaper than its average valuation over the past three years.

For those interested in the details, I created the above chart by calculating the one year forward earnings (based on underlying EPS before intangibles or uEPSa) and dividend yields for Steadfast stock over the past three years. Under this methodology, the cut off for forward looking actual data is 30 June 2022 (since FY 2023 is the most recent set of full year accounts) and so calculations beyond that date use a combination of my own and company forecasts. For FY24 earnings, I used the midpoint of management guidance of between 11% and 16% growth in EPS. For FY24 dividends, I have predicted a 10% rise to 16.5 cents per share and for FY25, a further 12% growth in both EPS and DPS.

Steadfast has been a remarkably consistent performer over the years with uEPSa increasing by 13.4% per annum over the past decade (including FY24 guidance) and 14.1% over the past five years. Therefore, I am comfortable forecasting a continuation of this trend out to FY25 and think that 12% growth could prove slightly conservative.

Zooming further out, we see that the stock was significantly cheaper during the covid shock and in the first couple of years after listing before the story was fully appreciated by the market. The mini bear market of late 2018 was also a decent time to buy.

Looking back at the way the stock was valued in the past is useful, but ultimately limited because things change. With that in mind, here are some factors which might influence share price performance looking ahead.

Interest Rates – The RBA cash rate is at 4.35%, the highest level since Steadfast listed. Higher rates have driven down the price of long-term Government bonds which are as cheap as they have ever been over the same period. Therefore, even though Steadfast stock is trading on a reasonably high earnings yield relative to its own history, it may still offer less value today compared to investment alternatives than in the past.

Insurance Pricing – Steadfast’s fortunes are tied to insurance pricing which has been on an upward march over the past decade, accelerating in the post covid inflationary shock. We might speculate that this trend will continue given the looming climate crisis, but at least one driver of rising prices from the past decade may be shifting into reverse.

Insurance companies earned very low returns on the premiums they held during the low interest rate QE era. It appears that we are now in a new monetary paradigm characterised by higher interest rates and an end to QE. Time will tell, but this could lead to higher investment returns for insurance groups going forward alleviating some of the upward pressure on premium pricing.

In the HY 2024 results presentation, CEO Robert Kelly said that there are signs that price rises may be moderating going forward. However, he also said he sees a floor of two to three per cent in premium pricing growth per annum which would hardly be disastrous. On top of this, he says that many properties are underinsured within Australia and therefore we should see additional GWP growth as this shortfall is addressed.

Business Maturity – Future growth may be curtailed by the sheer scale of the business today. Including third-party brokers, Steadfast’s network now represents roughly a third of the Australian market defined by gross written premium. By the same measure, brokers in which Steadfast has an equity stake represent roughly a sixth of the market.

Would fading growth due to market saturation lead to a decline in valuation? Perhaps not, because slowing growth for this reason would mirror increased market dominance which means reduced risk for investors.

For example, Steadfast already boasts industry leading data in several insurance areas due to its superior systems and scale. This data is of great value to its insurer partners and represents a competitive advantage that is strengthening over time.

However, even if a valuation derating is off the table, declining earnings growth will still lead to a worse share price performance compared to the past.

The US Opportunity – In early October, Steadfast announced the acquisition of US based agency network ISU Group for US$55 million. This represents Steadfast’s initial foray into the US, potentially a significant step for the group.

The board has deliberated over this move for some time and Robert Kelly has deep insight into the US market having held a position on the board of ACORD for the past 13 years.

According to its website, ACORD is a “global standards-setting body for the insurance and related financial services industries” with offices in New York and London and 36,000 participating organisations across 100 countries. It exists to facilitate “the flow of data and information across all insurance stakeholders through relevant and timely data standards”.

One of Steadfast’s great strengths is the quality of its internally developed software systems which have been widely adopted by third party brokers in Australia. Such systems are a key component of Steadfast’s combined service offering which management believes is superior to what is currently offered in the US.

It would seem that management is approaching the US opportunity in typically measured fashion, having taken their time to plan the move carefully and initially committing only a modest amount of capital to test their model. Risk of failure seems relatively low whilst the potential reward is vast.

Early signs are that US acquisitions will be slightly more expensive than those in Australia at around 11 times EBITA. This compares to roughly 10 times EBITA that Steadfast paid for the $331.7 million of Australian acquisitions completed in the first half of 2024.

Steadfast potentially represents an attractive alternative to private equity buyers for US brokers looking to sell their businesses. This is because Steadfast is happy to purchase a proportion of a business rather than the whole thing which might suit owners wishing to remain involved.

My View

Steadfast is becoming more mature at home which may temper future returns, but not if its high calibre management team successfully executes the tantalising opportunity in North America. Macro conditions might be waning given tighter monetary policy and a possible softening in premiums, but if so only marginally. In any case, such things are highly uncertain and so not worth weighting too strongly. Meanwhile, the recent acquisition of Sure looks like yet another example of proficient capital allocation.

Overall, the HY 2024 results reconfirm my view that Steadfast is a quality stock at a reasonable price.

Disclosure: The editor (Claude Walker) of this article does not own shares in any of the stocks mentioned, whereas the author (Matt Brazier) owns shares in SDF. Neither will trade shares in any of the stocks mentioned for at least 2 days following the publication of this article. This article is not intended to form the basis of an investment decision and is not a recommendation. Any statements that are advice under the law are general advice only. The author has not considered your investment objectives or personal situation. Any advice is authorised by Claude Walker (AR 1297632), Authorised Representative of Equity Story Pty Ltd (ABN 94 127 714 998) (AFSL 343937).