Austco Healthcare Limited is an ASX listed company in the business of providing hardware in the form of nurse call systems, software & workflow management solutions to hospitals and aged care facilities around the world. Headquartered in Australia their main markets include ANZ, Asia, Europe, and North America. Listing on the ASX in 2004, the company has gone about a couple of name changes from TSV Holdings to Azure Healthcare Limited and finally settling on Austco Healthcare Limited in November 2020. Some may see these name changes as an orange flag for the business, and for good reason given past events that I will touch on later.

As reported in their HY1 2023 report that was released to the market last month, Austco’s revenue split was 62% from equipment sales, 20% from installation fees, and 18% from Software and SMAs (Service & Maintenance Agreements). Austco’s software offering focuses on advanced clinical workflow, task management and business intelligence solutions for the nursing industry. This is mainly delivered via a smartphone app named ‘Pulse’ which is sold as a licence to the operator either in perpetuity or over a finite period. Currently running at gross margins of 54.8% (up from 52.8% in PCP), Austco’s CEO Clayton Astles has stated that to improve theses margins, the company’s long term strategic goal is to achieve a 50/50 split between software and hardware.

This goal seems ambitious, but it the proportion has increased slowly over the years.

There is a possibility that this traction may be able to be generated by leveraging the relationships already formed through past provision of hardware devices. This can be evidenced by the $1.6m SMA signed with Ng Teng Fong General Hospital which was announced to the market in November 2021 which came off the back of the pre-existing relationship formed with this customer after providing their nurse call systems back in December 2020. If Austco can focus on leveraging these types of relationships successfully, we may see software sales increase as a portion of total revenue.

Austco recently released their HY1 2023 report. While a revenue increase of 24% on PCP the reported NPAT looks to be weak compared to HY1 2022. However, if you strip out the grants received for both periods, NPAT (Ex Grants) has grown $477k from $848k in HY1 2022 to $1.325m in HY1 23.

Reflecting management’s goal of increasing software revenue as a proportion of total revenue, this segment’s revenue grew a whopping 47%, to 18% of total revenue, compared to less than 12% back in 2019.

This increase was driven mainly by software sales in North America, which can be seen as a positive sign given the large potential for growth in this market.

On the other hand, one weak point in the report was cash flow. After stripping out payments for intangible assets and lease liabilities, it was a paltry $30k.

This weak result arises from lumpy cash receipts, and the increase in inventory on the balance sheet. The inventory build has been flagged by management as a strategic move to combat supply chain issues and work through the order book backlog, which currently stands at $20.3m.

The nurse call system industry is highly fragmented, with many companies competing for a total addressable market of about $1.69b $US in 2022. According to Fortune Business Insights, this market is tipped to grow at a CAGR of 13.3% to $4.07b US in 2029.

Fighting for a slice of this revenue, Austco’s competes with names such as JNL Technologies, Cornell Communications & Hill-Rom Services in North America, Wandsworth Healthcare in the UK, Honeywell Ackermann & Jeron in Asia, Ascom in Europe, and Rauland & Hills Healthcare in Australia & NZ.

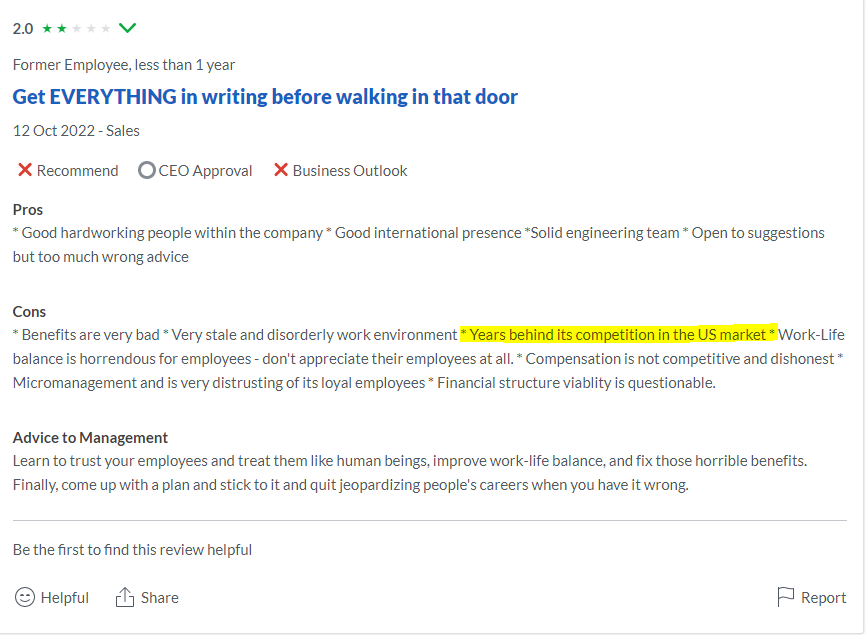

Whilst attempting to research Austco’s sustainable competitive advantage in what is a sea of competition in this industry, I came across conflicting views, each with likely biases. One former sales employee on Glassdoor said the company is ‘years behind the competition in the US market’.

On the other hand, I have spoken with a technical Engineer with 9 years’ experience working with nurse call systems in Asia. He believes that Austco products stand out positively in terms of quality and durability. From his LinkedIn profile, I can see he has worked with products from Honeywell Ackermann and Jeron being a couple of Austco’s competitors in this region.

Most of Austco’s revenue is from one off contracts with hospitals that are won through aligned suppliers. These Hospitals are either in the final stages of being built or undertaking upgrades, such as the latest deal with the Colchester General Hospital in April 2022. This kind of lumpy revenue is much more expensive to attain, with sales and marketing expenditure needing to play a big role. This is illustrated by the big gap between Austco’s GP & NPAT margins over time. This gap has only widened further on the release of the HY 23 report:

Without a substantial shift to software sales, I find it hard to see how this gap is going to close.

As hinted at the beginning of this article, Austco comes with some baggage of past management ructions.

In 2014, when it was trading under the name of Azure Healthcare then CEO seemed to sell right at the peak of optimism only for shareholders at the time to cop the brunt of a share price decline from a top of 45c in September 2014 all the way down to a low of 9.8c on 28/08/2015. 15 days after the company produced a stellar 2013 annual report where they achieved a 271.7% uplift in NPAT, then CEO and founder Robert Grey offloaded 37% of his shares in the company for 45c a share. According to the announcement released to the market on 05/09/2014, this was done to ‘to assist with the liquidity of the stock’. This explanation may have provided some comfort to shareholders at the time had the company not announced on 10/11/2014 that profit for the 6 months to 31/12/2014 would be decreasing from $2.17m to between $0.8m and $1.2m. As it happened, upon the release of this announcement, the share price dropped from 44.1c on 7/11/2014 to close at 23.5c on 10/11/2014. The back half of 2015 brought about a further announcement of decreased profits, ultimately ending in Azure posting a profit of $1.098m for the full year to 30/06/2015. By this time the damage was done and resulted in a share price fall of 78%. This ultimately led to now CEO Clayton Astles replacing Robert in the top job on 31/07/2015. As at 30/06/2022 Robert is still the majority shareholder of Austco, holding 54.5m shares (or 19.18% of the company).

Based on annualising the first half, Austco stands to make $3.36m in NPBT in 2023. At a share price of 12.5c, Austco has a market capitalisation of about $36m, and around $6m cash.

If we applied a standard 30% tax rate to this, that would imply net profit after tax of about $2.35m. However, with accumulated losses Austco is likely to enjoy a lower tax rate; it was about 18% in the first half. If we double the first half profit we get about $2.6m and using this slightly more generous figure Austco is trading at around 14x its earnings run rate.

Management’s ambition of increasing software revenue as a portion of their total sales seems to be starting to come to fruition, and that could support profit growth.

It is also possible the company can increase hardware sales. If they can do this and focus on attaining a consistent profit margin of around that 10%, then profit will grow.

The question is, what will the largest shareholder of the company do if positive sentiment does return to the stock?

Disclosure: the author of this article owns shares in AHC but will not sell any for at least 2 days following this article. The editor of this article Claude Walker does not own AHC shares. This article is not intended to form the basis of an investment decision and is not an official recommendation. Any statements that are advice under the law are general advice only. The author has not considered your investment objectives or personal situation. Any advice is authorised by Claude Walker (AR 1297632), Authorised Representative of Equity Story Pty Ltd (ABN 94 127 714 998) (AFSL 343937).

Sign Up To Our Free Newsletter