Hitech Group Australia (ASX: HIT) is a company that was founded in 1993 and listed on the ASX in 2000. The main revenue stream for Hitech is in the provision of recruitment services to both the government and private sector. Hitech is focused on the information and communications technology sector, but they also provide recruitment services in both the finance and office support sectors.

Hitech Group Australia was founded and is still currently run by brothers Ray Hazouri and Elias Hazouri, who with George Shad make up the board of directors. Elias (who is the current CEO) together with his brother Ray hold approximately 70% of the company’s 39,000,000 shares on issue.

That high insider ownership is fantastic when it comes to aligning the interests of shareholders and management, but also means there is little free float available for external shareholders. Therefore Hitech Group Australia stock is very illiquid, and would only really be interesting for microcap investors who fully understand the risks of getting trapped in an illiquid ASX minnow.

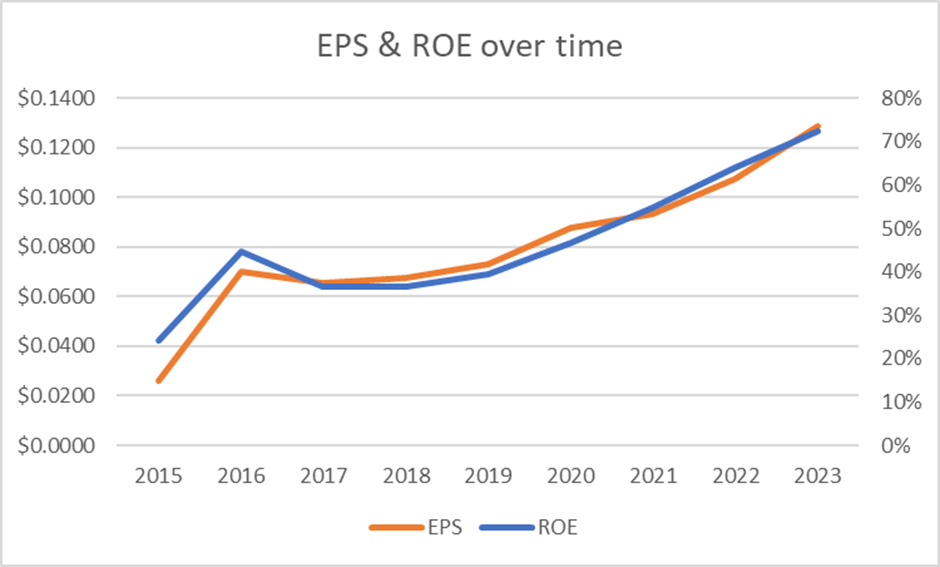

What first got me interested in Hitech was the stellar earnings growth for 2015 to today, produced while the company also achieved improvement in Return on Equity (ROE), a classic quantitative sign that suggests a business does not require new capital to grow.

Since 2015, Hitech has grown EPS at a CAGR of 22.1% from 2.61c per share in 2015 to 12.89c per share in 2023. In that period, ROE has gone from an already impressive 24% in 2015, to an incredibly impressive 72% in 2023. While in some ways this high ROE simply reflects the capital light nature of of a recruiting business (combined with strong demand), it is still an attention-grabbing high rate of return. The below chart shows the Hitech Australia Group EPS growth (left scale), and ROE (right scale), over time.

Of course, the more important question for investors today is if the company can continue to produce these kind of returns moving forward.

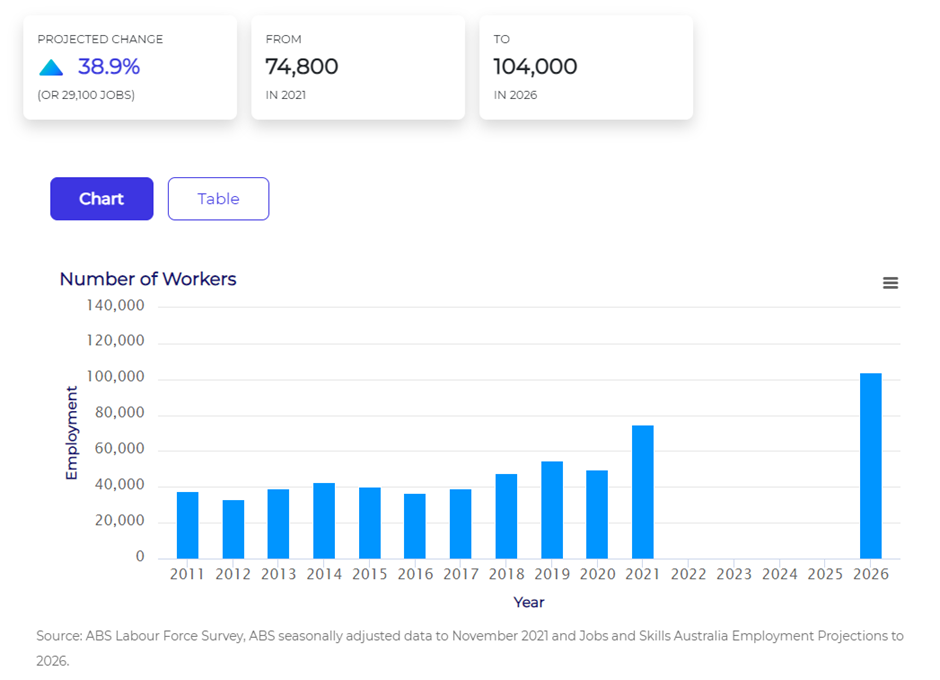

An obvious tailwind helping Hitech in its mission to achieve this is the increasing digital reliance in today’s society, and particularly the need for more and more IT professionals within government departments. Zooming out, I think that this trend will continue. For example, in 2021 the Australian government labour markets insights page has tipped the ‘Database & Systems Administrators & ICT Security’ labour market to grow at 38.9% per year to 2026

Another tailwind is the current skill shortage. As recently as October 2023, Professor Peter Dawkins said ‘Shortages were also pronounced, and grew the most, for Professionals, particularly Health Professionals like nurses and GPs, but also ICT professional groups and various types of engineers, especially civil engineers, mining engineers, mechanical engineers and engineering managers…’

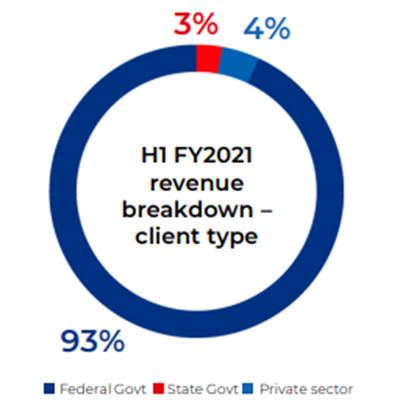

While having the Australian Government as a large customer can be seen as a positive for Hitech given the trust they would have built up, it also presents the company’s greatest risk. The last update on their revenue mix came way back in June 2021, whereby 97% of their revenues came from government agencies, which I would imagine hasn’t changed too much since, as there has been nothing conveyed by management to broadly address this issue.

This reliance is the key risk when looking at Hitech as there has been a move from the Australian government to cut back on outsourcing, something that has been spoken about for a long time as evidenced by news articles as far back as April 2022 stating ‘Labor pledges to cut government outsourcing by $3b’.

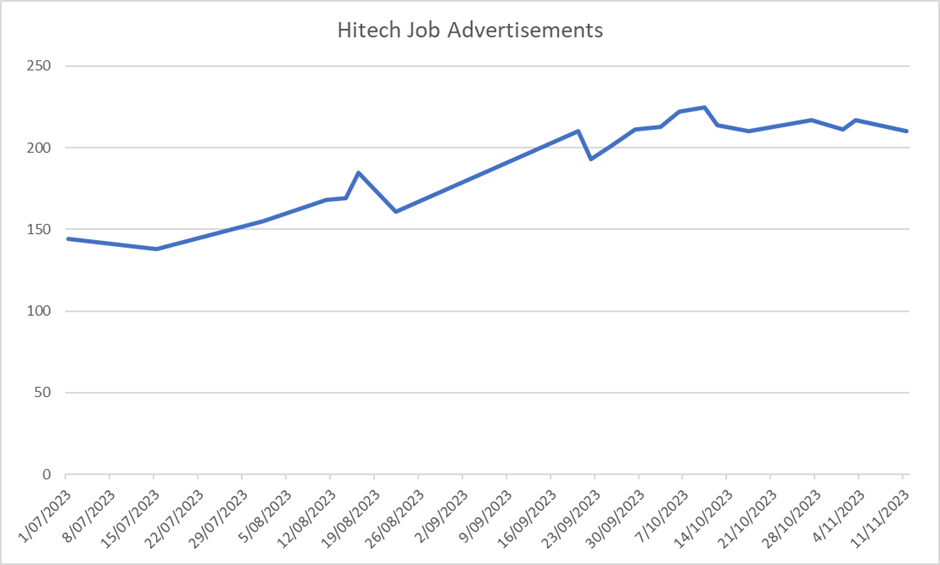

Whether or not this potential cut back is currently playing out in the ICT space and affecting Hitech’s revenues is the question. To assess this, I have been monitoring the job advertisements on the Hitch website weekly since July 2023 where around 80% of the job vacancies advertised are with government agencies. This has shown a steady increase in advertisements throughout this period, indicating good momentum since the start of the year.

It is worth noting that without comparisons to prior years, it’s hard to tell how this momentum really compares, as it might just reflect seasonal drift. Nonetheless, it is something investors could monitor moving forward as any drop-off might reflect the impact of government cut back on outsourcing spend, and how it is affecting Hitech specifically.

The current macroeconomic climate is also a genuine risk for Hitech, with figures released recently on job vacancy advertisements showing substantial declines in job vacancy advertisements over the past year.

While these risks don’t necessarily invalidate the hypothesis that Hitech is a good quality business, it is still worth keeping in mind that these factors outside Hitech’s control may impact its earnings. When you combine the potential for extraneous events to hit earnings, and consider the illiquid nature of the stock, there is definite potential for a sudden share price hit should fundamental results disappoint.

Another small risk with this company is that as at 30/06/2023 Hitech had $10m in cash on the balance sheet. While this is a positive in terms of balance sheet strength, there is also a risk of malinvestment by the management team. It is something to watch moving forward and if management can’t find a suitable use for these funds, it’s probably better off being returned to shareholders.

At today’s price of $2, Hitech is trading at a trailing PE of a around 15.5 and trades on a trailing dividend yield of around 5%, fully franked.

For a company that has grown EPS at a CAGR of 22% for the past 8 years, has $10m in the bank and no debt, and has recently moved to a 100% dividend payout ratio, this feels like a good value proposition.Of course, the operating leverage inherent in the business means this investment would only be suitable for experienced microcap investors who are comfortable taking on higher risk as part of a diversified portfolio.

Hitech stands out to me for its excellent progress over the last decade, high board alignment, and solid fully franked dividend yield. But shareholders could certainly be in for a very bumpy ride if the economy hits turbulence.

Disclosure: the author Benjamin Sayers owns shares in HIT and will not trade shares within 2 days of publication. The editor Claude Walker does not own shares in HIT and will not trade within 2 days of publication. This article is not intended to form the basis of an investment decision. Any statements that are advice under the law are general advice only. The author has not considered your investment objectives or personal situation. Any advice is authorised by Claude Walker (AR 1297632), Authorised Representative of Equity Story Pty Ltd (ABN 94 127 714 998) (AFSL 343937).

The information contained in this report is not intended as and shall not be understood or construed as personal financial product advice. You should consider whether the advice is suitable for you and your personal circumstances. Before you make any decision about whether to acquire a certain product, you should obtain and read the relevant product disclosure statement. Nothing in this report should be understood as a solicitation or recommendation to buy or sell any financial products. A Rich Life does not warrant or represent that the information, opinions or conclusions contained in this report are accurate, reliable, complete or current. Future results may materially vary from such opinions, forecasts, projections or forward looking statements. You should be aware that any references to past performance does not indicate or guarantee future performance.