When it comes to investing, most of my portfolio is in long term high quality businesses that I am willing to hold for the (very) long term. However, I’m also inclined to make some investments based on the current zeitgeist. The problem with this approach is that it is first order thinking, and first order thinking trades rarely last for very long. Quite quickly, the market factors in the new information and (usually) even overshoots. That means that if you’re coming too late to a first order play, you can end up losing money.

That said, while remaining mindful of the risks, I couldn’t resist trying to tilt my portfolio more towards companies that might benefit from the current zeitgeist. The way I see it, we are currently in a period where useful things are scarcer due to the added expense and difficulty for sourcing and transporting them. If you’ve purchased a car within the last few years, I recommend checking out the going price on Carsales.com. You might find that the sale price (likely above what you could get for it, after frictional costs) is closer to what you paid, then you would generally expect.

The Russian invasion of Ukraine, covid, and low rates have set the scene for commodity price increases across the board. Overall, I think it’s well worth acknowledging the reality we are currently in, because none of us really knows how long it might last. Is the only antidote demand destruction from high prices?

This article has some similarities with my article on 5 companies insiders have been buying recently, in the sense that some constituent companies will initially benefit from increasing prices, but may subsequently suffer, if higher prices destroy demand, or if input costs also rise. So keep in mind the benefits of higher commodity prices may be short lived.

RPM Global (ASX: RUL)

One of the good things about software is that it tends to have superior economics than mining, because once it is in use, it is much less replaceable by a competitor. Whereas a steel mill can switch iron ore providers quite easily, it’s much more difficult and costly for an iron ore miner to switch the software it is using.

Historically, I have thought RPM Global’s transition from licence fee model to subscription model created an opportunity for investors. Indeed, I recommended it to Hidden Gems, way back in 2016, at a share price of 40c, and my father in law has held it since 2017. Personally, I have avoided it because it was so involved with new coal mines, which I generally oppose.

More recently, the company has become less involved with coal specifically with its expansion into ESG advice and the divestment of its coal gas testing business. It’s still not my favourite business, but I don’t think all mining is bad and RPM Global gives a software quality exposure to the mining industry. It has capable management and in the most recent half (H1 FY 2022) it recorded a profit of $1.4m after tax from continuing operations, compared to a loss of $2.2m in the second half of FY 2021.

Personally, I think that the company is roughly fairly valued at a share price of $1.85 and market cap of $430m, but I wouldn’t be surprised if booming commodity prices sees a little extra demand for their services, particularly the lower quality advisory business (which displays strong operating leverage). If that’s true then we could see RPM Global score a decent profit in FY 2022, with a stronger second half, and the potential for further gains in FY 2023.

The company says: “With a strong balance sheet, healthy cashflow, plenty of M&A opportunities, competitive advisory and software offerings and new software products about to be released, we continue to be excited and optimistic about the year ahead.”

Obviously, this is a high priced software stock; and even once it becomes profitable for a full year, it will probably be on a P/E multiple in the hundreds. Therefore, I note the potential headwind in the form of higher rates pushing down growth stock valuations. But at least there should be some benefit from the commodity price boom, so I’ve bought some shares recently. My share purchase is partly to encourage myself to keep a closer eye on the business.

RPM Global has been transitioning its business over the last few years. Software division sales in the six months to December 2016 were $26.1 million, including $11.6 million in one-off license sale software. Software division sales in the half to December 2021, 5 years later, were only $17.8 million. However, the difference is that in the more recent half, just $1.25 million came from one-off license sales down from just $1.8m in the prior corresponding period. Therefore, the reported revenue growth headwind from transitioning to a subscription model is now almost completely over.

Firefinch Limited (ASX: FFX)

Firefinch is a loss making gold miner with a would-be lithium miner, Leo Lithium, as a subsidiary. The company is based in unstable Mali, and there is no guarantee that the company will ever pay out dividends at all. With all this risk, one could argue that the lithium side of the business has missed out on some of the speculative excesses that have driven lithium exploration companies to ever higher share prices.

In the last half year report, the company said:

By way of ASX announcement dated 9th February 2021, the Company announced its intention to demerge the Goulamina Lithium project into a separate ASX-listed lithium-focused entity to be called Leo Lithium Limited. Timing for the demerger will depend on the completion of the Goulamina JV Transaction and achievement of FID. Firefinch currently intends to seek shareholder approval for the demerger in February 2022, with completion and ASX listing during the March Quarter, 2022 (subject to various ASX and other regulatory approvals and rulings).

More recently, the new CEO of Leo Lithium, Simon Hay, who was previously CEO of Galaxy Resources, said:

“the Goulamina Project is advancing apace on all fronts, with detailed engineering about to commence and selection of an EPCM contractor underway. In Mali, site works are ramping up with a sterilisation drilling program in progress ahead of commencement of drilling to target conversion of Inferred Mineral Resource to Ore Reserves. Early civil works will start in February.”

However, the company seems to be running behind schedule with the demerger. My guess is that once the actual demerger is announced, there will be more interest from people who would like to own Leo Lithium shares. As a result, I’ve bought some shares in Firefinch at 90.5 cents, and I will probably look to sell some or all of them just before the demerger happens. I don’t generally invest in mining companies. I’m making an exception in this scenario because I would like to learn more about lithium, and the demerger puts a time limit on my involvement. In the meantime, this exposure replaces my (much larger) holding of ASX:GOLD, which I have sold out of. I also note that existence of these mines in Mali might be considered a bad thing, though I would have thought overall they are a net positive.

Sign Up To Our Free Newsletter

Laserbond Limited (ASX:LBL)

Laserbond was founded in 1992 by engineer Gregory Hooper along with other members of his family. Brother Wayne Hooper, also an engineer, joined the company in 1994 and the two still run it today. Gregory is responsible for much of the technology the company has developed over the years and Wayne is focused on business strategy and operations.

Laserbond has three operating divisions: services, products and technology. The services business is reclamation work where customers wish to extend the life of equipment. In many cases, Laserbond treated equipment can last more than twice as long. The products division makes new equipment for either OEMs or under Laserbond’s own brand name. These products are designed to last much longer than competing products that have not undergone a similar surface engineering process. Finally, Laserbond manufactures laser cladding rigs which it sells overseas to customers in non-competing industries along with ongoing training and maintenance.

In an inflationary environment, the value of increasing the lifetime of equipment goes up, and so too should the value of Laserbond’s services. If you look at the graphic from their most recent results you can see that they have pretty reliably earned $2.8m NPAT in the last few years. The current market cap of $97m at the current price of 89 cents per share, is almost 35x that historic level of sustained profit.

However, the most recent half was a little stronger, and the company said it is expecting a stronger second half from its services division because of “the Victorian cladding cell available from January and the newly acquired QLD cell. These two new cells will also free up capacity in NSW and reduce lead times for all customers across all states.” If we assumed a solid $3.2m profit, then the company would be trading on around 30x earnings, which is probably quite reasonable.

I don’t currently own shares but I could see myself buying some if the share price dropped (or earnings came in above what I thought they would).

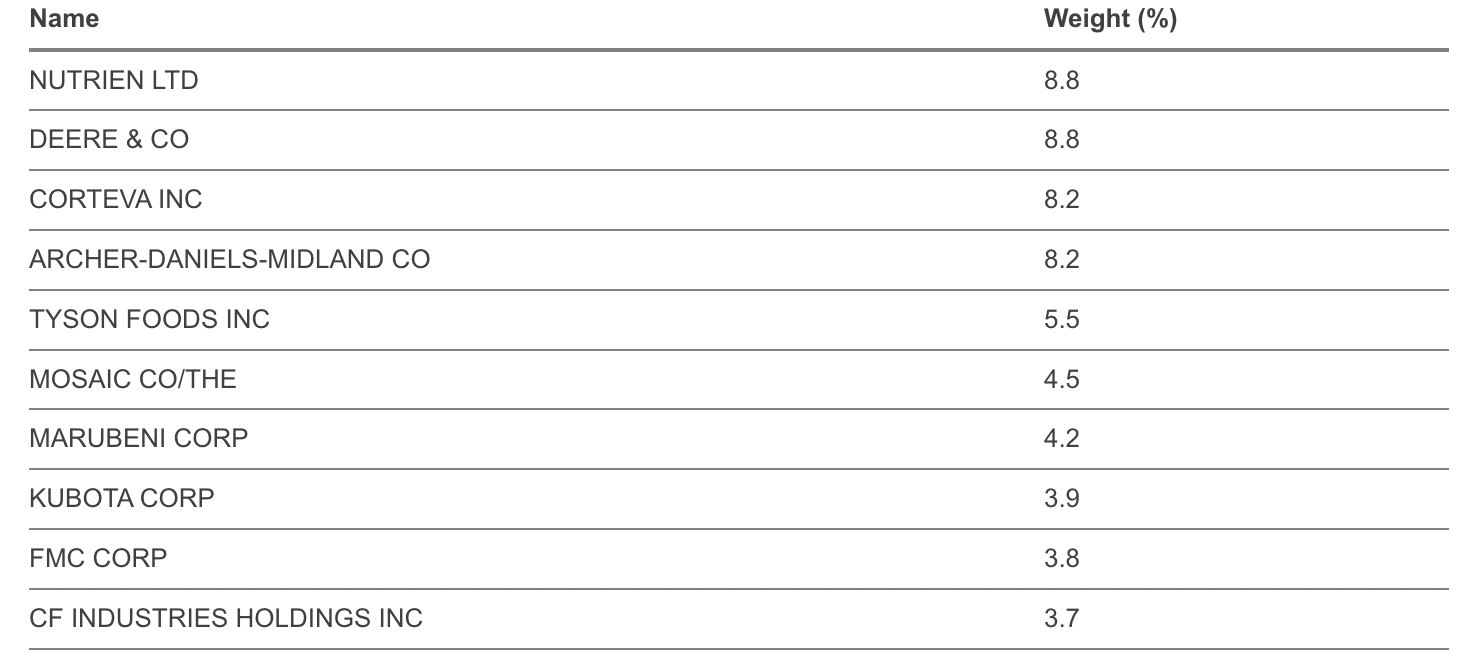

Betashares Global Agriculture ETF (ASX: FOOD)

FOOD is an ETF that holds a collection of companies that supply and support farmers to make food.

With supply chains under pressure, Elders reported that many farmers are stocking up. Logically, this should lead to one-off additional demand for products sold by these companies. If you are a farmer, and you think prices are going up, it makes sense to buy your tractor now, or your fertilizer, to avoid paying up, down the track. And of course, farmers should be feeling confident, as global wheat shortages should help ensure higher prices for their food products.

I bought units in ASX: FOOD for this reason, at a price of $7.99. The current price is $8.45 and you can see below that the ETF is sitting on its highs. I’ll probably look to sell it soon as I think that this fairly obvious short thematic must be fairly fully priced quite quickly, and it may already be overweighted. The “stocking up” event only really pulls demand forward and I was probably a bit late to the trade.

Please remember that these are personal reflections about a stock by author. I own shares in RUL, FOOD, and FFX, albeit all with low conviction. This article should not form the basis of an investment decision but is merely me documenting the rationale for why I did something. It is an investment diary valuable only for the cognitive process it demonstrates. We do not provide financial advice, and any commentary is general in nature. Please read our disclaimer.

Sign Up To Our Free Newsletter