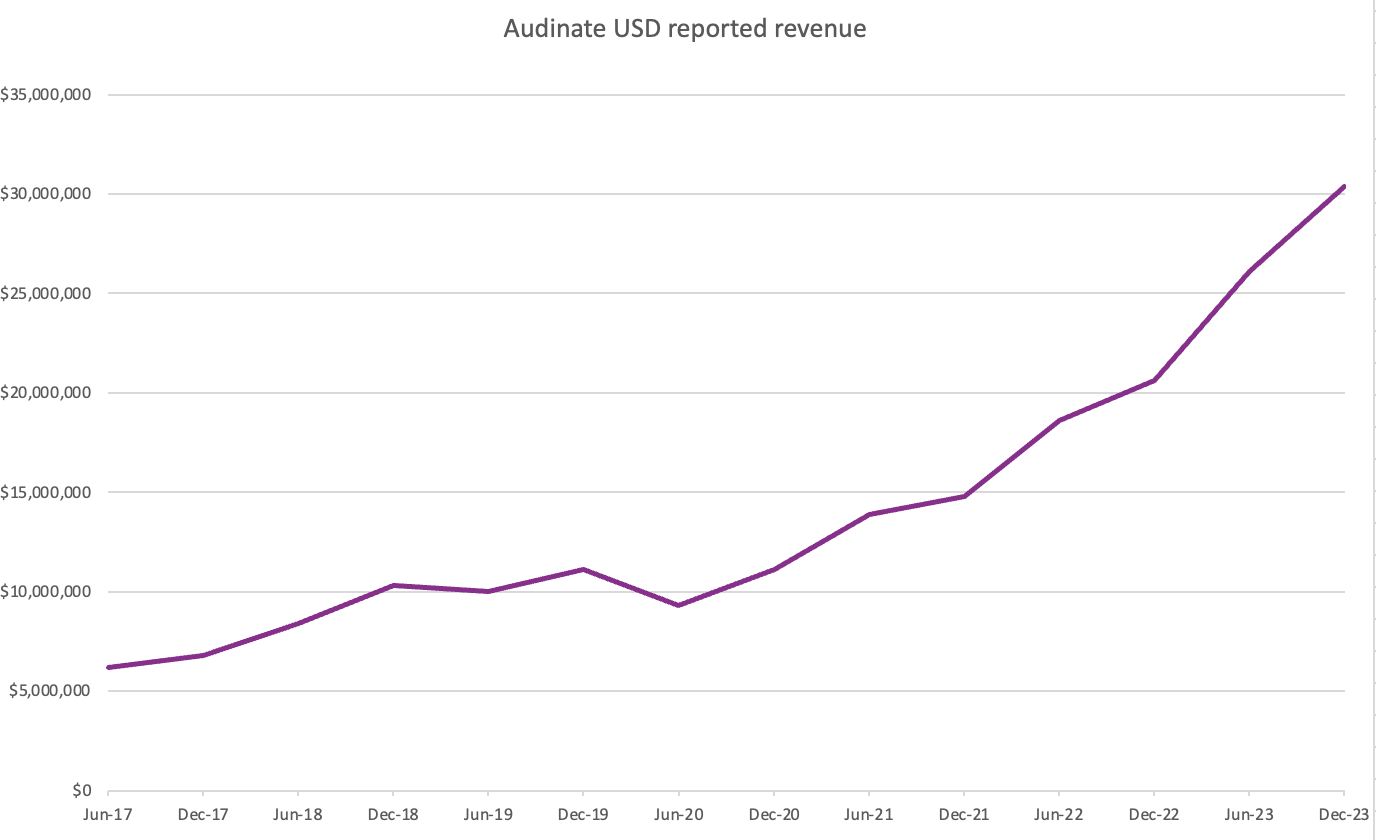

AV technology provider Audinate Group Ltd (ASX:AD8) released their 1H 2024 financial results today reporting an impressive 47.7% increase in US dollar revenue to $30.4 million. As the Group invoices its customers in US dollars, this currency is a more relevant measure of sales performance.

AUD revenue was up 51.1% to $46.6 million for the half thanks to a favourable exchange rates with profit before tax of $5.6 million, a $6 million improvement compared to the prior corresponding period. Net profit after tax was $4.7m, up on a mild loss in the prior corresponding period. We’ve previously covered Audinate extensively here. You can see by the below graph that revenue tends to be stronger in the second half. Shareholders will be hoping it’s a trend that continues.

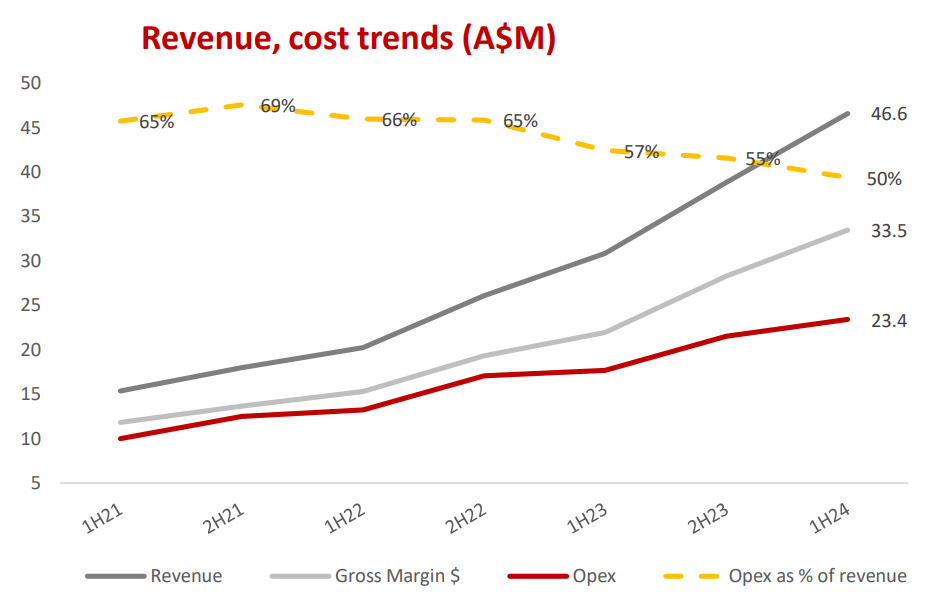

It has been well documented that Audinate’s gross margin has been under pressure following a change in product mix.

With easing supply chain issues it had been flagged that in the long term the gross margin would return to 75%. The overall gross margin percentage increased to 71.8% from 71.2% in the previous corresponding period although down from 72.1% at 30 June 2023. Audinate continues to work through the backlog of demand for Ultimo chips which are lower in margin compared to software It expect that gross margin will continue to improve as a more favourable product mix is found with less chips and more software.

With an increase in revenue and managed overheads Audinate saw earnings per share increase from (0.49) cents to 5.88 cents. The below graph from the presentation clearly showing that improving revenue and gross margin is flowing through to the bottom line with operating expenditure continuing to reduce as a percentage of revenue.

Revenue to cash flow conversion was again strong.

The AU $46 million collected in receipts aligned with revenue, while the total cash flow for the period was skewed by a capital raise and term deposit movements. If you were to use operating cash flow less property plant & equipment, intangibles and lease payments as a definition of free cashflow, then Audinate produced positive free cash flow of $3.4m up on negative free cash flow of $6.8m in 1H2023. A truly stunning improvement.

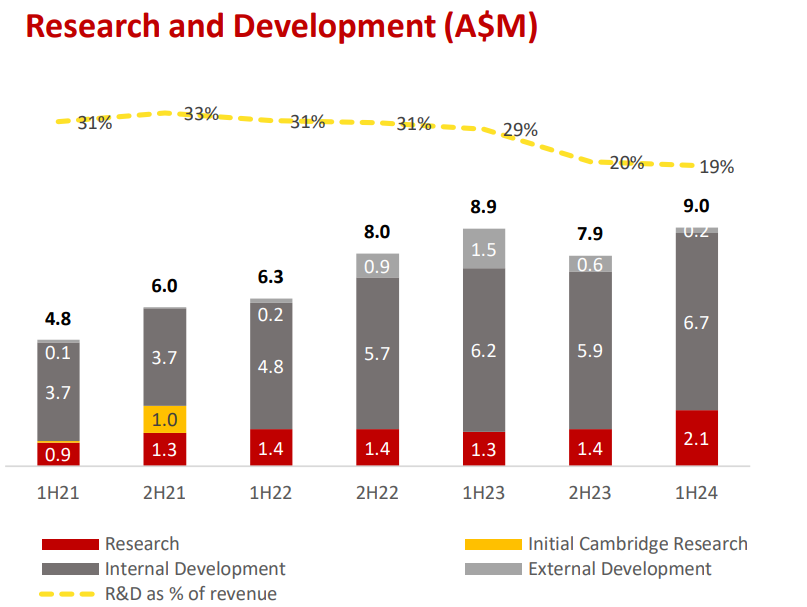

Historically Audinate capitalises a large portion of development costs which improves profitability and is identified through the cash flow statement. In the first half capitalised intangibles actually decreased compared to the prior period. The percentage of revenue spent on R&D activities continued to drop and is now below 20% of revenue.

Time will tell if this trend continues, particularly with the company’s continued progression into video.

In 2023 Audinate had the goal of shipping 10,000 video units.

At the AGM Aidan Williams stated they were targeting 30,000 units for 2024. Today he confirmed the company has already achieved this goal 6 months earlier than expected. Williams has previously noted that it took 6-7 years for the audio business to generate as many products as the video segment has done in a few short years. Fifty manufacturers now licence Dante video offerings, an increase from thirty, 12 months ago. And 66 video products have been released by customers, triple the number of products available at 31 December 2022.

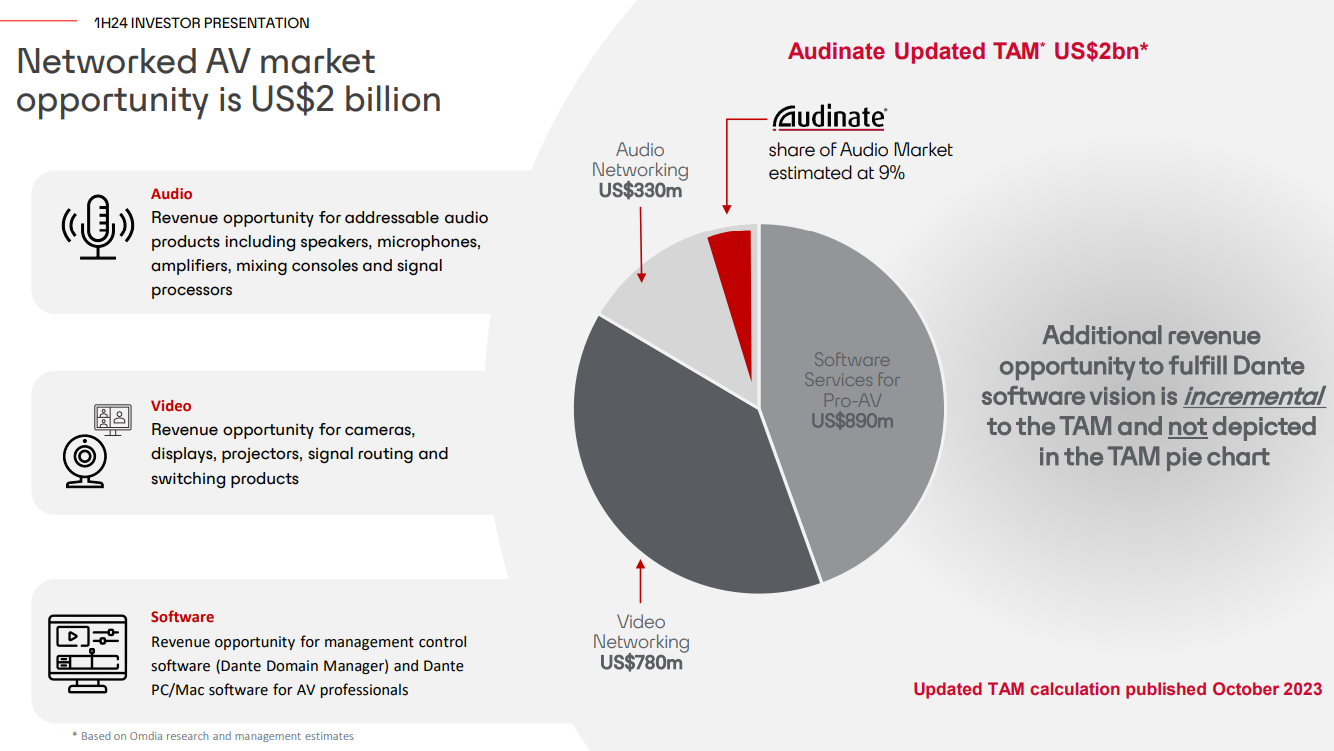

Management are also excited by the potential of the audio business, since they recently updated their total addressable market estimation. An updated TAM always something to be cautious of.

Cashed Up Balance Sheet

Audinate successfully completed its AUD $20 million Share Purchase Plan last year, following its $50 million placement to institutional investors back in October 2023. The intention of the raise was to ‘deliver organic growth through continued strategic investment in new and innovative products, ‘Win in Video’ by building on early success and to provide flexibility to explore a pipeline of identified bolt-on M&A opportunities’. At the end of December Audinate held over $111 million in cash and term deposits. While I’m okay with the company not spending for the sake of it I would like to see that cash put to use sooner rather than later. Perhaps the raise could have waited?

Prior to the raise and following the full year results Audinate had a little over $40 million in cash and term deposits. The raise definitely caught investors off guard (or at least me). Even with negative free cash flow it seemed at the time funds wouldn’t need to be raised in the short term.

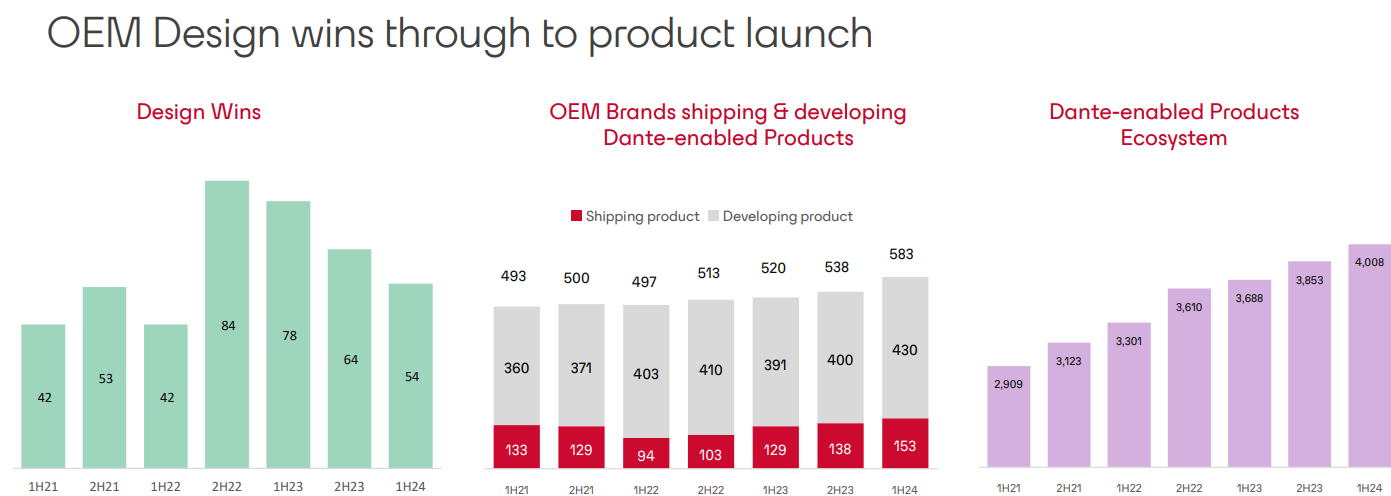

Audinate Units Shipped, Revenue per Unit & Design Wins

Design wins continued its decline post pandemic.

2022 saw an increase in design wins due to chip shortages, customers were required to update their products to address shortages. I raised on the call whether the continued decline was of any concern. CFO Rob Goss wasn’t overly worried and pointed to the continued increase in products shipped as well as the increase in Dante-enabled products in the ecosystem.

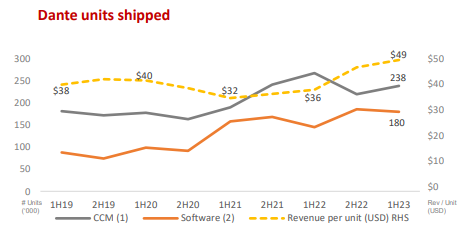

A useful metric that was previously reported was the revenue per unit.

The last time this metric was presented was 1H 2023 which showed USD $49 per unit shipped.

Per the full year results I had estimated this cost had dropped to $44 per unit.

To 31 December 744,000 Dante units were shipped with $30.4 million in USD revenue generated. This equates to around $41 per unit. Given the reported metric has not reappeared I might assume it continues to decline. I think that the increasing proportion of Ultimo chips are bringing down the revenue per unit.

Audinate Valuation & Outlook

The sharemarket has lapped up the results with Audinate trading as high as $19 at the time of writing.

Assuming Audinate can repeat the lofty 30%+ growth on full year 2023 revenue the company would be trading at close to 14 times sales, incredibly expensive particularly in what we’ve seen in the last few years with lofty technology valuations. Perhaps the difference here is Audinate is growing at a rapid rate and now showing signs of consistent cash flow generation and profitability. Historically I’ve looked to cash flow as a valuation target. With operating cash flow a vague guide to EBITDA (1H $11.7 million) if it can repeat this for 2H and hit close to $23 million, with a market cap of $1.3 billion it trades close to 56 times operating cash flow!

Looking forward the company expects growth in US dollars to be consistent with prior years. The good news is that management expect profitability and operating free cash flow is here to stay. The company will continue to explore M&A opportunities given its warchest of cash particularly in the video space.

For me, I’m happy to continue holding for the long term. The company is under pressure to execute given its extreme valuation but so far to date revenue growth has been exceptional and we could be at the beginning of an inflection point where the jaws of operating leverage begin to open up. As David Gardner would say, let your winners run. High.

Disclosure: The author of this article Nick Maxwell owns shares in AD8. The editor Claude Walker does not own shares in AD8. Neither will trade AD8 shares for at least 2 days following the publication of this article. This article is not intended to form the basis of an investment decision and is not a recommendation. Any statements that are advice under the law are general advice only. The author has not considered your investment objectives or personal situation. Any advice is authorised by Claude Walker (AR 1297632), Authorised Representative of Equity Story Pty Ltd (ABN 94 127 714 998) (AFSL 343937).

If you would like to be among the first to receive articles like these, and even suggest small-cap mailbag articles yourself, then you can click here to join the waitlist to become a Supporter.

Sign Up To Our Free Newsletter