It’s been a busy seven months for Austco Healthcare, and given we have received full year results, I (Benjamin Sayers here) thought it would be appropriate to revisit my thesis for investing in Austco Healthcare.

Since it reported the H1 FY 2023 Austco Results, Austco has released a steady stream of announcements to the market, and following on from this, its FY 2023 results. These announcements, along with some interesting news in relation to one of their Australian competitors has forced me to re-look at my thesis for owning the stock, something that is vital when investing, to try to combat the many cognitive biases that can creep into our thought patterns.

On the 22 of May, Austco advised the market of a $3.9m contract win at Maple View aged-care facility in Athens, Ontario, Canada. This was followed soon after on 16 June 2023 by the announcement of the company’s largest ever contract win of $7.4m, again in Canada at St. Paul’s Hospital in Vancouver, British Columbia. This contract will span over multiple years to be finalized in 2026. Having two major contract wins, one after the other, with one being the largest in the company’s history, shows that Austco are on their way to becoming a trusted brand within the nurse call system industry, especially in Canada.

Just prior to Austco announcing their largest ever contract win, On 13 June 2023, a competitor for nurse call systems within the Australian market, Hills Limited, appointed administrators.

This can sometimes prove to be a short-term tailwind for others in the same industry, as new and existing work that was being completed by Hills will need to be redistributed amongst the remaining players in the industry, of which Austco is one.

Something that will bolster the tailwind of Hills going into administration is Austco’s acquisition of Teknocorp, announced on 29 May 2023. Teknocorp is an Australian communications hardware and software solutions provider and certified Austco Nurse Call reseller which was acquired by Austco to align their Australian region with their strategy to build its direct sales capability, as is already the case in other regions such as North America.

This acquisition will be immediately earnings per share accretive and will add $1.1m of EBITDA in 2024. With the purchase price of $3.85m, this looks to represent good value at 3.5 times EBITDA. However, there is always some risk when you buy a reseller, because other resellers who sell your products might now consider you the competition.

With this acquisition, Austco are better placed to take advantage of any extra work that is made available due to Hills going into administration.

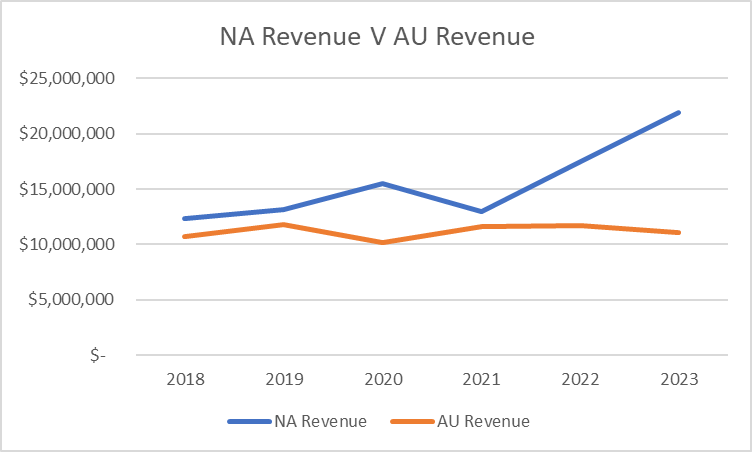

As can be seen from the past growth, it looks as if this direct sales capability has brought about great results in North America, which has grown revenue at 35% from 2021 to 2022 and 25% from 2022 to 2023. If this strategy within the Australian market can be executed to the same standard, Austco could see revenue in the Australian segment increase meaningfully over the coming years. As highlighted by the chart below, the contrast in revenue trajectories between these 2 geographies could not be more apparent, since introducing the direct sales strategy into North America in 2021.

Following on from the busy months leading into the end of FY 2023, Austco released their results to the market on 24th August 2023. These results saw headline NPAT fall 3% from $2.32m to $2.26m, while on the surface this looks disappointing, if we strip out the COVID grants and other income received in both years, it shows underlying NPAT increasing from 2022 to 2023. On top of this, the company seems to be making serious headway in their ambition to have 50% of their revenues come from software sales, with this segment of the business growing from 14.95% of revenues in 2022 to 20.2% of revenues in 2023. This growth is mainly due to the North American market where software revenues increased by 102% to $5.8m. It seems that on the back of the increased software sales, gross margin increased slightly to 53.44%, however, if you look at the trend between the increase in software sales and gross margin, it shows that there is no real correlation between these two variables, with GM continuing to hover around the 50% mark, despite software sales moving from 10% of revenue to 20% of revenue.

It is important to note also that management has indicated that gross margins in 2023 were negatively impacted by supply chain issues & higher logistics costs, so I expect these margins to increase throughout 2024 and beyond as these pressures abate.

Although revenue growth and gross margins are improving, if you refer to the cash flow statement, free cash flow for 2023 was negative $540k. This reflects the lumpiness of the business’s cash flows and is mainly driven by the large increase in receivables in 2023. This is an area of concern and is something I will be looking out for throughout the 2024 FY.

The final new piece of information released to the market was released on 19 September 2023 with Austco’s roadshow presentation. In this update they provided the market with an order book update that it had increased to $37.2m, which is a 50% increase on the orderbook that was held in September 2022 and suggests the increase in marketing spend in 2023 is doing its job nicely.

Given all the good news since we covered the stock in April this year, the stock price has responded by increasing 48% from 12.5 cents at the time of that article, to 18.5 cents today.

One of the issues I raised in my previous article was what would the major shareholder and former CEO Robert Grey be doing on such an increase. A look at the company’s top 30 shareholders pleasingly shows that Robert has not sold any shares this year, which has provided limited selling pressure and allowed the price to rise on good news.

All in all, 2023 was a good year for Austco, no doubt. However, the string of positive announcements didn’t quite translate into a bumper 2023 FY report. This makes the 2024 FY very important for the company. Given the increasing order book, I expect that revenue growth should be strong in the 2024 FY and beyond.

In order for my initial thesis to hold, this revenue growth will need to translate into better profits and more importantly cash flows for the shareholders. It should be much easier for Austco to do this as their gross profit climbs, as this it is reasonable to expect that operating expenditures should rise less than revenue.

However, the trailing price to earnings ratio of about 20x suggests the market is already pricing in some earnings growth. While I am no longer buying the stock at these prices I continue to hold in Austco Healthcare.

For now, my thesis for Austco remains on track.

Did you enjoy this coverage? Enter your email below to receive occasional free emails with otherwise hidden content, or click here to join the waitlist to become a Supporter, with access to all our paywalled content, including all our recommendations.

Sign Up To Our Free Newsletter

Disclosure: the author Benjamin Sayers owns shares in Austco Healthcare and will not trade shares within 2 days of publication. The editor Claude Walker does not own shares in Austco Healthcare and will not trade within 2 days of publication. This article is not intended to form the basis of an investment decision. Any statements that are advice under the law are general advice only. The author has not considered your investment objectives or personal situation. Any advice is authorised by Claude Walker (AR 1297632), Authorised Representative of Equity Story Pty Ltd (ABN 94 127 714 998) (AFSL 343937).