Lovisa Holdings Ltd (ASX: LOV) recorded another record earnings result for the H1 FY 2023 half year report, with revenue increasing 44.8% to $315.5 million and net profit after tax up 31.9% to $47.7 million. Lovisa’s H1 FY 2023 result showcased the ability to offset inflationary pressures with price increases, with gross margin improving by 190 basis points to 80.3%.

Lovisa increased free cash flow in the most recent half to $39.1 million, an improvement from the $36.4 million achieved in H1 FY 2022. Here, I am measuring free cash flow as net cash from operating activities of $98.5 million minus net investing cash flow of $31.9 million and lease liabilities of $27.1 million.

Lovisa spent $36.8 million opening 86 new stores and expanding into seven new regions during the half, offset by fit-out contributions of $5.0 million. Lovisa now has 715 stores in over 30 countries. Lovisa announced a 100% franked interim dividend of 38 cents per share, a one-cent increase on the prior year’s interim dividend. At a share price of $24, Lovisa is trading on a dividend yield of 3.1%. If you haven’t already, check out Raymond’s initial deep dive on Lovisa and why it’s a rare ASX gem.

Store Rollout Accelerates

Lovisa accelerated its store rollout this half under chief executive Victor Herrero, who was hired from Inditex (owner of Zara) to oversee the global expansion. Lovisa entered Namibia, Hong Kong, Mexico, Italy, Hungary, Romani and Columbia. In total, it opened 86 net new stores.

37 of the new stores added were in the United States. The USA now represents Lovisa’s largest region, surpassing Australia. Lovisa reiterated its laser focus on store economics, with the business willing to relocate or shut stores that it deems are not capable of meeting its profitability and return criteria. Management cited that the key restriction on growth is finding locations with attractive lease terms.

As for future expansion, the business has invested in headcount and new regional headquarters in Los Angeles, Poland and South Africa. Plans for entry into China look to be on the horizon, with Herrero citing that the company will likely enter when there is less uncertainty around COVID-19. Lovisa also said it would begin listing its product on online marketplaces, in order to achieve the dual goal of brand awareness and enhancing its omnichannel sales strategy.

Usually, when a company is expanding so quickly, it’s a sign that the management might be moving too fast and could lose focus on core markets and the customer. However this concern is somewhat alleviated by the presence of Chairman Brett Blundy, who owns 40.2% of Lovisa. Chris Lauder, the CFO, is also long-serving, having been with the business since 2017.

Potential Downside Events

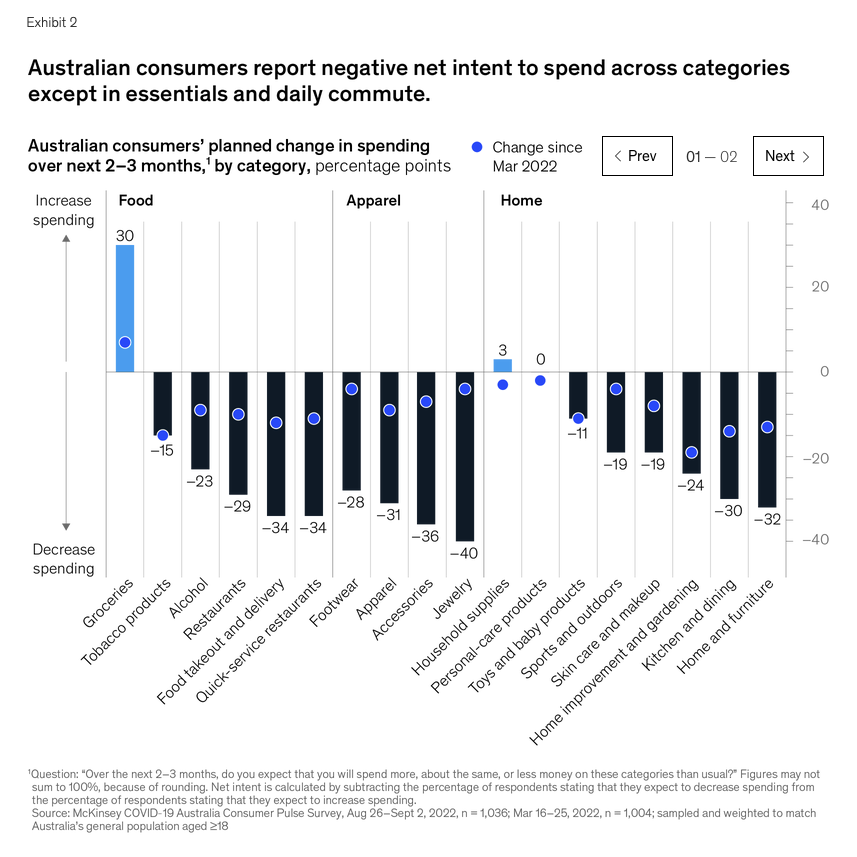

The following chart from McKinsey consumer spending intentions illustrates a market deterioration in discretionary spending, particularly for jewellery (-40%) and accessories (-36%). This survey is from August-September, so implies expectations for around December. But to me, the bigger takeaway is the fall in expectations from March 2022 (blue dot) to September 2022 (black bars). I would argue this trend is somewhat reflected by Lovisa’s trading updates for the past six months, and performance so far in H2 FY 2023 where total sales are only up 24% in the first seven weeks.

Another negative is that Lovisa may face a potential class-action lawsuit that alleges a failure to pay minimum rates of pay, directing staff not to take meal/toilet breaks, and directing staff to work extra hours without compensation. Lovisa’s Glassdoor reviews aren’t flattering either, with workers citing long hours, under-staffing and low remuneration. Even though it may never happen, the prospect of litigation here could risk brand damage, given Herroro is a very highly paid CEO.

On the investor call, an analyst asked about Lovisa’s ability to bargain with suppliers given the strength in its gross margin. Management was reasonably positive about the ability to bargain.

Are Lovisa Shares Attractive?

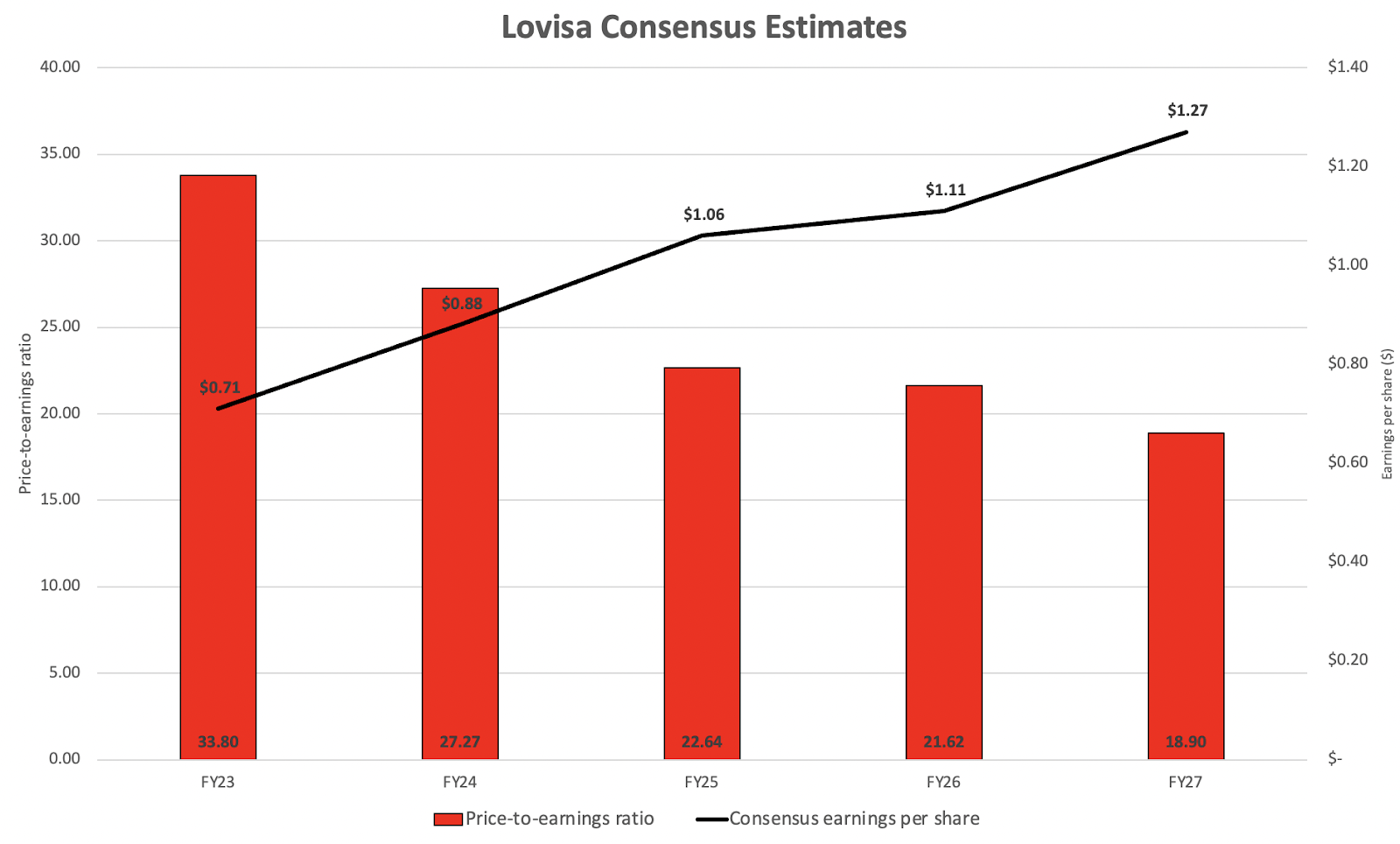

This was an awesome result for Lovisa. It is a quality retailer. For investors who believe in the growth story, and are willing to look past the potential weakness in consumer spending, this is an attractive global growth story. That said, the chart below of consensus estimates, accessed today, prior to any updates post-results. This view suggest that the market is well and truly pricing Lovisa for ongoing profit growth. And while that may well be reasonable, it is hard to argue the stock is undervalued.

To receive an email containing a selection of our company results coverage (including coverage you won’t find on the front page) please sign up to our Free Newsletter, below.

Sign Up To Our Free Newsletter