Probiotec Limited (ASX:PBP) released its FY23 results on Friday. The Probiotec share price yawned to a 1.1% higher close on the day.

In FY 2023, Probiotec revenue rose 17% to $214 million which was at the upper end of management guidance at the half year. 100% of the revenue growth was organic.

Underlying Probiotec EBITDA came in just above the midpoint of guidance at $35.3 million, up 8% on last year. On a statutory basis, EBITDA increased 2% to $35.4 million.

Underlying Probiotec EBIT was up 4% to $24 million and down 4% to $21.3 million on a statutory basis.

Underlying Probiotec NPAT was 3% lower at $13 million on an underlying basis and down 20% to $11 million on a statutory basis.

Probiotec EPS slipped 5% to 16 cents on an underlying basis and was down 21% on a statutory basis.

It is worth analysing the Probiotec adjusting items given the large discrepancy between underlying and statutory results. These included $2.7 million of amortisation of acquisition related intangibles which in my view is a valid exclusion. $0.6 million of fair value gains on acquisitions is another reasonable exception since these are non-cash in nature. Finally, non-recurring costs of $0.5 million is more debatable, particularly given Probiotec tends to record these in most years. But this is not a significant sum in isolation and therefore my view is that the underlying results represent a fair picture of Probiotec performance.

Probiotec declared a final fully franked dividend of 3.5 cents taking the full year dividend to 6.5 cents, up 16% on FY22.

Probiotec net debt at year end was $32.9 million and net debt to EBITDA was a manageable 0.9.

Operating cash flow less lease repayments was $11.5 million, down 19.1%. A working capital build of $7.1 million during the year contributed to the fall.

Probiotec free cash flow less lease repayments was $1.4 million, down from $7.3 million last year following a substantial increase in capital expenditure. This relates to additional manufacturing capacity coming online in the first half of FY24 to support growth.

Management elected not to provide formal guidance which is consistent with prior years. However, it did indicate both higher sales and earnings in FY24 and referenced elevated sales enquiries.

Probiotec will shortly commence a major warehouse consolidation project that management expects to complete by early 2025. The full year results presentation states $3 million to $5 million of expected annual savings following go live although the estimated investment cost is not given.

An effective strategy

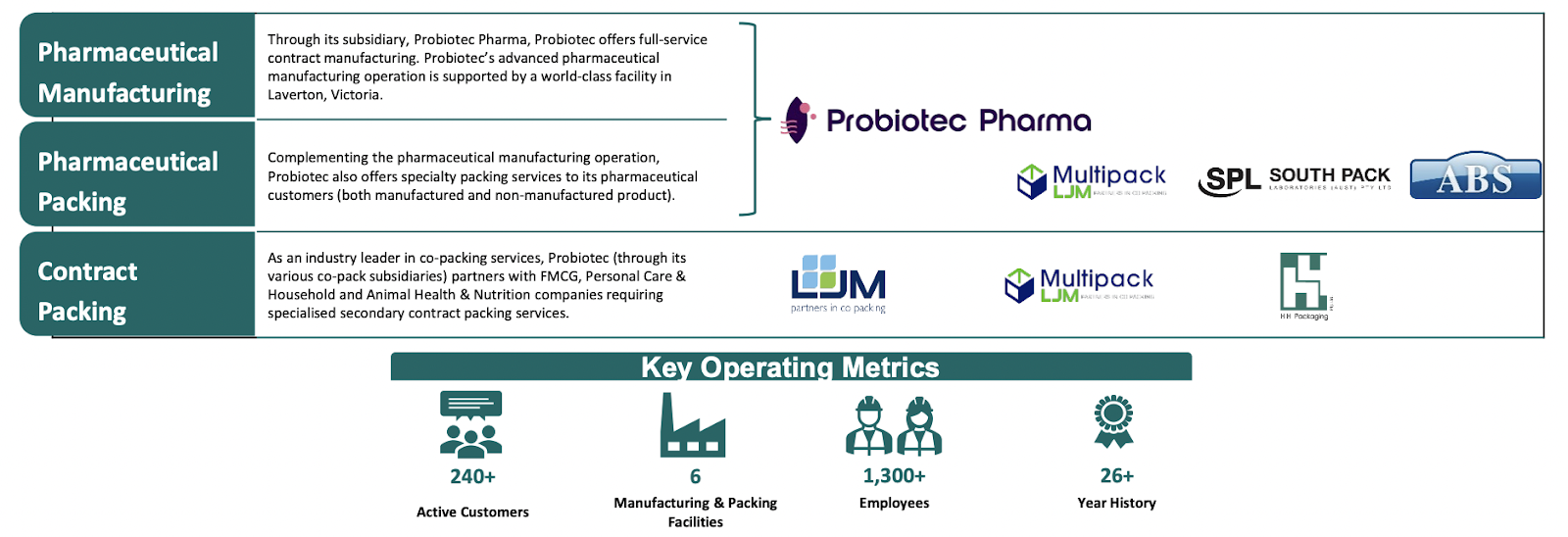

Probiotec is a manufacturer, distributor and packager of pharmaceuticals and fast moving consumer goods with operations across NSW and Victoria.

Source: Probiotec FY23 results presentation

The group has grown both organically and through acquisitions in recent years.

Source: Probiotec HY23 presentation

The aggressive pace of growth has led to a 54% increase in the company’s share count from 52.9 million in 2017 to 81.3 million today. In addition, net debt has grown from $7.1 million in June 2017 to $32.9 million as at June 2023.

Meanwhile, underlying NPAT has improved almost fivefold from $2.7 million in FY17 to $13 million in FY23, considerably outpacing share dilution over the period. The share price has rallied strongly as a result.

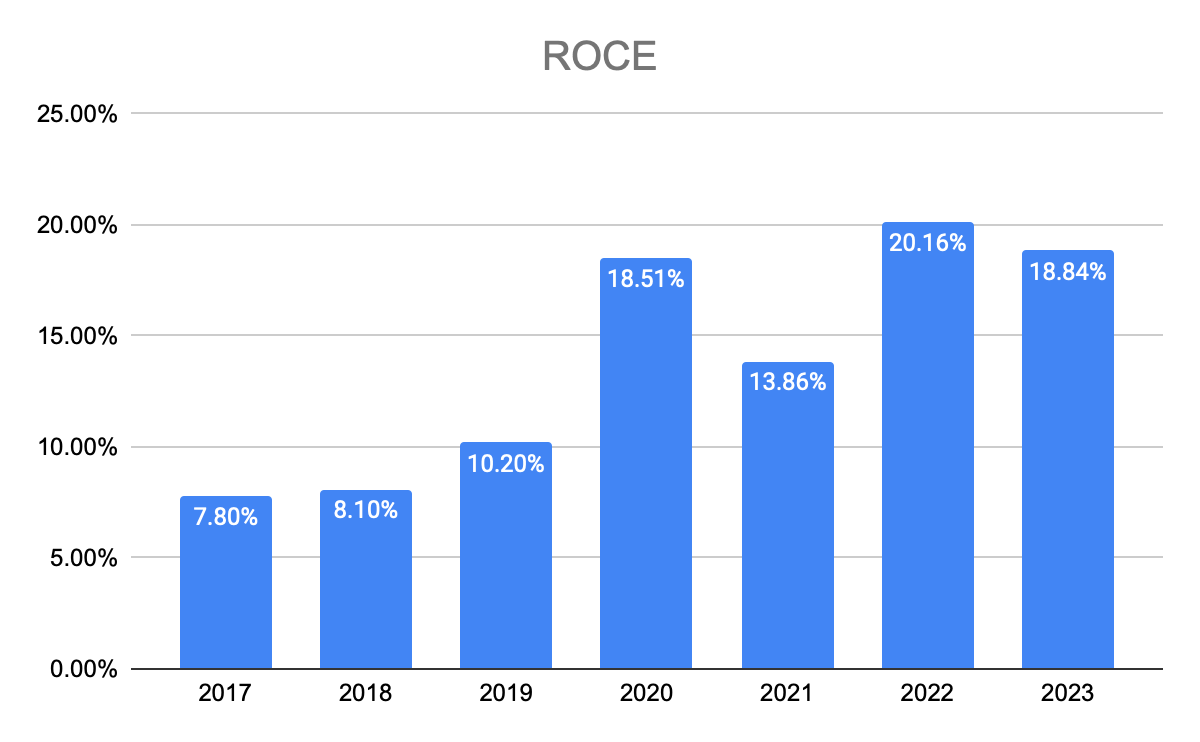

Further evidence that the strategy is working can be seen in the trend of improving returns on capital. Probiotec has seen an increase in adjusted earnings before interest and tax of $17.2 million since FY17 from an incremental capital investment of $61.5 million giving an impressive return on incremental capital of 28% over the period.

Source: Probiotec accounts

A possible emerging tailwind

There is scope for further improvement on the horizon which makes Probiotec an interesting proposition right now. As an Australian based manufacturer, Probiotec is currently benefiting from nascent reshoring trends driven by deteriorating relations between the West and China and the desire to strengthen supply chains since the pandemic. Assuming it persists, this trend should bolster the group’s organic growth and possibly margins if management can harness economies of scale.

Source: Probiotec FY23 presentation

The above chart shows the expected growth in Australian pharmaceutical manufacturing according to IBISWorld. As you can see, the impact of any long-term covid related boost to domestic manufacturing is fairly minor, although it is enough to see the industry return to growth after a period of stagnation.

Offsetting the possible reshoring tailwind is the spectre of continued inflation. Gross margins reduced 140 basis points to 30% in FY23 due to delays in passing on cost increases to customers. However, inflation is now moderating and customer price rises are fully effective from 1 July 2023 which could mean the worst is behind Probiotec.

A family business with a mixed past

Probiotec is run by brothers Wesley and Jared Stringer, CEO and CFO respectively, and who hold 8.7 million shares between them (over 10% of the company). Meanwhile, dad Charles Stringer has a 9.7 million shareholding representing a further 11.9% of the group. The latter founded Probiotec in 1996 and was CEO until 2015.

It has not been all plain sailing since Probiotec listed in 2007 for $1 per share and a market capitalisation of $46.5 million. Up until the end of 2009 things were going well and management even managed to raise capital at $2.55 (close to all-time highs) before the share price fell precipitously in 2010.

Back then, Probiotec primarily sold over the counter brands including slimming agents, vitamins and traditional herbal medicines while the contract manufacturing division contributed around 20% of group revenues.

An overly aggressive international expansion strategy combined with a slump in the Australian weight management sector brought profits crashing down in 2011.

Since 2017, there has been a sustained recovery in the share price as management pivoted away from the branded business and doubled down on packaging and contract manufacturing. It now boasts some of the world’s most successful consumer defensive and healthcare businesses as customers.

Conclusion

Probiotec is an improving, defensive, family run business with an impressive recent history of generating shareholder returns trading on a mid-teens PE multiple. No wonder there is currently speculation that the group might be taken over.

Probiotec is likely to deliver decent returns to shareholders in the future even if the onshoring thesis fizzles out, if it can continue to execute its current strategy. A possible nearterm takeover adds to the appeal.

To access all our subscriber only content, join the waitlist to become a supporter, via this link.

Disclosure: the author of this article Matt Brazier owns shares in PBP, but the editor Claude Walker does not and neither will trade in those shares for at least 2 days following the publication of this article. This article is not intended to form the basis of an investment decision and is not a recommendation. Any statements that are advice under the law are general advice only. The author has not considered your investment objectives or personal situation. Any advice is authorised by Claude Walker (AR 1297632), Authorised Representative of Equity Story Pty Ltd (ABN 94 127 714 998) (AFSL 343937).