Electrical distributor IPD Group (ASX: IPG) announced its annual results on Friday. Here are the key highlights.

IPD Group Revenue increased 28.3% to $226.9 million. Impressively, this growth was entirely organic.

Gross margin held steady at 38.2%, which is noteworthy given inflationary pressures.

EBITDA improved 37.1% to $27.7 million and IPD Group EBIT was similarly up 41% to $23.4 million. Both of these metrics came in at the top end of the company’s guidance range provided on 14 June.

IPD Group NPAT increased 45% to $16.1 million and EPS was 18.6 cents giving an historical PE ratio of 23.

The IPD Group balance sheet is healthy with $20.8 million in cash and no borrowing at year end. However, this figure was before the acquisition in July of EX Engineering, a Perth based supplier of electrical hazardous area equipment, for an initial $10.2 million.

IPD Group operating cash flow fell 33.7% to $7.4 million and free cash flow sank 64.9% to $2.5 million as both inventory and receivables rose significantly. Management said that the increase in working capital was due to restocking following normalisation of supply chains combined with ongoing business growth. This should mean that cash flow improves significantly next year.

The IPD Group Ltd (ASX:IPG) share price is up about 76% since we first highlighted it as one of 5 Stocks With Good Share Price Momentum back in November 2022. To access all our subscriber only content, join the waitlist to become a supporter, via this link.

The IPD Group final dividend rose 27% to 4.7 cents taking total dividends for the year to 9.3 cents representing a dividend yield of just over 2%.

The IPD Group share price closed down 4.8%. This may be related to the lack of guidance provided by management who said:

“It is too early in the new financial year to provide a full year earnings outlook given domestic and global economic volatility and the recent acquisition of Ex Engineering. IPD’s market focus on higher growth non-residential sectors of the economy will continue. The Board will provide an update on Q1 trading performance at the IPD Group Limited AGM on 28th November 2023.”

However, management also gave no guidance and provided a similarly worded statement upon release of last year’s results and so this may not be relevant to Friday’s share price fall. Furthermore, on Friday’s analyst call CEO Michael Sainsbury confirmed that sales for the first two months of the year are “consistent with our expectations around double digit organic growth”. Perhaps the weak cash flow result is a more likely explanation.

Is IPD Group (ASX: IPG) A Cyclical Stock

We can see below that IPD Group revenue and profit growth slowed in the second half of the year.

Source: IPD Group Accounts

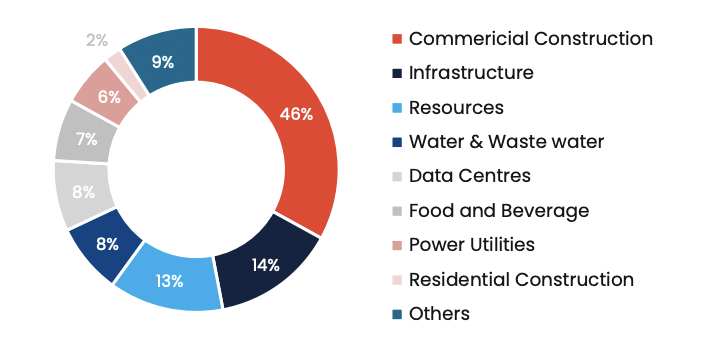

As a shareholder, it is concerning that IPD Group derives 73% of its revenue from cyclical sectors such as resources, infrastructure and commercial construction. The risk is somewhat mitigated by the fact that IPD Group also generates revenue from more defensive sectors such as water, data centres, food and beverage and utilities.

Source: IPD Group IPO Prospectus

Source: IPD Group FY23 Results Presentation (somewhat of a chart crime)

In addition, ongoing maintenance requirements including from the more cyclical sectors provides a fairly smooth demand backdrop over time.

Source: IPD Group IPO prospectus

IPD Group Growth Through Acquisition

IPD Group consists of three businesses. The core business is an electrical products distributor serving the Australian market called IPD. Then there is Gemtek which specialises in electric vehicle charging infrastructure. Finally, Addelec is a service provider focusing on high and low voltage products. Roughly 90% of revenue is generated from products with services making up the rest. For more details see Chris Coe’s thorough overview of the company late last year.

Although IPD Group’s history dates back to the 1950s, the business has grown substantially since a management buyout (MBO) in 2005. Revenue increased at a CAGR of over 12% between the MBO and the IPO. This is an impressive ‘through the cycle’ growth rate, albeit one assisted by acquisitions.

Source: IPD Group FY23 Results Presentation

Ex Engineering is the latest such acquisition for which management paid just over four times EBITDA. Such a low multiple inclines me to think that Ex Engineering is not a particularly good business. After all, it services the cyclical Oil & Gas, mining and agriculture sectors. However, in Friday’s analyst call Michael Sainsbury explained that there is a legal requirement for many of the products supplied by Ex Engineering to be replaced every three to five years offsetting any cyclical exposure.

Also, IPD Group can add value to companies like Ex Engineering through cross selling and rationalisation of distribution infrastructure. Furthermore, such deals expand the group’s product range and increase customer and supplier diversification which strengthens IPD Group’s competitive position over time.

In April 2022, IPD acquired Gemtek for $0.5 million establishing a presence in the electric vehicle market. Gemtek generated sales of just $1.3 million in FY21, but this looks like a savvy purchase given the expected acceleration in the the rollout of electric vehicle infrastructure in coming years.

Indeed, Electric Vehicle (EV) hardware accounted for $3.5 million of group revenue in FY23 compared to nothing prior to the Gemtek acquisition. In Friday’s call Michael Sainsbury made the rather bold claim that EVs represented a billion dollar opportunity for IPD over the coming decade.

IPD Group Board & Management

IPD enjoys high insider ownership and a longstanding leadership team. Michael Sainsbury joined in 2013 and has held the top job since 2015. CFO and exec director Mohamed Yoosuff has been with the group since 2005 when he was appointed CFO. They hold 1.2 million and 11.2 million shares respectively.

Other major shareholders include former CEO Keith Toose who was replaced by Michael Sainsbury in 2015. He was part of the management buyout in 2005 alongside Mohamed Yoosuff.

Source: IPD Group FY23 results presentation

Whilst IPD Group boasts an impressively high level of inside ownership, some insiders have started reducing their positions. This is perhaps to be expected given IPD Group shares are up over 250% since IPO just over 18 months ago.

In particular, non-executive Andrew Moffat sold 380,000 shares (just under half of his holdings) at $3.10 per share in March this year.

Meanwhile, The Bacon family reduced their ownership from 9.3% of the group to 5.9% at a sales price of $3.64 per share in May. The Bacon family became shareholders when IPD Group purchased their company Control Logic in 2020. Two of the family members are currently executives at IPD.

This is not ideal, but I would be more concerned if Mohamed Yoosuff started to sell down in meaningful size given his longer association with the group.

Value added distribution

Given IPD Group trades on a fairly fulsome forward price-to-earnings multiple of 18, a key question for investors is whether the business has a competitive advantage.

After all, distributors can be great businesses such as in the case of Dicker Data Ltd (ASX:DDR) or Steadfast Group Ltd (ASX:SDF) or they can be less good, such as with National Tyre & Wheel Ltd (ASX:NTD).

One reason for the difference in fortunes between these companies is that the former two distribute specialist products (IT hardware & software and business insurance) whereas National Tyre supplies a fairly commoditised product (tyres).

Dicker Data and Steadfast customers have bespoke needs and are therefore more likely to value the greater choice and technical expertise provided by a distributor. Meanwhile, National Tyre customers are more likely to be comfortable sourcing products independently.

I suspect that IPD is more similar to Dicker Data than National Tyre. IPD’s customers likely often need to engineer specific solutions which IPD can assist with by advising on an appropriate combination of products.

This value add would explain how the company managed to earn a return on capital of more than 50% in both FY22 (after adding back listing costs) and FY23. (My ROCE calculation differs from the company in that I adjust for cash)

Having said that, heavy dependence on key suppliers is a risk. For example, IPD derives about 40% of sales from European multinational ABB LTD (SWX:ABBN) growing at roughly 30% per year. Michael Sainsbury said that there was scope for further growth here, given that ABB still has a much lower market share in Australia compared to other parts of the world.

This partially alleviates my fear that IPD Group is a highly cyclical business, but I’m not sure such significant supplier risk is much more palatable.

IPD Group’s relationship with ABB has been in place for 30 years although it has expanded significantly since 2019 when ABB acquired GE Industrial Solutions. Since then, IPD has been appointed ABB’s Australian distributor for the electrical wholesale market and now sells ABB’s entire electrification product range including EV chargers.

IPD’s IPO prospectus lists Schneider Electric SE (EPA:SU) as a competitor in the products division. Schneider Electric is an electrical products manufacturer of similar scale to ABB. Clearly, there is a risk that ABB might also decide to distribute directly into Australia in the future.

However, perhaps it makes more sense for manufacturers to focus on their core competency rather than vertically integrate given the level of service typically required by IPD’s customers.

Indeed, IPD Group had been purchasing from its top 10 suppliers for more than 15 years at the time of its IPO. Customer relationships are even stronger by this measure with the top 10 having been retained for over 25 years at the time of IPO.

I wonder if it might be possible to automate the educational aspect of selling electrical products in future given recent advances in AI. If so, then this might threaten IPD’s business model and make it more likely that manufacturers take greater control of their supply chain.

On the other hand, perhaps distributors like IPD are best placed to create such solutions given the customer data available to them and the internal knowledge base of their reps. IPD already provides a number of software tools designed to help customers to select, install and configure various products.

Closing thoughts On The IPD Group FY 2023 Results

Friday’s IPD Group results were strong, albeit as expected. Given IPD Group’s relatively short listed life, we do not have much historical data to judge the degree to which recent sales growth is cyclically driven. Other more obviously cyclical businesses are certainly benefiting from the upswing in resources and infrastructure investment currently underway, and I suspect IPD Group is also. Offsetting this risk is the secular tailwind of decarbonisation, its exposure to maintenance spend and the fairly diversified range of end markets that IPD Group serves.

I actually held shares in IPD Group into Friday’s results announcement, but sold them on Monday. The process of researching and writing this article caused my opinion of the company to change. I had previously thought that IPD Group was a quality compounder, but now believe it is far more cyclical in nature. Therefore, the best returns from owning IPD Group stock are likely behind us, and I think there are better investment options available on the ASX.

To access all our subscriber only content, join the waitlist to become a supporter, via this link.

Disclosure: neither the author of this article Matt Brazier nor the editor Claude Walker owns shares in IPG and neither will trade in those shares for at least 2 days following the publication of this article. This article is not intended to form the basis of an investment decision and is not a recommendation. Any statements that are advice under the law are general advice only. The author has not considered your investment objectives or personal situation. Any advice is authorised by Claude Walker (AR 1297632), Authorised Representative of Equity Story Pty Ltd (ABN 94 127 714 998) (AFSL 343937).

The information contained in this report is not intended as and shall not be understood or construed as personal financial product advice. You should consider whether the advice is suitable for you and your personal circumstances. Before you make any decision about whether to acquire a certain product, you should obtain and read the relevant product disclosure statement. Nothing in this report should be understood as a solicitation or recommendation to buy or sell any financial products. A Rich Life does not warrant or represent that the information, opinions or conclusions contained in this report are accurate, reliable, complete or current. Future results may materially vary from such opinions, forecasts, projections or forward looking statements. You should be aware that any references to past performance does not indicate or guarantee future performance.Save time at tax time: If you’d like to try Sharesight, please click on this link for a FREE trial. It saves heaps of time doing your tax and gives you plenty of insights about your returns. If you do decide to upgrade to a premium offering, you’ll get some discount (the best deal available, I’m told) and we’ll get a small contribution.